Buckeye Partners (BPL) traces its roots back to 1886 as the Buckeye Pipe Line Company, part of John D. Rockefeller’s Standard Oil empire. Over 30 years ago the business changed its corporate structure to that of a master limited partnership (MLP).

Today Buckeye Partners operates a global portfolio of petroleum and petroleum product pipelines and storage terminals. The partnership organizes its operations into three business segments:

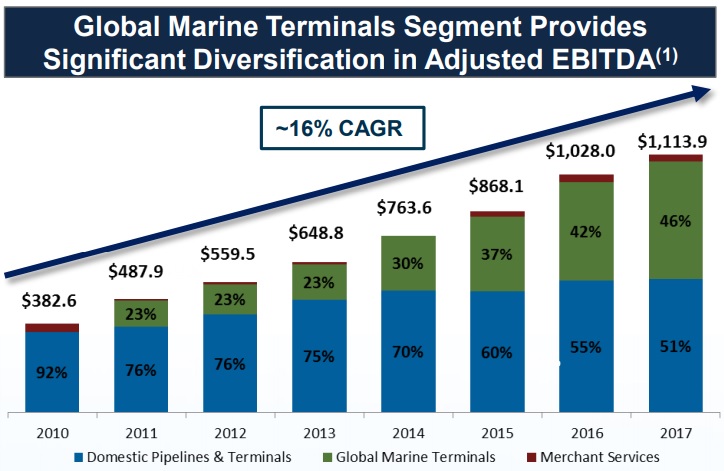

- Domestic Pipelines & Terminals (51% of 2017 Adjusted EBITDA):6,000 miles of petroleum products pipelines and 115 product storage terminals with 57 million barrels of capacity.

- Global Marine Terminals (46% of 2017 Adjusted EBITDA): 22 storage and import terminals, with 120 million barrels of storage capacity. These terminals are designed for oil import/export and are capable of handling the largest oil tankers in the world.

- Merchant Services (3% of Adjusted EBITDA): markets refined products in areas served by its domestic pipeline network.

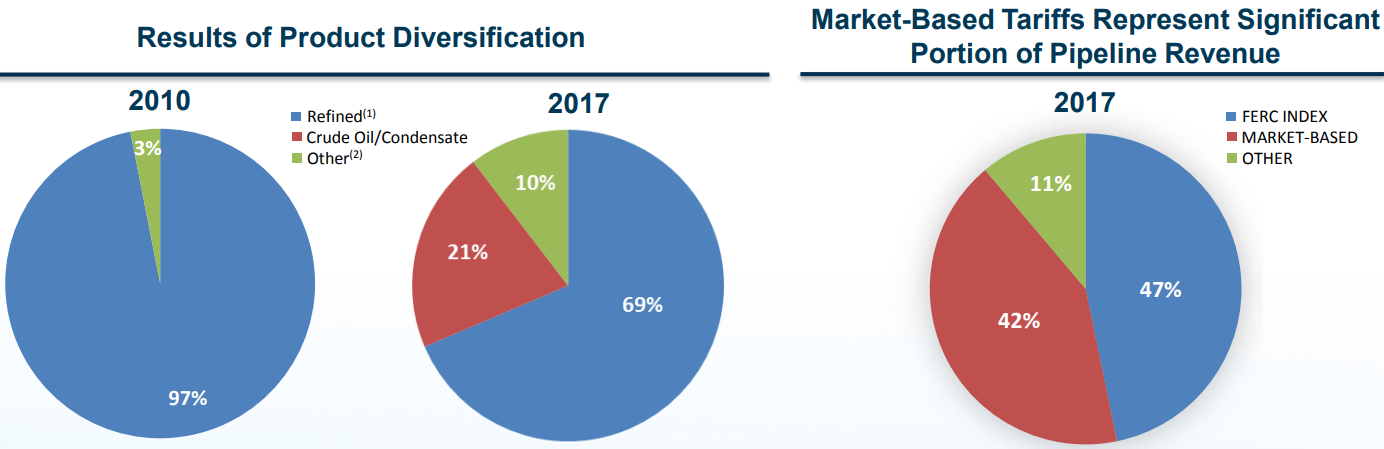

Approximately 95% of Buckeye’s cash flow is derived from fixed-fee contracts, which have always been the core of the MLP’s focus. However, in recent years the MLP has transitioned from predominantly refined product pipelines regulated by FERC (Federal Energy Regulatory Commission) to market-based rates on terminal storage facilities.

