The first Starbucks (SBUX) location opened in 1971, and the company has since grown to become the world’s largest coffee purveyor with just over 28,000 stores in more than 75 countries. Starbucks stores sell not just premium coffee but also tea, packaged coffee, juices, bottled water, pastries, and various lunch items.

In addition, the company licenses several of its products, which are available in supermarkets and stores, and sells through other up-and-coming brands such as Teavana, Tazo, Seattle’s Best Coffee, Evolution Fresh, La Boulange, and Ethos.

In its most recent fiscal year, the vast majority of Starbucks’ sales came from the company’s namesake, company-owned stores.

- Company-owned stores: 79% of revenue (growing 5% a year)

- Licensed stores: 11% of revenue (growing 9% a year)

- Consumer packaged goods: 10% of revenue (growing 3% a year)

By geography, Starbucks generated 70% of its revenue last year in the Americas (U.S., Canada, Latin America); 13% in China / Asia Pacific; and 5% in Europe, Middle East, and Africa. The remaining 12% of revenue was related to channel sales of Starbucks’ products and other business segments.

Business Analysis

Starbucks’ key to its long history of impressive sales and earnings growth has largely come down to its ability to differentiate its brand and often become a destination in its own right. Each location does its best to provide customers with a unique Starbucks Experience, which is built upon superior service, high-quality coffee, a seamless digital experience, and clean and well-maintained stores that reflect the personalities of the communities in which they operate.

The end result has been a high degree of customer loyalty in what is otherwise a very crowded coffee market, helping the company command strong pricing power and generate excellent profitability. For example, the company’s free cash flow margin is north of 20%.

To put it another way, Starbucks’ competitive advantages, including its substantial economies of scale, mean that this coffee chain has the profitability profile typically seen only in far more lucrative industries such as pharmaceuticals or technology. That’s a testament to the great job management has done creating a unique coffee experience that its core customers will continuously pay up for.

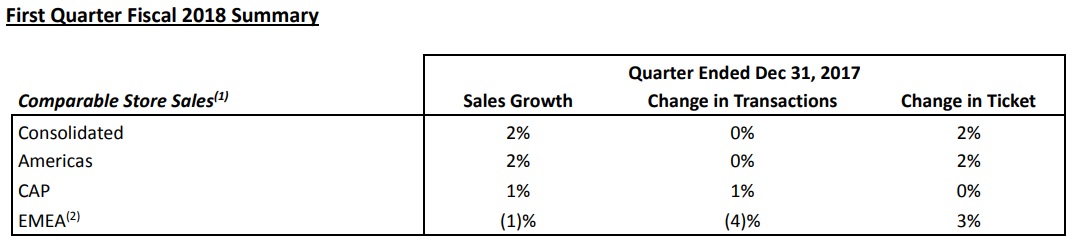

However, Starbucks has seen its growth slow substantially in recent years. For example, in the last quarter the company’s same-store comps (sales growth recorded by stores open for at least a year) fell to their lowest levels in years, 2% in the U.S. and to -1% to 1% in the rest of the world.

Starbucks Q1 2018 Same-Store Comparable Sales

Only in China, where management says it’s “cracked the code,” did the company post the kinds of comps (6%) and revenue growth (30%) it has long been famous for. This is largely due to Starbucks’ executing well on its decadeslong track record of innovating new ways for consumers to access its products.

Specifically, the company has found success in expanding its loyalty program (6 million Chinese members and growing fast) and integrating mobile payments (WePay and AliPay) into its Chinese app. Like in the U.S., this app allows customers to locate stores, order online, and pick up orders at a physical location with minimal or no wait time. This helps to drive faster turnover and throughput, which helps fuel stronger sales volumes, strong comps, and overall earnings growth.

Management also has a multi-prong plan to address its decelerating U.S. sales and help it achieve its long-term growth targets of:

- 3% to 5% global same store comps

- High-single digit revenue growth

- Double-digit earnings and free cash flow per share growth

Management’s earnings and cash flow growth targets seem possible thanks to ongoing cost cutting and efficiency initiatives that analysts expect to allow Starbucks to raise its operating margins to 20% over the coming years.

These U.S. changes include simplified store operations and more use of throughput-boosting technologies such as its popular app and increased use of mobile payments which speed up transaction times.

The company also plans to continue expansion of new offerings like the Mercato fresh foods menu, Blonde Espresso roast, and Nitro Cold Brew coffee offerings. The Nitro Cold Brew rollout is being increased by 1,000 stores in 2018 (to 2,300), and management says that Nitro Cold Brew usually boosts comps by 1%.

More importantly, Starbucks is continuing to focus on its loyalty program, which saw 18% U.S. member growth in 2016, and 11% growth in 2017. Today this program has 14 million U.S. members, or close to 20% of the 75 million U.S. customers it serves each month. Recently Starbucks partnered with Chase/Visa to launch a co-branded credit card to further improve its loyalty program, which accounted for more than 40% of U.S. and Canadian transactions in its most recent quarter.

Starbucks’ loyalty program members usually purchase about twice as much as non members, which is why the company is so focused on expanding the program to as many U.S. (and global) customers as possible.

