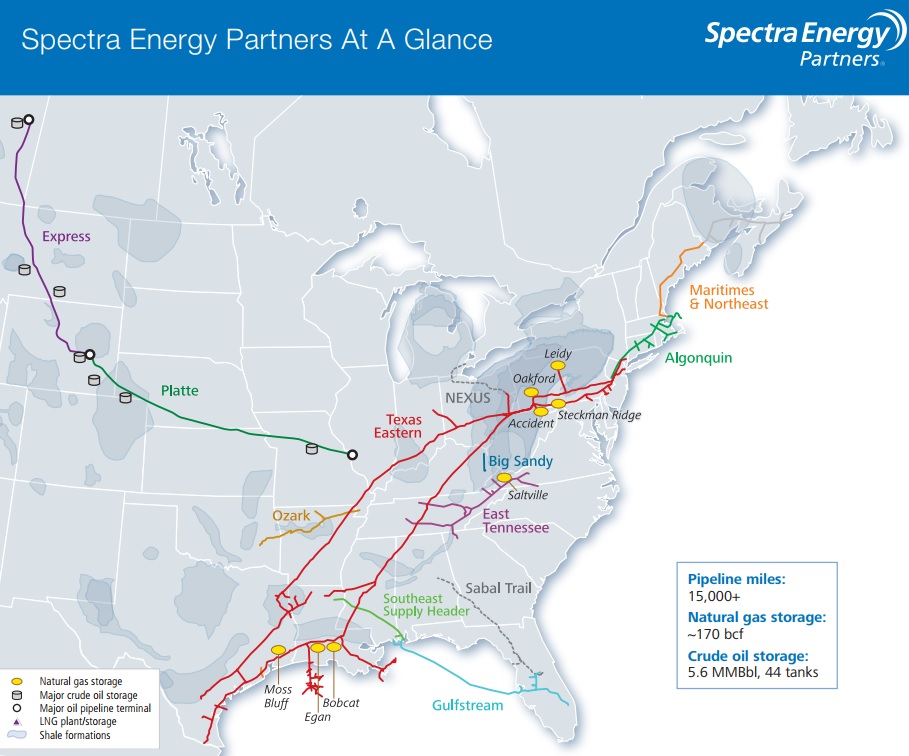

Spectra Energy Partners (SEP) is one of America’s largest midstream master limited partnerships, or MLPs. Its assets include 170 billion cubic feet of natural gas storage, 5.6 million barrels of crude oil storage, and approximately 16,000 miles of gas and oil pipelines that connect producers, consumers, and exporters with some of North America’s most important energy regions, including:

- The Eagle Ford oil shale formation of Texas

- The Marcellus/Utica shale gas fields of Ohio, Pennsylvania, and West Virginia

- The tar sands oil reserves of Alberta, Canada

The heart of Spectra’s pipeline system is the Texas Eastern natural gas transmission system, which moves an estimated 10% of the nation’s gas and serves 120 million people across 16 states, according to Morningstar.

This system connects the booming gas fields of East Texas and the Marcellus/Utica shale to high demand regions such as the North East. Cities such as Boston, Philadelphia, and New York City have some of the nation’s highest gas prices and are in need of lower cost alternatives.

Spectra is also a major gas supplier to the fast-growing state of Florida, where its Gulfstream pipeline supplies most of the states winter heating needs and provides the majority (75%) of gas for its natural gas power plants. In fact, over 60% of all of Florida’s gas demand is serviced by Spectra’s pipelines, which have an average of 13 years remaining on their fixed-fee and inflation-adjusted contracts.

Overall, approximately 82% of Spectra’s EBITDA is generated from its U.S. Transmission business, which provides transmission and storage of natural gas for customers throughout the northeastern and southeastern U.S. Spectra’s Liquids business transports crude oil for customers in the central U.S. and Canada and accounts for the remaining 18% of EBITDA.

On January 22, 2018, Spectra and Enbridge Inc (ENB), which serves as Spectra’s sponsor and general partner, announced an agreement in which Spectra would buyout Enbridge’s general partner stake and incentive distributions rights in exchange for additional units worth about $7.2 billion.