Business Analysis

Midstream MLPs like Buckeye provide the gathering, storage, processing, and transportation infrastructure that enables the oil & gas industry to function. The business model is similar to a toll road, with most cash flow derived from fixed fee contracts, often with minimum volume guarantees.

This deal structure helps ensure highly predictable cash flow from which to fund the distribution (the equivalent of a dividend for an MLP), and barriers to entry are sizable in this industry.

Pipeline are typically the lowest cost method for long-haul overland movement of liquid petroleum products. Constructing major pipelines can cost upwards of several billion dollars, take several years of time, and require strict compliance with various regulatory bodies.

Only so many pipelines are needed in any one energy-producing region as well, which tends to limit new entrants since the incumbents have already locked down the necessary relationships across the supply chain (energy producers through energy consumers).

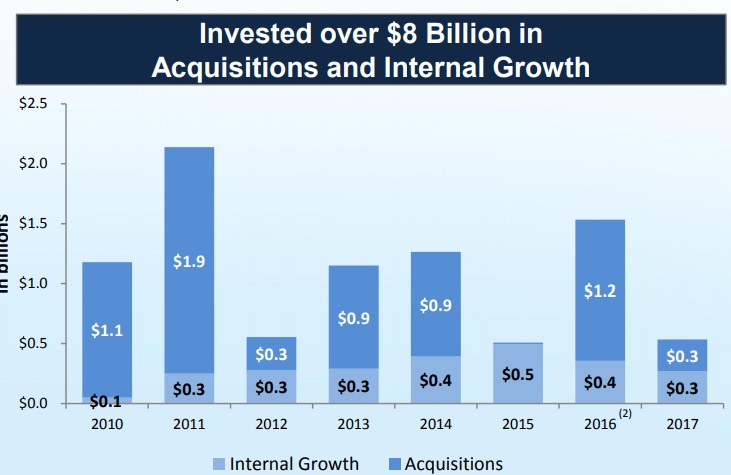

Buckeye began its life as an MLP with nearly an exclusive focus on the U.S. refined pipeline market. However, since 2010 the MLP has invested over $8 billion into growing its asset base, including diversifying into marine oil storage facilities.

Similar to pipelines, the marine terminals business enjoys several advantages that result in high barriers to entry. First, there are only so many major energy hubs that can support having a terminal located nearby.

Besides geographic constraints, constructing a new terminal typically costs hundreds of millions of dollars and must undergo a lengthy permitting and development cycle. With only so many sites suitable for development, the incumbents have strong market positions.

