Founded in 1869, Royal Bank of Canada (RY) is Canada’s largest bank by assets (about $1 trillion) and one of the 15 largest global banks by market cap. The firm is well-diversified across businesses, geographies and client segments, serving 16 million customers worldwide in Canada, the U.S., and 35 other countries. Royal Bank of Canada provides its services via a network of approximately 1,350 branches and more than 4,600 ATMs.

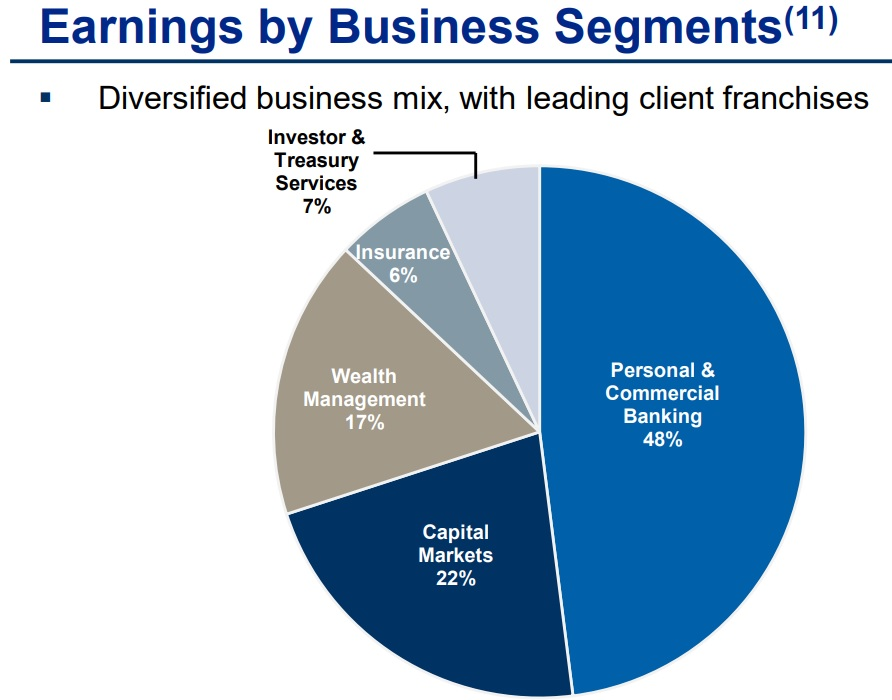

The company operates under five business segments:

- Personal & Commercial Banking (48% of earnings): provides personal (72% of segment revenue) and business banking services (22%), as well as auto financing and retail investment products. These offerings are provided through the company’s branch locations, ATMs, online channels, mobile app, and telephone banking networks, as well as through sales professionals. The firm has No. 1 or No. 2 market share in all key Canadian banking product categories.

- Capital Markets (22% of earnings): offers corporate and investment banking, as well as equity and debt origination, distribution, and structuring and trading for public and private companies, institutional investors, governments, and central banks. Royal Bank of Canada is the 10th largest investment bank in the world by fee revenue.

- Wealth Management (17% of earnings): offers a suite of investment, trust, banking, credit, and other wealth management solutions to high net worth and ultra-high net worth clients. This segment also markets asset management products and services directly to institutional and individual clients. Revenues are split almost evenly between retail investors and institutional clients, and Royal Bank of Canada is a top-five wealth manager globally by assets.

- Investor and Treasury Services (7% of earnings): offers asset services, custody, payments, and treasury services for financial and other institutional investors. This segment also provides cash management, correspondent banking, and trade finance for financial institutions.

- Insurance (6% of earnings): provides life, health, home, auto, travel, wealth, group, and reinsurance products and solutions through: retail insurance branches, field sales representatives, advice centers, online channels, and independent insurance advisors. The firm is Canada’s largest bank-owned insurer and among the fastest growing insurance companies in the country.

As you can see below, nearly half of the company’s earnings are from traditional retail banking with less than a quarter coming from the more cyclical capital market segment.