This was done to simply the MLP’s capital structure, permanently lower its cost of capital, and allow for longer and stronger payout growth in the future. After this deal, Enbridge now owns 83% of Spectra’s units.

Business Analysis

There are three main factors that make Spectra a potentially appealing high-yield income growth investment.

First, the company’s business model enjoys a wide moat, because building new pipelines is both expensive (up to $6 billion each) and time consuming (average regulatory approval takes three years). The midstream industry is also one with highly stable and recurring cash flow.

Interstate pipelines are regulated by the Federal Energy Regulatory Commission, or FERC, which approves new pipelines and monitors the methodology used to set pipeline rates. This essentially means that Spectra has a near monopoly on many of its interstate routes and has been able to consistently enjoy setting strong market rates (far above its costs of capital) without a single FERC review for over 25 years.

The midstream MLP industry essentially serves as a toll booth for energy, with cash flow locked in under long-term, fixed-fee contracts with very little exposure to commodity prices.

Spectra takes that low-risk business model to another level, because the MLP is a 100% pure-play toll operator, with absolutely no direct commodity price exposure whatsoever. In addition, the duration of its contracts are six to 17 years (the longest is 25 years), with a weighted average remaining contract representing nine years of fixed and inflation-adjusted cash flow.

Importantly, the majority of Spectra’s revenue is from investment grade or equivalent customers, mostly large utilities who are largely price insensitive and primarily concerned with reliable access to gas.

This is why, despite the worst oil crash in over 50 years (late 2014 to early 2016), when oil prices plunged more than 75%, Spectra’s revenues and cash flows actually continued to rise.

In fact, in the last decade the MLP has never seen a year of falling revenue, and it was able to continue raising its distribution during any economic, interest rate, or energy price environment, including the financial crisis.

This impressive growth, including 10 consecutive years of raising the distribution every single quarter, is due to Spectra’s experienced, disciplined, and long-term focused management team.

Specifically, Spectra avoided the mistake that many midstream MLPs made during the oil boom times (when oil was over $100 per barrel), which was paying out close to 100% of cash flow and funding growth through taking on excessive debt. The company kept its distributable cash flow payout ratio near 80% or below each year.

The company has also been very conservative with how quickly it grows. That includes retaining between 17% and 39% of cash flow each year to internally fund its growth projects, compared to the average MLP which retains only about 5% to 10%.

In addition, Spectra has always been very careful to avoid too much debt (excess leverage caused many payout cuts at other MLPs during the oil crash). For example, the partnership’s leverage ratio (Debt/EBITDA) is just 4.1, with management having a long-term target of 4.0.

That’s in contrast to the industry average of 6.4, showing that Spectra has a very strong balance sheet. As a result, the company has a BBB+ credit rating (tied for the highest in the industry) and is able to borrow at an average interest rate of just 3.5%.

Note that in 2018, Spectra’s DCF payout ratio is expected to jump significantly due to the MLP buying out Enbridge’s incentive distribution rights fees and general partner stake. However, this is actually a smart move for the long-term.

Incentive distribution rights, or IDRs, are designed to give the sponsor of an MLP an incentive to grow the payout quickly. In this case, Spectra’s IDRs mean that 50% all marginal distribution growth goes to Enbridge (about $460 million in 2018) instead of Spectra’s common unit holders.

However, with Spectra buying out these IDRs for a very reasonable 15.7 times 2018’s IDR fees, (most IDR buyout multiples are 15 to 20), the companywill no longer have to split its payout increases between Enbridge and its public investors.

