Founded in 1896, Tootsie Roll (TR) is the maker of famous candy brands such as: Tootsie Roll, Tootsie Pops, Child’s Play, Caramel Apple Pops, Charms, Blow-Pop, Junior Mints, Charleston Chew, Sugar Daddy, Sugar Babies, Andes, Razzles, and Dubble Bubble.

The company sells its products primarily through 30 candy and grocery brokers to over 4,000 supermarkets, variety stores, dollar stores, chain grocers, and drug chains in the U.S., as well as numerous outlets in Canada and Mexico, which are its largest foreign markets. Tootsie Roll also sells in Europe, the Middle East, and Asia, but the U.S. is its largest market, accounting for 91% of total product revenue.

With 52 consecutive annual dividend increases, Tootsie Roll is a dividend king.

Business Analysis

In 1896, Leo Hirschfield took his family recipes and started a candy company out of his Brooklyn, New York, shop. The famed inventor developed numerous patented products for Stern & Saalberg which later became The Sweets Company of America and eventually Tootsie Roll.

Tootsie Roll achieved its biggest success on a combination of two things. First, it was a pioneer in advertising, beginning with its namesake Tootsie Rolls in 1914. Over the years, the company would go on to develop famous print, radio, and TV advertising campaigns including “how many licks to get to the center of a Tootsie Pop”. Last year, Tootsie Roll spent $18.8 million, or 3.6% of its revenue, on advertising.

The second major growth driver for the company was actually America’s involvement in World War I and II. Tootsie Roll refocused its advertising on patriotism and made its candy’s synonymous with freedom, democracy, and America.

During the wars, Tootsie Roll products were added to military rations which helped develop brand loyalty with many American GIs. That loyalty translated to increased sales when they returned home and started families (their children then enjoyed Tootsie Roll products as well).

Over the years, management has focused almost exclusively on organic growth. The company’s only major acquisitions included famous candy brands such as: Andes, Dubble Bubble, Junior Mints, and Dots. The last major acquisition the company undertook was in 2004 when it paid $200 million to buy Concord Confections, the Toronto-based maker of famous bubble gums such as Dubble Bubble.

Unfortunately, Tootsie Roll has run into a growth problem over the past six years with sales peaking in 2012. Management’s response was doubling down on the Enterprise Resource Planning (ERP) strategy it began in 2011. This was a data-driven analytical approach to streamlining the firm’s manufacturing and supply chains to minimize costs and maximize economies of scale. That included an emphasis on specialized, high-speed and increasingly automated equipment that allowed its 2,000 employees to generate $519 million in sales in 2017 ($260,000 per employee in revenue).

The results were impressive with operating margin rising from 11% in 2011 to 18% in 2016, and returns on invested capital (proxy for good capital allocation and quality management) also rising strongly for several years. However, ultimately a company can only cut costs so much, and Tootsie Roll has seen its profitability deteriorate over the last two years.

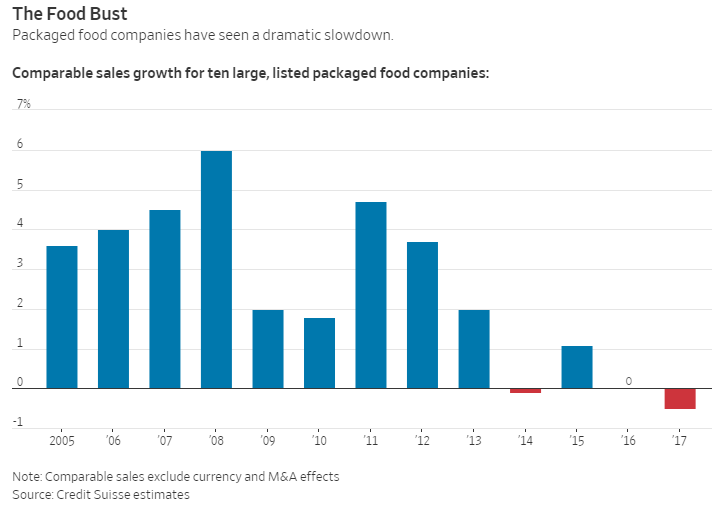

In fairness to the company, the margin compression Tootsie Roll is facing (more on this in a moment) is occurring across the industry. And Tootsie Roll still enjoys some of the highest margins in the industry. However, its free cash flow and returns on invested capital have been declining. This is largely due to increased investment in automated manufacturing, which has caused capex spending to almost double between 2011 and 2017.

Diminishing returns on these investments (in terms of cost savings) have caused return on invested capital (a rolling measure of how efficiently management allocates capital) to decline. Ultimately, Tootsie Roll needs to return to growth (sales have declined in four of the last five years) by either launching new products or expanding into new markets outside of its core U.S. operations.

So far the company has indicated no major plans along those lines. However, Tootsie Roll does have a strong balance sheet which gives it the financial flexibility to try such strategies. For example, while Tootsie Roll doesn’t have a credit rating due to its small size (and low budget), the firm has around $100 million in net cash (cash minus debt) on its balance sheet.

Overall, Tootsie Roll seems likely to remain a mature cash cow for the foreseeable future. However, the company’s dividend growth rate has decelerated from 7% per year over the last two decades to just 3% in 2017. Payout growth seems likely to remain unimpressive given the challenging secular industry trends Tootsie Roll faces in the years ahead.

Key Risks

While Tootsie Roll has a great track record of dividend growth over the past 50 years, there are growing signs that the company’s best days might be behind it.

One of Tootsie Roll’s challenges is its pension. Tootsie Roll is part of a multi-employer pension plan called the Bakery and Confectionery Union and Industry International Pension Fund. This fund is 57% funded meaning that its assets are only expected to cover 57% of its projected future liabilities. That’s why the plan is considered to be in “critical and declining status” and expected to become insolvent (unable to pay obligations) by 2030.