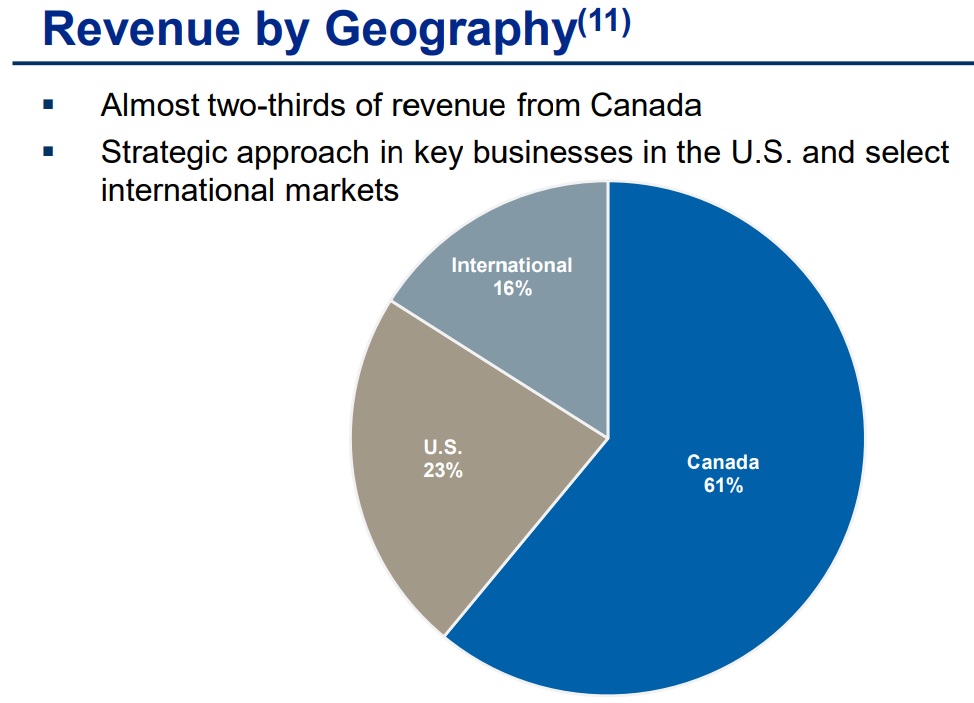

More than 80% of the company’s revenue is derived from North America, with just over 60% from its home market of Canada.

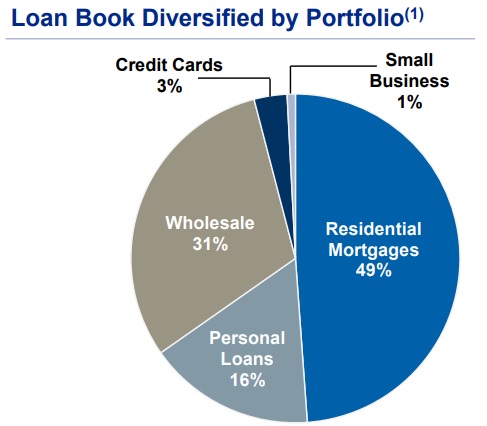

Net interest income from lending operations accounted for 42% of the bank’s revenue in 2017, with non-interest income activities such as investments and insurance operations accounting for the other 58%. On the lending side, residential mortgages account for about half of Royal Bank of Canada’s loan book, representing 21% of the bank’s total assets.

Business Analysis

Banking is largely a commodity product in the U.S., with consumers and businesses seeking access to dependable financing at the lowest interest rate possible. Banks with the largest low-cost deposit bases (i.e. cheap sources of funding to use for lending), most efficient operations, and conservative risk management practices tend to be best off.

Unfortunately, significant regulation and intense competition (there are more than 9,000 U.S. banks) tend to reduce the level of profitability that is possible. However, even stricter regulations in Canada, where Royal Bank of Canada generates over 60% of its revenue, create just the opposite effect.

For example, the Canadian banking sector is known for its stability, even sailing through the global financial crisis with relative ease (no Canadian banks failed or required government bailouts). In fact, Canada hasn’t had a banking crisis since 1840, largely due to strict regulations that cement the largest six banks as an effective oligopoly.