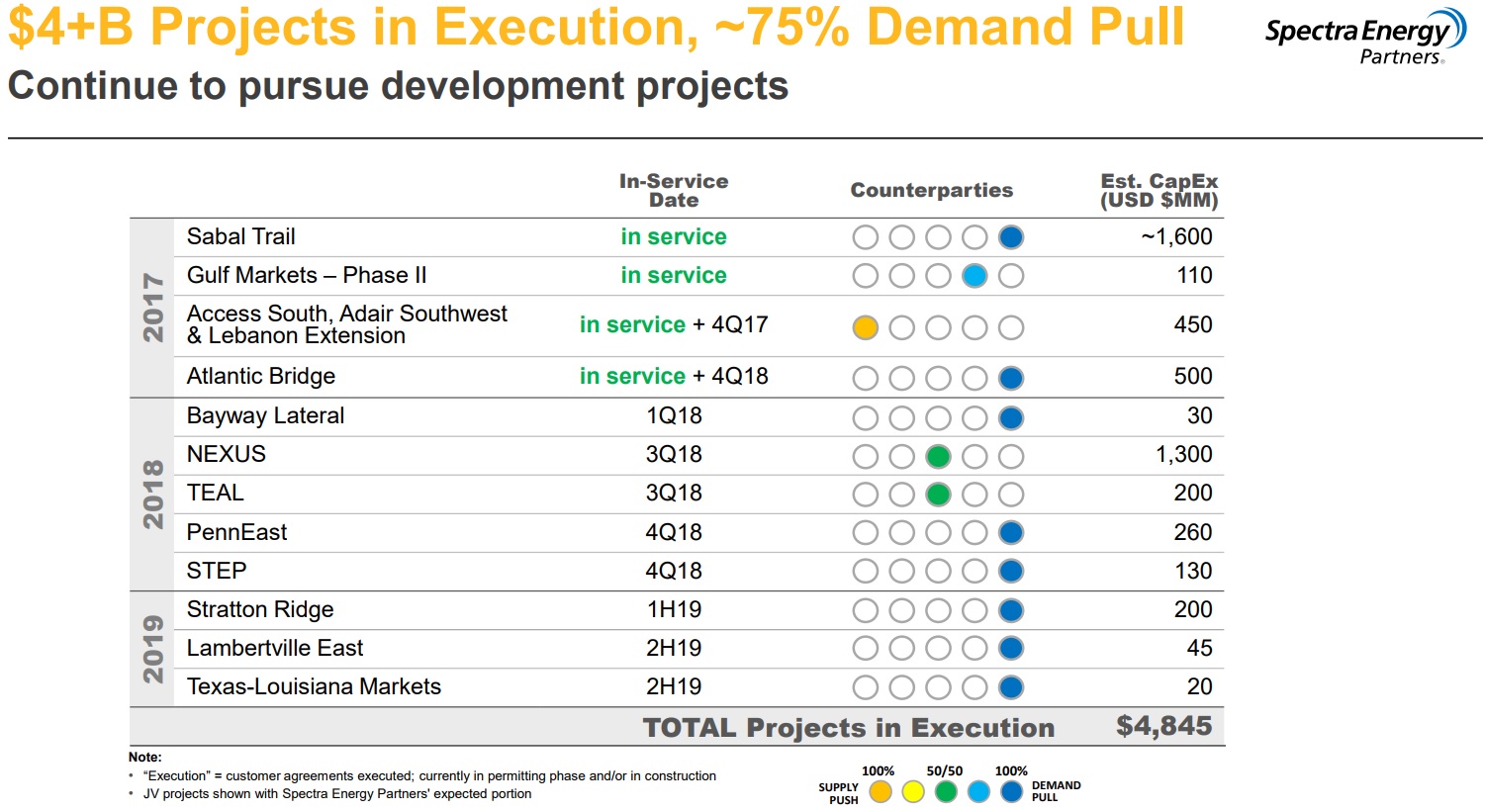

As a result, the firm’s relatively low cost of capital will fall further. This in turn will mean that Spectra will be able to pursue more profitable and larger growth projects in the future, beyond the over $4 billion in projects already under development, including $2 billion in 2018.

More importantly it means that Spectra will be able to grow its distribution faster, more safely, and for longer. Management is expecting to grow the payout at 4% to 6% through 2020 while maintaining an average distributable cash flow payout ratio of about 85%.

Analysts believe that Spectra will be able to continue this pace of payout growth for far longer (through the next decade), due to the continuing U.S. energy boom.

