Founded in 1890, Emerson Electric is a global industrial conglomerate that serves the oil and gas, refining, chemicals, power generation, pharma, food and beverages, pulp and paper, metal and mining, and municipal water supply sectors.

Founded in 1890, Emerson Electric is a global industrial conglomerate that serves the oil and gas, refining, chemicals, power generation, pharma, food and beverages, pulp and paper, metal and mining, and municipal water supply sectors.

Emerson Electric brings together technology and engineering to provide solutions for customers in the process, industrial, commercial, and residential markets.

Whether it’s monitoring food temperatures throughout the supply chain or replacing a deteriorating valve that could cause costly downtime, the company helps customers optimize their operations and increase reliability, efficiency, and safety.

Emerson completed a number of strategic actions in recent years to streamline its portfolio and refocus on its core businesses. The company divested more than $5 billion worth of operations, including its network power systems and power generation, motors, and drives businesses.

Emerson also completed its $3.15 billion acquisition of Pentair’s valves and controls business in 2017. This deal expanded Emerson’s capabilities to help it provide broader solutions to more of its customers.

Emerson manages it business through two segments.

Automation Solutions (62% of sales, 53% of profits) – enables manufacturers to maximize production, protect personnel and the environment, and optimize their energy efficiency and operating costs through a broad offering of integrated solutions and products, including measurement and analytical instrumentation, industrial valves and equipment, and process control systems.

Commercial & Residential Solutions (38% of sales, 47% of profits) – provides products and solutions that promote energy efficiency, enhance household and commercial comfort, and protect food quality and sustainability through heating, air conditioning, and refrigeration technology, as well as a broad range of tools and appliance solutions.

Geographically, the company generates 52% of its revenue in North America, 21% in Asia, 16% in Europe, 6% in Middle East/Africa, and 5% in Latin America.

Business Analysis

Very few companies have been in business as long as Emerson Electric has, and even fewer can boast such a lengthy dividend growth streak (60+ years). The company’s track record speaks to its durability, disciplined capital allocation, and numerous competitive advantages.

Emerson sells thousands of different products, but almost all of them account for just a small percentage of an end product’s total cost. As a result, customers have less reasons to squeeze Emerson on prices or consider switching to competitors’ offerings.

That’s especially true since most of Emerson’s products also provide mission-critical functionality, such as gauging the pressure and flow rate of an oil well. The company’s customers need reliability, so Emerson’s longevity and proven expertise give it a trusted reputation and strong market share position.

Unlike many other industrial companies, Emerson sells many of its products through a large direct sales force and also has thousands of field engineers working directly with its customers.

These efforts further solidify its favorable brand and customer relationships, deepening switching costs and helping the company continuously deliver innovative, rigorous solutions that solve customers’ most challenging problems.

Thanks to the company’s selectiveness with which product niches it enters, as well as its focus on quality, reliability, and strong customer relationships, Emerson has been able to maintain a leading market share position in many core categories – control valves, fluid control, measurement devices, compressors, wireless devices, and more.

Holding onto top market share positions for 100+ years has many benefits, including a massive installed base in the tens of billions of dollars.

Having a huge installed base really helps smooth out results because it provides more reliable (and high-margin) aftermarket business – customers need to keep their equipment up and running to stay efficient, and Emerson helps them do that. In fact, predictive maintenance can lead to a 30% reduction in maintenance costs and a 70% cut in downtime from equipment breakdowns, according to the company.

Furthermore, a lot of Emerson’s industrial automation products (e.g. wireless sensors, software, instrumentation) are tied to the “industrial internet” theme. As this technology continues advancing and data management needs grow, Emerson has potential to better monetize its installed base.

The company has installed more than 30,000 wireless networks that have logged over 10 billion operating hours, for example. There are plenty of insights to be harvested there to help customers continue becoming more efficient.

Speaking of growth, Emerson, led by President, Chairman, and CEO David Farr, who has been with the company for over 30 years, has a long track record of making prudent capital allocation decisions to better position the company.