Fixing the problem will either require Tootsie Roll to make much larger contributions (which will greatly hurt profitability) or leave the pension entirely. However, to do so would require a withdrawal liability of $82 million (close to 5% of Tootsie Roll’s current market cap, and approximately 15% of revenue). Basically, any company can leave this multi-company pension, but they need to pay a large one-time fine to settle their share of future benefits they owe.

Tootsie Roll’s withdrawal fine continues to grow quickly (it was $61 million in 2015), and management still hasn’t determined whether or not the firm can ultimately salvage this pension or will need to cut its losses and end its participation.

The problem with multi-employer pensions is that other companies are in the same boat as Tootsie Roll. They have been underfunding the pension for decades and now either everyone needs to significantly increase payments into the fund, or some companies might decide to drop out.

While unlikely, this could trigger a spiral in which a smaller number of companies are left participating in the plan, making the pension ever more underfunded and the withdrawal penalty even steeper for the companies left in the program. Tootsie Roll’s small size (annual sales of about $500 million) means that within a few years the company may be forced to leave this pension and pay a fine in excess of $100 million. For context, in 2017 Tootsie Roll’s net income was $65 million.

And while the company’s balance sheet is strong with $102 million in net cash, the point is that its deeply underfunded pension obligations might end up wiping out its cash reserves in one fell swoop. That would greatly limit Tootsie Roll’s financial flexibility during a time when it is struggling with a long-term trend of declining candy sales in its core markets.

Rising concerns about obesity have caused a secular trend against candy and sugary sweets. For instance, the U.S. government’s 2015 to 2020 dietary guidelines recommend that sugar represent no more than 10% of calories consumed. For most Americans, that means limiting sugar intake to 12 teaspoons of sugar per day or less. For context, a can of Coke has 10 teaspoons of sugar.

Consumers appear to be on board with the low sugar trend, and Euromonitor International estimates that sales in the chocolate confectionery market (where Tootsie Roll operates) will continue declining gradually through at least 2021 (and perhaps far beyond this timeframe).

Most of Tootsie Roll’s top brands are on the wrong side of this trend, filled with sugar, corn syrup, and artificial colors and flavors.

Meanwhile, the company has faced higher input prices in the form of sugar and corn syrup, the two main ingredients used in its products. Shipping costs are rising as well due to higher oil prices and a large and growing shortage of truckers (due to retirement overtaking new hires).

This one-two punch of declining sales and rising costs has caused the company’s operating margin to decline significantly, resulting in double-digit EPS declines in recent quarters. Historically, food companies with strong brands offset rising costs by passing them onto consumers in the form of higher prices. However, there are two reasons that Tootsie Roll’s ability to do that may be in decline as well.

For one thing, changing consumer tastes, especially among Millennials (the largest generation in America right now), have made household brands less valuable than in the past. This is why numerous food companies such as General Mills (GIS) and Campbell Soup (CPB) have been struggling to grow their top lines.

Tootsie Roll’s pricing power might also prove limited given its heavy reliance on Walmart (WMT), which represented 24% of its sales in 2017. Walmart is locked in a fierce battle with Amazon (AMZN), Target (TGT), and Costco (COST) to transition to a more e-commerce-focused business model.

While Walmart’s online sales are growing strongly, margins on internet sales are lower than the company’s core brick and mortar business. As a result, Walmart is fighting back by squeezing its suppliers as much as possible and rolling out an increasing number of store-brand products to maintain its famous everyday low prices.

Finally, be aware that Tootsie Roll is currently run by Ellen Gordon, who took over the company in 1962. The Gordon family has run Tootsie Roll since 1948 and controls 83% of the Class B shares. Those have 10 times the voting rights of Class A shares that regular investors own.

In other words, this struggling company is effectively controlled by the 86-year-old Ms. Gordon who doesn’t believe in much shareholder transparency. For example, the company doesn’t do conference calls, CEO interviews, or provide investor presentations other than the annual report.

Critics of the Gordons, including shareholders who have periodically sued management over the years, claim that the Gordon’s have abused this absolute power by paying themselves lavishly in both salary and benefits.

Anyone owning shares of Tootsie Roll has to accept the fact that they are completely at the mercy of non-transparent management, who can do almost anything it wants, as well as pay itself whatever it likes.

Ms. Gordon is also very stingy when it comes to R&D with the company effectively investing nothing each year in new product development. Instead, management appears to believe that cost cutting activities across its supply, logistics, and manufacturing chains will be able to right the ship and restore the company to bottom line growth.

However, with the trend in candy sales looking firmly negative, and Tootsie Roll having very little growth presence (and almost no branding power) in fast-growing emerging markets, there is little reason to believe that Tootsie Roll’s sales can achieve any significant growth. Combined with continued margin pressure, Tootsie Roll’s future dividend growth potential appears rather bleak.

Closing Thoughts on Tootsie Roll

Tootsie Roll has a storied past and boasts one of the most impressive dividend growth track records in America. That being said, its large portfolio of well-known candy brands is increasingly out of favor with consumers, and management has not executed on growth opportunities in fast-growing international markets.

Combined with the stock’s low yield, margin headwinds, pension problems (our Dividend Safety Scores account for unfunded pension debt), questionable corporate governance, and weak dividend growth prospects, income investors are likely better off looking elsewhere.

To learn more about Tootsie Roll’s dividend safety and growth profile, please click here.

Companies that cheat their employees will eventually go bankrupt. I once was a victim of one of those companies. TR will be a victim of their own poor management!