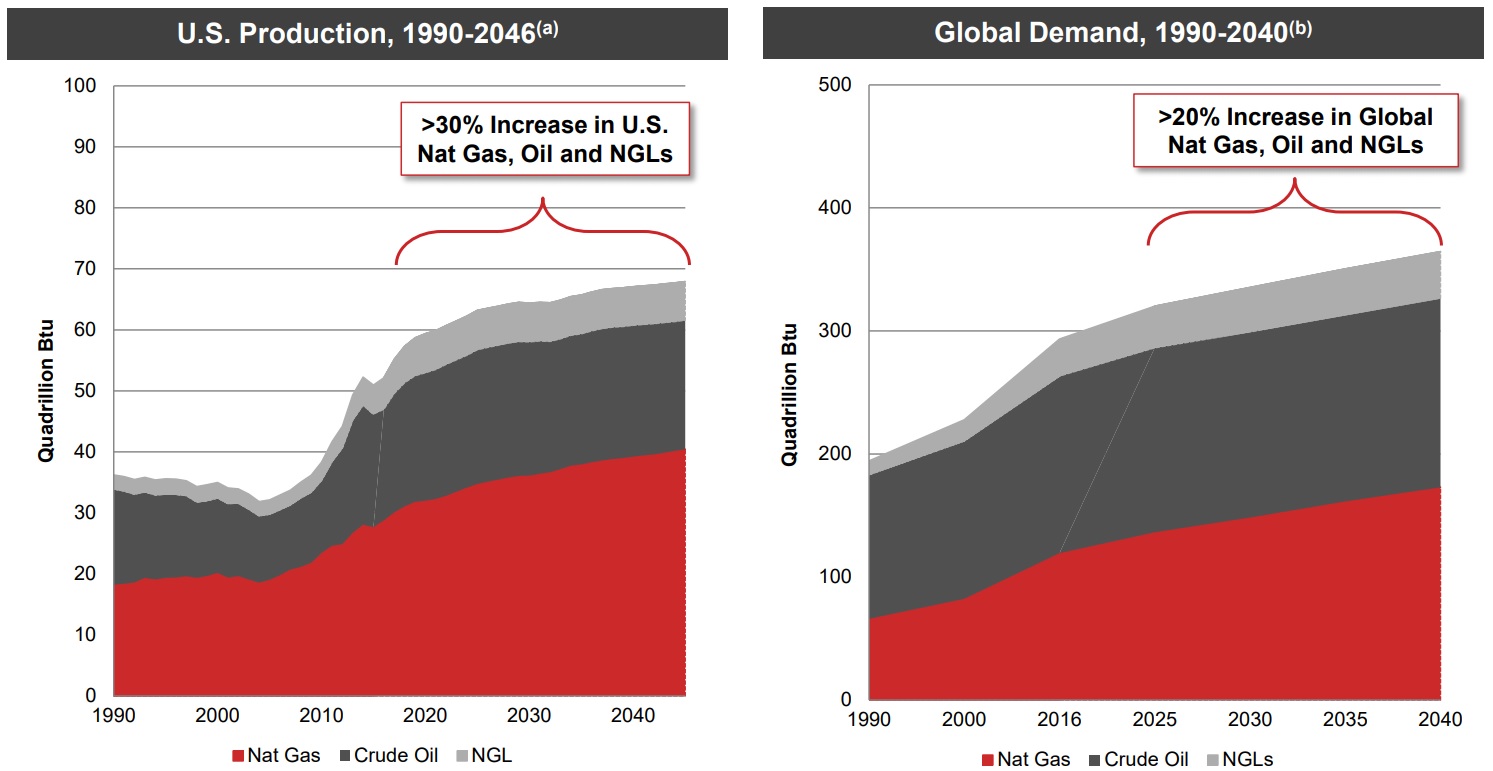

In fact, the U.S. recently hit a new record in oil production, 10.1 million barrels per day, which is expected to eventually rise to 12 million. That would be more than Russia or Saudi Arabia, making the U.S. the world’s largest oil producer.

The Energy Information Administration expects that, despite growing use of renewable energy, global demand for oil & gas will continue to rise through at least 2040. The U.S., with its plentiful and low cost shale oil & gas reserves, is expected to be one of the largest suppliers of this rising demand.

Importantly, Spectra’s key natural gas markets – the northeastern, the southeastern and Gulf Coast regions of the United States – are projected to continue to exhibit higher than average annual growth in natural gas demand versus the U.S. average growth rate through 2020. This demand growth is primarily driven by the natural gas-fired electricity generation sector and Gulf Coast exports of natural gas and LNG (liquefied natural gas).