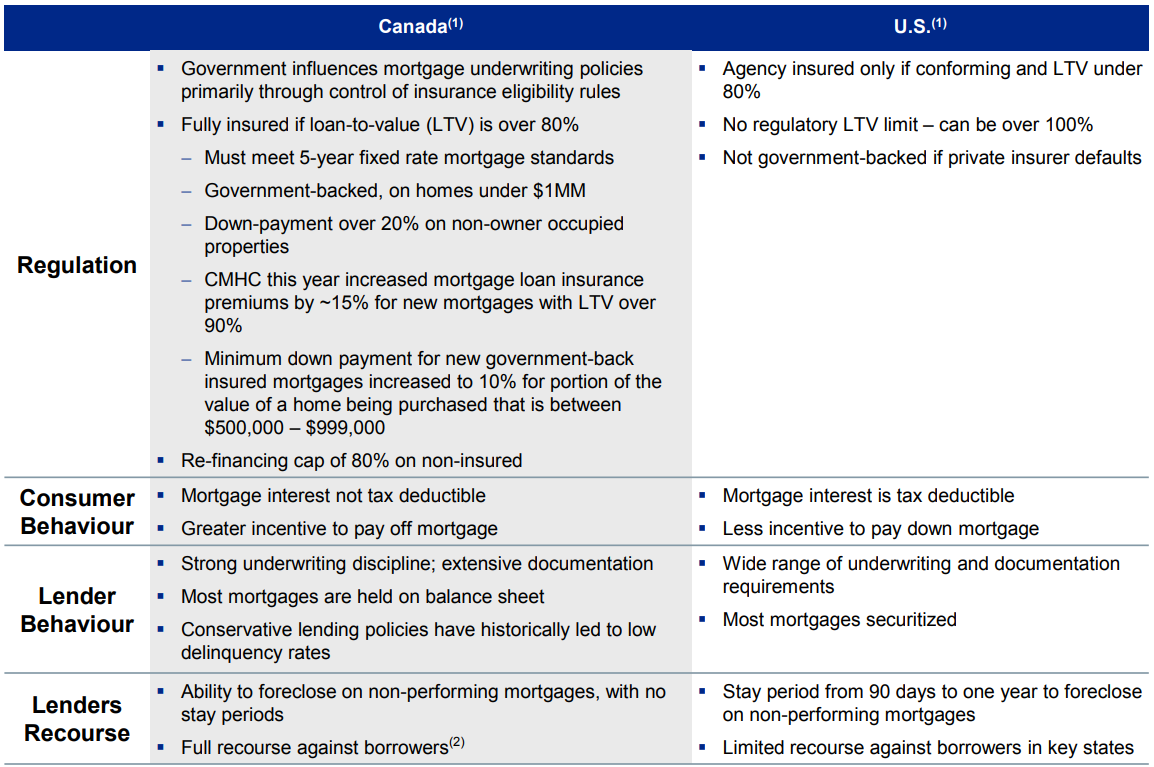

For one thing, Canadian regulators set very strict underwriting and credit standards, while also forcing banks to eat more of their own cooking. For example, Canadian banks are required by law to hold more loans (including mortgages) on their own books, rather than securitize (i.e. sell) them to third parties. As a result, lending practices tend to be far more conservative.

Home mortgages, which account for around 20% of the bank’s assets, also require a minimum downpayment of 5%, and any mortgage without at least 20% down payment requires default insurance.

Besides mortgage rules, stricter credit score lending standards are also in place because the Canadian government insures all home loans under 1 million CAD against default. These conservative practices are one reason why Canadian banks suffered far less than many other financial institutions in 2008-2009.

When combined with their impressive scale and geographic diversification across the country, Canada’s largest banks enjoy durable competitive advantages, despite offering similar products and prices.

These giants enjoy some of the lowest cost sources of funding (massive deposit bases paying little interest), have thousands of retail locations across the country to cheaply acquire new customers, and have expanded their operations into hundreds of different product lines to continue growing. Smaller rivals struggle to compete with the giants’ prices, services breadth, and reputation.