In addition, Starbucks is planning on rolling out new store concepts, both big and small. For example, it’s experimenting with smaller-format express stores, drive-thrus, beverage trucks, and kiosks.

On the high end, the company is also opening more Starbucks Roasteries, super premium locations that have much higher-end offerings that some reviewers have called “Starbucks on crack.” Prices for some of its select reserve coffees in these stores can sell for as much as $100 per pound. Roasteries are also coming with Princi bakeries, which offer premium artisanal baked goods.

Starbucks Shanghai Roastery

Starbucks founder and Chairman Howard Schultz is spearheading the roastery concept, first launched in Seattle, but now expanding to Chicago, New York, London, and Shanghai. In fact, the Shanghai roastery, which opened in December of 2017, is the largest coffee shop in the world, and management says it’s performing “well above expectations.”

And speaking of China, Starbucks is firing on all cylinders in that region. The company commands about 75% market share in coffee shops, compared to McDonald’s second-place position of about 10%. In late 2017 the company bought out the remaining 50% stake in its east China stores (1,400 of them) from its joint venture partners Uni-President and President Chain Store Corporation. This means that Starbucks now owns all 3,100 of its successful Chinese stores.

By 2021 the company plans to open 1,900 more locations, bringing its China store count to 5,000. However, according to CEO Kevin Johnson, he expects China to one day have more stores than the U.S., where Starbucks operates 14,000 locations.

The bottom line is that Starbucks has done a remarkable job in building itself a moat in a cutthroat industry characterized by minimal switching costs and low margins. Starbucks has also shown its dedication to rewarding dividend investors with payout increases of 25% in 2016 and 20% in 2017. And with tax reform expected to boost earnings by 25% in 2018, dividend lovers can likely expect similar growth this year.

Key Risks

Starbucks is undoubtedly a great business but also faces some major challenges going forward.

For example, in the U.S. market, which management has called one of its core growth catalyst (the other being China), the company has seen same-store sales growth continue to fall for years.

Part of this is due to declining mall traffic. While mall locations make up less than 10% of Starbucks’ U.S. locations, the strong negative trends of the past few quarters has been enough to severely ding its comps in America.

Another problem that management highlighted is that non-reward members are less reliable sources of sales, especially for holiday specialty products and merchandise, which were disappointing in 2017. Only time will tell if management’s plans to boost U.S. sales will be a success.

The biggest issue is that with about 14,000 U.S. stores, Starbucks has pretty much saturated the domestic market, and it becomes increasingly difficult to consistently maintain the unique store experience that has made the company so successful over the years. What’s worse, the U.S. coffee shop market is becoming even more competitive with McDonald’s (MCD) making an aggressive push into premium coffees on the high end.

On the low end, Dunkin’ Brands (DNKN) is also planning to rapidly expand into the western half of the U.S. The new competition, at every price point, could make it harder for Starbucks to increase the size of its loyal core user base (75 million U.S. monthly visitors). The same problem might apply to the roastery concept. After all, how many people are willing to pay $4, $5, or more for a cup of coffee, no matter how good it tastes and is marketed?

As a result, the company will need to largely focus internationally to hit its target of 2,300 new store openings in 2018. However, as was demonstrated by the even weaker comps in Asia and Europe last quarter, Starbucks’ ability to recreate its strong U.S. success in other countries isn’t guaranteed.

But what about China, where Starbucks plans to open another 1,900 stores over the coming years? There Starbucks is indeed seeing massive success, with management seeming to have “cracked the code” of wooing China’s massively expanding middle class, which is expected to number 600 million by 2021.

However, remember that relying too much on one growth market can be dangerous. Yum Brands (owner of Pizza Hut, KFC, and Taco Bell) saw amazing success in China for years, particularly in its KFC store concept. However, starting in 2012 and lasting through 2015, a tainted chicken scare saw Chinese KFC sales plummet, by as much as 19% to 25% a year, for several years.

Combine this with the risk that Chinese tastes might change and Starbucks’ market share in China may have nowhere to go but down. After all, it’s hard to improve on 75% market share in a highly competitive industry.

That’s especially true if a preference for local stores, or at the very least Chinese chains, occurs in the future. The point is that Starbucks investors can’t expect a booming China to drive strong and consistent sales and earnings growth forever.

Overall, Starbucks’ days of rocket-like earnings growth are likely behind it, and the company may have a harder time achieving its long-term growth targets than management currently expects.

That’s especially true given that Starbuck’s sales and earnings will always be impacted by factors outside the company’s control, including volatile commodity prices and fluctuating foreign currency rates. In fact, as overseas sales become a larger and larger part of the overall business, foreign currency risk will only grow over time.

Closing Thoughts on Starbucks

Starbucks has proven itself very good at building one of the world’s most premium brands and quickly growing while adapting to various challenges over time. More importantly, the innovative company appears to have a solid plan to continue rewarding income investors with double-digit dividend growth for the foreseeable future.

While the risks facing Starbucks’ growth are very real, the management team is very experienced and seems likely to continue finding success in expanded the company’s global reach and store concepts.

To learn more about Starbucks’ dividend safety and growth profile, please click here.

Leave A Comment