Not surprisingly the International Energy Agency projects that $700 billion to $900 billion in new U.S. midstream infrastructure will need to be built by 2040 to support this increased production. As a result, Spectra Energy, with its new, lower-cost capital structure and conservative business model, seems poised for many more years of highly secure and stable payout increases.

However, while Spectra Energy appears to be a lower risk choice for high-yield investors, there are certain risks to be aware of.

Key Risks

First, as with all MLPs, be aware that there are some tax complexities involved. Specifically, this means that MLPs are best owned in taxable, not retirement accounts.

That’s because distributions from MLPs are treated as a return of capital, meaning that rather than pay taxes on them they lower your cost basis, potentially to zero. Beyond that they are taxed as long-term capital gains (15% to 20% for most people).

In an IRA or 401K, you don’t get this deferred tax benefit (since you pay no taxes on distributions). In addition, MLPs generate something called UBTI (unrelated business taxable income). If your account generates over $1,000 of UBTI, then you need to report it to the IRS and pay taxes on it.

As for risks specific to Spectra Energy Partners, there are several to keep in mind. First, as with all pipeline stocks, there is the risk that growth projects can become bogged down in regulatory approval, especially if environmental groups of local or state governments object to them. Fortunately, Spectra’s largest networks are in Texas, where its intrastate pipelines face friendly regulators who are very supportive of the energy industry.

In addition, accidents and natural disasters (such as hurricanes) can temporarily shut down a pipeline and reduce cash flows to the MLP. However, Spectra’s highly diversified network provides good cash resiliency, meaning that such events pose only a small risk to the safety of the distribution.

There is also some concern, as outlined by The Wall Street Journal, that tax reform might end up hurting some MLPs. This is because one of the pricing models FERC uses for pipeline rates is a cost model, which includes tax expenses. So with taxes now lower, the regulatory agency has requested 13 MLPs to review their rate structures.

Spectra largely operates on a market-based and negotiated model, and FERC’s jurisdiction only applies to interstate pipelines, not its large network of intrastate assets. As a result, while there is still some risk that Spectra will have to lower some of its pipeline fees, for the most part its cash flows should be largely immune.

And with all highly capital intensive industries that rely in large part on debt and equity markets to raise growth capital, there is a risk that rising interest rates could potentially raise the MLP’s cost of capital. This might lower the profitability of future growth projects, hurting both cash flow and distribution growth rates.

Fortunately, Spectra’s industry-leading balance sheet and conservative use of debt should continue to ensure it access to cheap debt, even if long-term rates rise. And while there is a risk that a low unit price could make its cost of equity rise, keep in mind that MLPs who don’t have IDRs usually trade at a meaningful premium to their rivals.

In other words, Spectra’s strong balance sheet and IDR buyout has positioned it well to have a cost of capital advantage over its peers and continue growing for many years to come. That’s even in a world of higher interest rates.

Finally, it should be noted that while midstream stocks make for great long-term income growth investments, they are likely to have a finite lifespan. This is because the world is gradually moving towards a renewable energy model that will, one day, cause the demand for midstream infrastructure to peak and decline.

Analyst firm McKinsey estimates that in 2050 oil & gas will still supply 72% of the world’s energy needs, compared to 84% today. However, they also project that global peak oil demand might occur faster than expected, as early as 2030.

In other words, the U.S. energy boom, which is what is expected to power the growth of midstream MLPs like Spectra for decades, might not be as long lived or as strong as many investors hope.

Closing Thoughts on Spectra Energy Partners

The oil crash revealed that some midstream MLPs were not nearly as secure an income source as many investors believed. However, blue chips like Spectra Energy Partners, with their disciplined management teams, strong balance sheets, and slow but steady payout growth, continued to prosper throughout the worst industry downturn in over half a century.

Going forward, the partnership expects reasonable distribution coverage of 1.1x to 1.2x through 2020 and should continue to benefit from providing essential services that connect diverse, low-cost supply basins with regional demand markets.

While Spectra does face certain industry-specific risks and challenges, it appears to be one of the better choices for income investors looking to purchase relatively safe, high-yield stocks in the MLP industry.

To learn more about Spectra Energy Partners’ dividend safety and growth profile, please click here.

Leave A Comment