Since taking the top spot in 2000, Farr has done an admirable job of selling off low margin businesses, acquiring more profitable divisions, and expanding into developing markets, which will be a key for sustaining long-term growth.

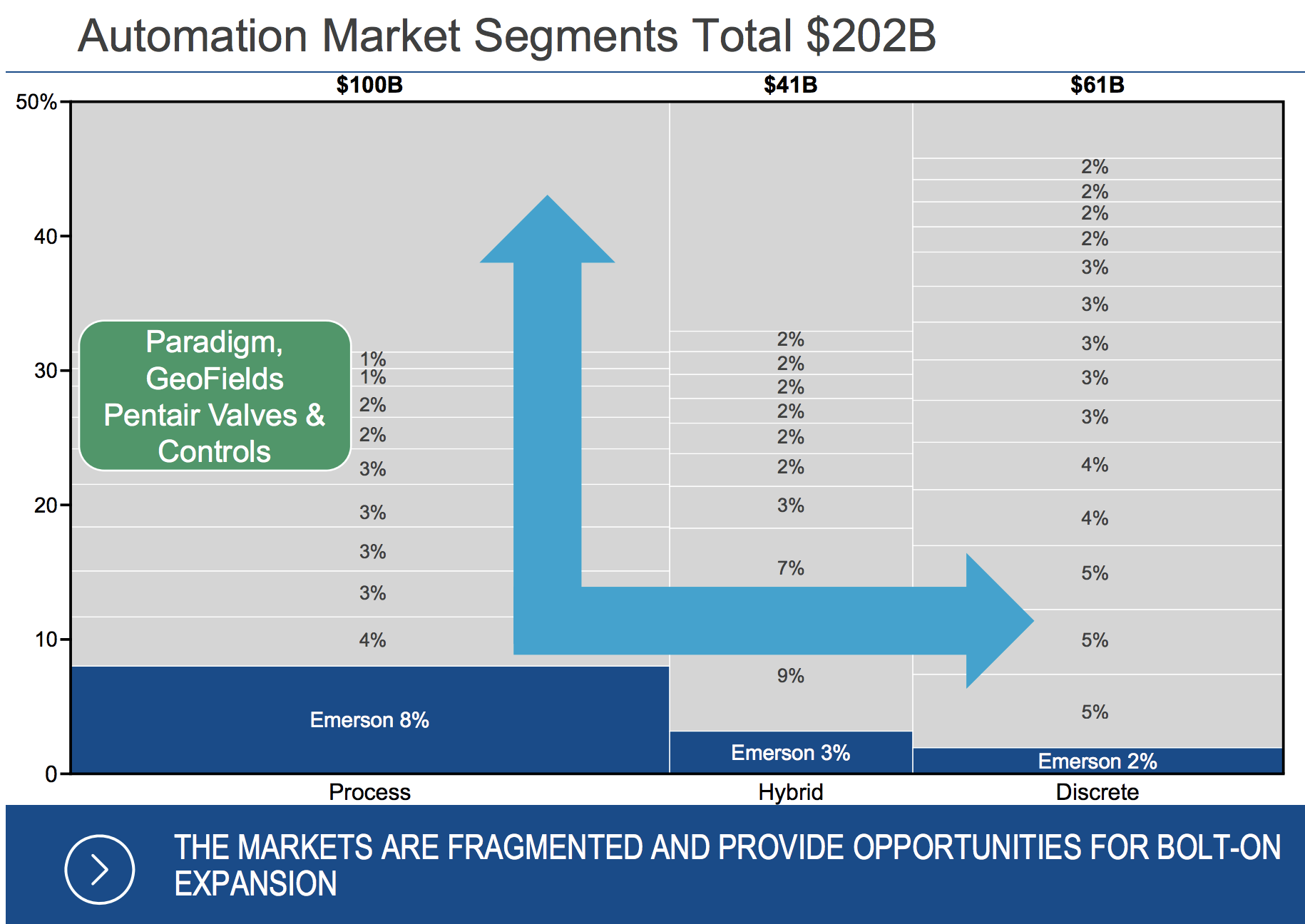

Emerson’s two business segments have benefited greatly from bolt-on acquisitions over the years, and there is plenty of runway left for growth. The company estimates that the addressable global industrial automation market is more than $200 billion, but its market share is well under 10%.