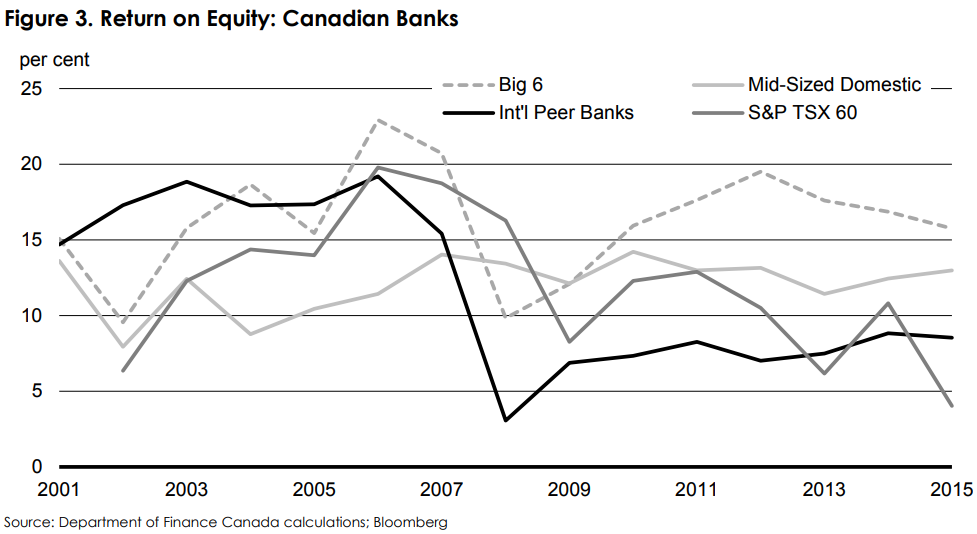

As you can see below, Canada’s big six banks (the dashed line) have generated solid profitability throughout all types of economic environments for many years. They have also earned a superior return on equity compared to smaller Canadian banks, international peers, and the corporate sector overall.

Canadian banks tend to enjoy a much higher return on equity (the key banking profitability metric) than their U.S. counterparts as well. Given the greater number of U.S. banks competing with each other, plus the onerous regulations that were implemented following the financial crisis to reduce risk, most U.S. banks earn a return on equity around 10% to 12%.

While regulations are even stricter in Canada, the major banks here enjoy more meaningful economies of scale and less competition which support a return on equity that is nearly two to three times higher than in the U.S. Part of their higher profitability is due to the low-cost structure of Canadian banks.

A bank’s efficiency ratio (operating costs/revenue) is a key profitability measure, for example. In the U.S., most big banks have efficiency ratios of 55% to 65%, and international banks that hit 60% are considered very lean operations. In Canada, most major banks have efficiency ratios between 50% and 55%.

Royal Bank of Canada recorded an efficiency ratio of 53.5% in 2017, among the lowest of any bank in the world. With No. 1 or No. 2 market share positions in every aspect of Canadian retail banking, the firm enjoys a substantial low-cost deposit base and the industry’s best economies of scale.

The bank’s relatively low operating costs result in far higher profitability than any U.S. bank, with RBC’s overall operations earning a 17% return on equity in 2017. However, its Canadian businesses enjoyed a 33% return on equity, about tripling the profitability norm in America.

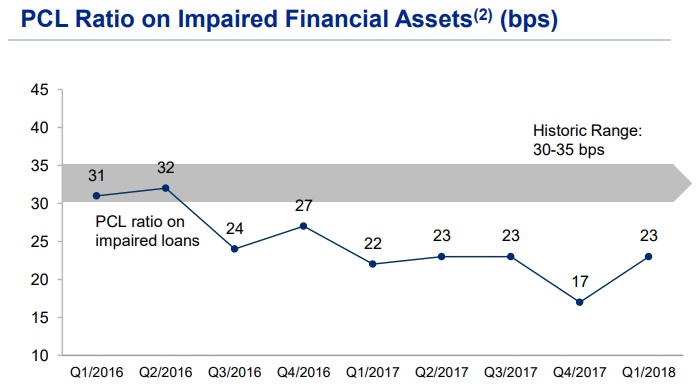

More importantly, management is generating solid profitability without taking on excessive risk. RBC’s loan underwriting is very disciplined and conservative, even more so than what regulators require. This is one reason why the bank’s loan losses are among the lowest in the world, just 0.23% in the first quarter of 2018.

Most importantly, the bank’s balance sheet is very strong with a common equity tier 1 (CET1) ratio of 11.0%. CET1 measures a bank’s common equity (shareholder equity and retained earnings) against its risk-weighted assets. A bank’s CET1 ratio is arguably its most important risk metric.

Under the post-financial crisis Basel III international banking accords, CET1 creates a standardized way of judging how well capitalized a bank is. For context, the U.S. Federal Reserve, which regulated all U.S. banks, has a minimum CET1 requirement of 8.5% to 9.5% (depending on a bank’s size and complexity) to ensure a bank remains safe during another financial crisis.

This number was determined by advanced annual stress tests, which simulate a worse global recession than occured in 2008-2009. It’s now considered a good global banking standard that is likely to result in a large bank being able to weather any economic storm and remain solvent (i.e. not need a bailout).

Canadian bank’s CET1 ratios generally range from 11% to 12%, well above the U.S. and international standards. And those figures are expected to rise somewhat in the future due to new Canadian banking regulations designed to make these banks even more bulletproof. Given RBC’s conservatism with its balance sheet, it’s no surprise that the company earns an AA- credit rating from Standard & Poor’s, one of the highest ratings of any bank in the world.