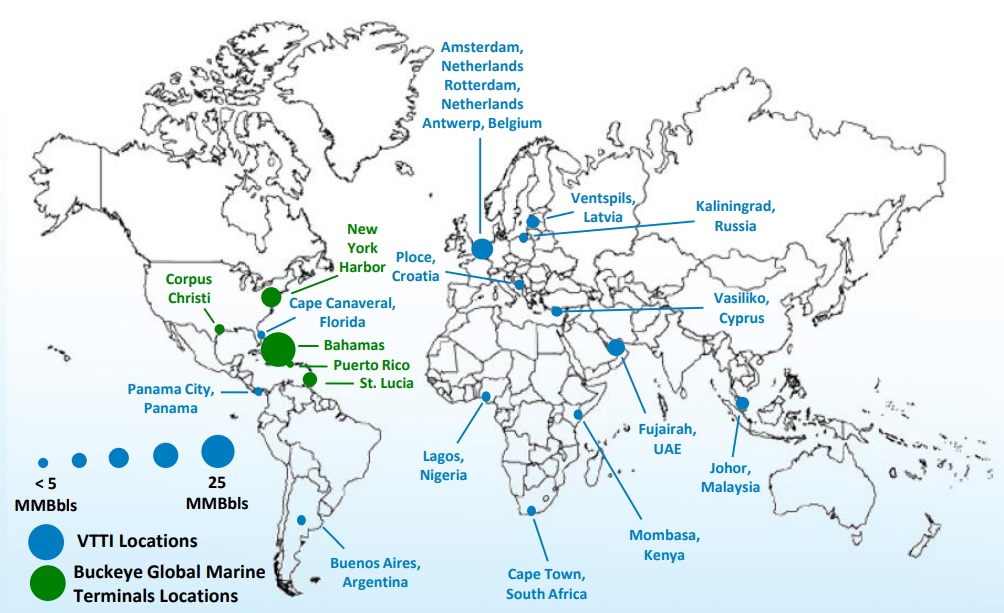

A large part of Buckeye’s diversification into the marine terminals business was the company’s $1.2 billion partnership with Vitol, a large Dutch owner of global oil storage and import/export facilities, in 2017. Specifically, Buckeye bought a 50% stake in VTTI, the marine storage business. In September 2017, Vitol and Buckeye bought out VTTI’s MLP, VTTI Energy Partners, for $476 million in cash.

The VTTI deal added 15 global marine storage and import/export terminals to the MLP’s existing five storage facilities. In addition, there are two new facilities under construction in Panama and Croatia, as well as planned expansions of VTTI’s terminals in Antwerp and Rotterdam. The MLP also plans to break ground soon on a new storage facility in South East Asia.

Going forward, Buckeye has two primary long-term growth catalysts. The first is in the U.S., where it hopes to serve the fast-growing needs of the U.S. shale industry.

According to the International Energy Agency, U.S. oil production is expected to rise about 20% by 2023, increasing from its record level of 10 million barrels per day to 12 million barrels per day.

This would make America the world’s largest oil producer. Higher production is expected to also increase U.S. exports from their current level of about 2 million barrels per day to 5 million barrels per day, second only to Saudi Arabia.

U.S. refining capacity is expected to see significant increases as well, with companies like Exxon Mobil (XOM) planning large investments in expanded and new refinery capacity to make use of this flood of U.S. crude.

Meanwhile, increased U.S. oil exports are similarly expected to fuel strong demand for storage and export facilities. Buckeye has numerous new projects underway to capitalize on these trends, including the Southwest Texas Gateway. This is a major pipeline project connecting the booming Permian basin in West Texas to Corpus Christi’s export facilities.

In addition, the MLP has expansion projects underway for refined product pipelines connecting Midwest refineries to major markets in Pennsylvania. Buckeye also is working on expanding its storage facilities in Chicago, the major hub for refined products in the Midwest.

Finally, there are ongoing expansion plans for numerous projects in Florida, New York State, and Pennsylvania. All told the MLP expects to invest $275 million to $325 million in growth projects in 2018.

Overall, demand for Buckeye’s pipelines, storage facilities, and terminals should presumably rise over the years ahead as more products need to be moved from shale production fields to their end destinations around the world. High and steady U.S. oil production will be a key driver.

The company’s global oil storage business has particularly attractive growth potential. That’s because numerous industry studies project that global oil demand is likely to continue rising through at least 2040. In fact, Exxon Mobil thinks that world oil consumption will rise about 20%, or 20 million barrels per day, by that time, and it will need to be held somewhere.

Simply put, Buckeye Partners appears to have a large number of growth projects to pursue going forward. Combined with one of the industry’s top income track records, including 22 consecutive years of annual payout increases and over 30 years of uninterrupted quarterly distributions, one might think that this MLP is a good long-term income stock.

However, Buckeye Partners faces numerous major risk factors that mean it might not be able to execute on its growth potential. In fact, there are several reasons to worry that the distribution will not only grow far more slowly in the future, but its current level may even prove to be unsustainable.

Key Risks

Part of the appeal of the MLP industry is that interstate pipelines, which make up about half of Buckeye’s business, are regulated and thus usually enjoy strong price stability (as long as their customers can pay).

However, this can also act as a double-edged sword. In March 2018, FERC, the key regulator for pipelines, announced it was reversing a 2005 tax ruling to no longer allow interstate pipelines owned by MLPs to recover an income tax allowance in the cost of service customers previously had to pay for.

As pass-through entities, MLPs do not pay any federal taxes. In other words, they were essentially getting a double benefit on taxes, which is now being taken away and could reduce cash flow. The policy revision only affects interstate oil and gas pipelines and will not go into effect for oil pipelines until 2020 since they are regulated differently.

Fortunately, the rule only applies to cost-of-service contracts, and not the negotiated market rates that represent most of Buyckey’s affected pipelines.

In addition, FERC has no jurisdiction over marine terminal storage, which is a major focus of the MLP’s future growth efforts. This is why the MLP has announced that it anticipates no material impact to its cash flow from the rule change.