Commercial and residential markets add another $30 billion to the company’s growth opportunities. Emerson is among the leading innovators when it comes to energy efficient heating and cooling systems, which helps explain this segment’s impressive margins. With a continued recovery in U.S. housing construction, this business will likely represent a key growth driver for Emerson.

Despite Emerson’s long-term expansion opportunities, industrial companies are still cyclical, with growth in sales, earnings, and cash flow generally tied to that of the broader global economy.

With decades of experience in both good business cycles and bad, the company has managed to use disciplined cost cutting to keep Emerson’s margins and returns on capital far above its peers. Perhaps most importantly, Emerson has maintained a high free cash flow margin that has continued to support its dividend and allowed continued dividend growth, even through numerous lean periods.

Key Risks

There are three main risks to be aware of before investing in Emerson.

First, even after the company’s restructuring in recent years, Emerson is very heavily exposed to the oil & gas sector. In fact, almost 50% of its sales come from this highly cyclical industry. Investors considering Emerson should think of it almost more as an energy or basic materials company given its customers’ dependence on economic growth and high commodity prices. Its aftermarket business makes it less volatile, but Emerson is still sensitive to macro conditions.

In addition, Emerson’s geographic diversification, which is likely to increase in the coming years, exposes the company to some foreign currency exchange rate risk. When the U.S. dollar strengthens, the company reports lower sales and earnings for accounting purposes.

Fortunately, Emerson’s sales and manufacturing costs are fairly well aligned regionally, minimizing the risk to its actual profits. However, the company’s foreign competitors are better able to undercut the company on price when the U.S. dollar is strong. This shouldn’t impact Emerson’s long-term earnings power, but it could weigh on the stock any given quarter or year.

Finally, Emerson has made it clear that the company is on the hunt for acquisitions, driven in part by a desire to replace some of the lower-margin, slower-growing revenue it divested in recent years.

While bolt-on deals are often a good move for industrial companies, Emerson is also interested in deals that are significantly larger in size. The company bid nearly $30 billion for Rockwell Automation (ROK) in late 2017, for example, but its offer was rejected.

Large acquisitions increase risk, as management teams are often prone to overestimating synergies, underestimating integration costs, and paying too much for a prized asset. Emerson’s management team deserves the benefit of the doubt here given their capital allocation track record, but there are never any guarantees.

Closing Thoughts on Emerson Electric

Emerson Electric is a tried-and-true dividend grower with enduring competitive advantages stemming from its global scale, large installed base, wide breadth of mission-critical solutions, and conservative management team.

The company’s recent moves to reposition its business for stronger long-term growth and better profitability should bear fruit over the coming years, even if they have come at the expense of near-term earnings growth. As industrial companies seek to become more efficient and manufacturers embrace more digital technologies, the company should also enjoy some wind at its back thanks to its large presence in automation markets.

Income investors shouldn’t forget about Emerson Electric’s sensitivity to commodity prices and the general health of the industrial economy. However, the company appears to have the financial strength and discipline to ride out just about any cycle thrown its way while improving its long-term earnings power.

To learn more about Emerson Electric’s dividend safety and growth profile, please click here.

Brian,

Looking at the detail for EMR, their Free Cash Flow per share for FY 2017 was the lowest for at least 12 years; further, in their credit metrics you show FCF of $1.4 billion and dividend payments of $1.2 billion which, in turn, should give a FCF payout ratio of somewhere over 80% while the graph shows a 50% for the most recent year, 2016.

When or how do the dividend safety metrics adjust for the rolling quarterly changes to FCF?

Thanks

What about valuation? p/e is all time high at 26.7. Brian, what’s your recommendation on entry price?

Yes Brian I agree with the above. What price would you be willing to pay for EMR?