However, this event, which sent the entire MLP industry into a brief panic (with some prices plunging nearly 20% on the announcement), clearly illustrates the danger that regulatory changes can create. Investors in this space must realize that future rate/tax policy shifts could negatively impact the entire industry.

Buckeye Partners faces two other major risks in the future as well. First, despite an impressive record of distribution increases over the decades, the MLP has a bad habit of retaining little to no cash flow to invest in future growth.

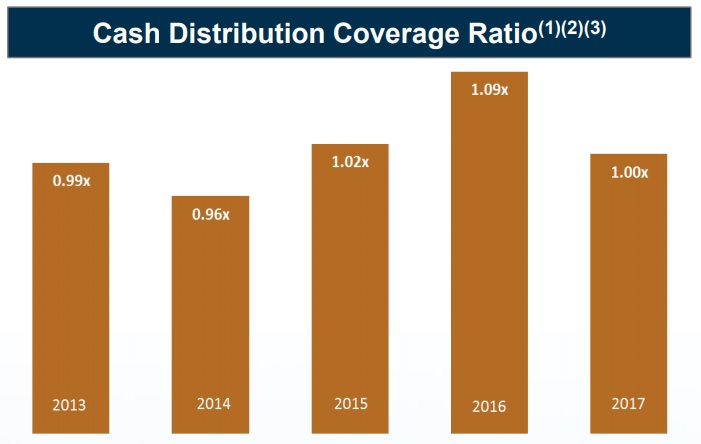

For example, Buckeye’s distribution coverage ratio, which measures the ratio of distributable cash flow to distributions paid, has spent the last five years dangerously close to 1.0. In the MLP industry, a ratio of 1.1 is considered the minimum level needed for a sustainable and somewhat secure payout that’s also capable of continued growth.

Buckeye’s distribution has been using up virtually all of the partnership’s distributable cash flow in recent years. As a result, the MLP has had to fund its growth nearly entirely with debt and equity financing. When combined with Buckeye’s desire to maintain its streak of 22 years of consecutive annual payout growth, there is very little margin for error.

It’s true that MLPs were designed to pay out the majority of their cash flow as distributions and grow through the use of accretive (relatively cheap) debt and equity issuances. However, most MLPs retain at least 10% to 20% of cash flow to decrease their reliance on fickle capital markets.

Since the 2015 oil crash, the worst in over 50 years, MLP unit prices have been much lower than in the past. This has raised Buckeye’s cost of equity to increasingly dangerous levels.

For example, in 2017 it sold $346 million in new stock, increasing the unit count by about 7% and causing the MLP’s payout coverage ratio to fall to dangerous levels. Management was forced to freeze the distribution, so Buckeye investors are now unlikely to get increasing payments for the first time in 23 years.

Today the unit price has fallen to around $40, pushing BPL’s dividend yield above 12% and representing a very steep cost for the company to issue new units in the future. In order to continue growing, the MLP has had to resort to more expensive and non-standard financing.

For example, in January of 2018 the MLP issued a $400 million 60-year junior bond. The initial interest rate is fixed at 6.4% through January of 2023, after which it becomes a floating rate loan with an interest rate of 3-Month LIBOR plus 4.02%.

LIBOR is the London Interbank Offer Rate, which is set by 18 global banks on a daily basis. It represents the banks’ cost of borrowing from each other, and many U.S. corporate loans are indexed to it.

The 3-month LIBOR is currently around 2.1%. Should interest rates rise significantly, Buckeye could be facing steep rates above 8% on this bond by 2023. The bonds are redeemable by the company beginning in 2023, but it’s hard to say what financial condition Buckeye will be in, as well as the state of capital markets.

On the equity side of the capital equation, the situation is also looking increasingly challenging. In 2017, the MLP sold $265 million of class C units, with an option for buyers to buy another $50 million later. The distributions on these units are not paid in cash, but rather in additional units.

This helps Buckeye in the short-term because it can raise growth capital without increasing the cash cost of its distribution. However, the problem is that these units are scheduled to convert to regular LP units, which are paid in cash, in two years.

In other words, Buckeye investors are potentially looking at about 6% to 7% additional dilution by the end of 2019. With the coverage ratio in Q4 2017 already a tenuous 1.01, the MLP is racing against time to grow its distributable cash flow just so this impending dilution doesn’t make the current payout unsustainable.

In addition, be aware that Buckeye’s big push to diversify into global oil storage terminals may also backfire. In recent years the worldwide supply glut of oil has meant very strong demand for crude storage facilities.

However, in 2016 OPEC partnered with Russia to impose 10% production cuts that have continually been extended. Those cuts are now set to expire by the end of 2018 but resulted in decreased global oil production to about 97 million barrels per day.

Demand for oil has continued to rise. The International Energy Agency expects 2017 global oil demand grew to 99.3 million barrels per day, driven by strong consumption from China and India.

With demand exceeding supply, oil inventories have started to shrink. This is why Buckeye’s oil storage utilization rate has fallen from 99% in 2016, to 92% in 2017, with Q4 2017’s levels coming in at just 88%.

Oil storage contracts are short term and reset far more frequently than pipeline contracts. This means that Buckeye’s major recent acquisitions, for which it heavily diluted existing investors, could become far less profitable in the coming years.

Since Buckeye’s top three oil storage customers represent close to 60% of that segment’s revenue, they may have a stronger bargaining position to negotiate lower rates in the future.

Meanwhile, Saudi Arabia has stated that it wants to maintain the OPEC cuts far beyond 2018, in order to boost global oil prices from $65 per barrel to $70 per barrel over the long term. Russia has indicated that it is amenable to doing this, too.

Should the production cuts be extended for several years, then Buckeye’s oil terminal business could suffer ongoing declines in cash flow, at a time when the MLP’s distribution appears to have no margin of safety.

While Buckeye Partners does maintain an investment grade credit rating for now, its BBB- rating is just one level above junk bond status. The company faces higher borrowing costs than many larger blue-chip MLPs, who have stronger balance sheets.

Management’s insistence on continuing the distribution for now will require Buckeye to take on ever-increasing debt, which could ultimately jeopardize its credit rating as well.

In addition, BPL’s very low unit price means the partnership appears to be facing an equity liquidity trap. In other words, it can’t sell new units at a high enough price to make its planned growth investments profitable.

Even with a strong long-term growth potential, Buckeye will likely struggle to invest profitably based on its current cost of capital, meaning that DCF per unit could grow very slowly.

In fact, analysts currently project just 1% DCF per unit growth over the next decade. With a large convertible equity cliff coming, Buckeye’s distribution could become unsustainable by as early as 2020, potentially forcing a payout cut.

For now, management is determined to maintain its distribution in 2018, even despite the company’s coverage ratio dipping below 1.0. Here’s what CEO Clark Smith said during Buckeye’s fourth quarter conference call:

“Looking forward, during 2018, there may be periods where our distribution coverage falls below 1x. However, based on our longer-term outlook, a temporary shortfall in coverage will not affect our distribution policy. Our management team and board views a distribution reduction as an optional last resort.

While decisions on distribution policy are made on a quarterly basis, Buckeye currently has no intention to cut its distribution. Our performance over the past decade across the significant volatility in the crude oil commodity markets and during both contango and backwardation storage conditions have demonstrated the value of our diversified asset base and the stability of our fee-based cash flows.”

While many other MLPs are now focused on deleveraging, self-funding much of their growth, and lowering their payout ratios, Buckeye Partners seems determined to maintain its current course and push its financial limits to the brink of sustainability.

This seems like a risky capital allocation decision that could get the company into deeper trouble in the years ahead.

Closing Thoughts on Buckeye Partners

Buckeye Partners is one of the oldest MLPs in America, with roots going back more than 130 years. Over time the partnership has proven to be one of the most consistent distribution growers in its industry. And the continued rise in global oil demand, U.S. shale oil production, and export activity all represent potentially large growth catalysts for the MLP.

That being said, Buckeye’s policy of prioritizing consistent distribution growth at the expense of its coverage ratio has put the MLP in a liquidity trap that makes the safety of the payout highly suspect over the next few years.

So despite the MLP’s impressive track record thus far, Buckeye’s future status as a dependable income stock could be jeopardized. Conservative investors should probably avoid the stock altogether.

For investors who are still determined to invest in MLPs, Enterprise Products Partners (EPD) and Magellan Midstream Partners (MMP) could be more appropriate candidates to consider.

To learn more about Buckeye’s dividend safety and growth profile, please click here.

very thorough