Outside of traditional retail banking, RBC is also dominant in asset management and investment banking. For example, the firm is the 10th largest global investment bank by fees, a top-five wealth manager globally, and commands 40% market share in Canada’s asset management industry.

RBC has also been making progress expanding its reach in the U.S. market. While more competitive and less profitable due to a different regulatory environment, America has nearly nine times the population of Canada. In the early 2000’s, RBC purchased several regional Southeast banks. However, these firms were badly hurt by the housing crash.

In 2015, RBC refocused its U.S. strategy with its $5.4 billion acquisition of City National Bank. The goal was to use a far more limited and focused approach to U.S. banking, specifically targeting very affluent clientele.

City National serves high net worth and commercial clients across a number of the largest and wealthiest U.S. metropolitan areas, including New York, Los Angeles, San Francisco, and San Diego. However, City National is just one part of RBC’s U.S. strategy, which involves opening more asset management offices in other affluent and fast growing markets.

Technology is expected to play an increasingly important role in helping RBC execute its growth plans and defend its strong market share. In fact, RBC spent CAD 3 billion on technology in 2017, the most of any Canadian bank.

While some of these investments are going into sensitive areas such as cybersecurity, a big focus is on increasing convenience for consumers and businesses in the digital age.

Specifically, the company is investing heavily into online and mobile banking platforms. RBC has more than 6 million active digital users in its Canadian banking businesses, and 84% of its financial transactions were performed in self-serve channels in 2017. Mobile banking is so important because the company expects it to help improve customer service (to help grow or maintain market share) and improve its efficiency rate even further as fewer physical branch locations are needed.

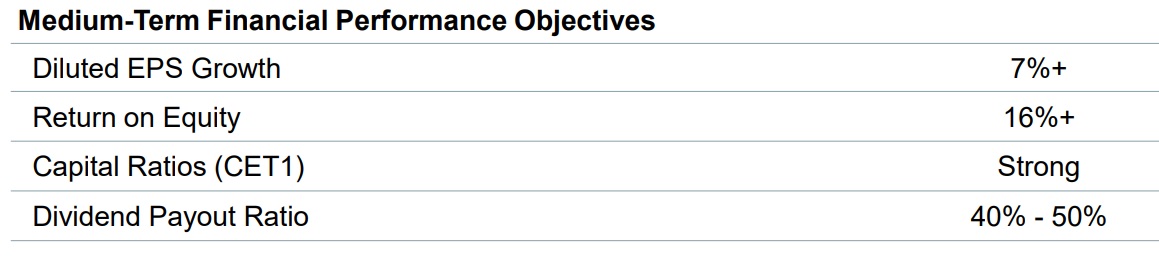

All told, RBC expects its growth and cost cutting efforts to result in at least 7% annual EPS growth over the next few years.

More importantly for income investors, the bank plans to pay out about 45% of its earnings as dividends, as it did in 2017. Management’s target payout ratio appears very reasonable given the bank’s low risk profile, which has helped RBC pay uninterrupted dividends for more than 20 consecutive years. It also suggests that dividend growth will continue tracking earnings growth, just like it has for most of the past decade.

Overall, Royal Bank of Canada is one of the world’s best run, most conservative, and most profitable banks. The firm’s disciplined management team, leading market share positions, low-cost deposit base, diversified portfolio, and technology investments all help ensure that RBC remains a dominant force in banking for many years to come.

However, all banks have certain risks that investors need to be aware of.

Key Risks

First, it’s important to point out that as a Canadian company, RBC pays its dividend in Canadian dollars. This creates some currency risk in that a stronger U.S. dollar might decrease the effective dividend amount for American shareholders, at least in the short term (each quarterly dividend is converted from Canadian dollars to U.S. dollars when it is paid, based on prevailing exchange rates).

In addition, like all Canadian stocks, RBC investors will face a 15% foreign dividend tax withholding, except in retirement accounts such as IRAs and 401Ks. Tax treaties between the U.S. and Canada allow U.S. investors to potentially recoup this withholding, but it can be a complicated and lengthy amount of paperwork at tax time.

As for risks to the bank itself, there are several to consider. Like all banks, Royal Bank of Canada’s earnings are tied to the financial health of the economies in which it operates, with Canada being the most important. And while the bank expects Canada’s economy to continue growing steadily, be aware that the country is somewhat more dependent on volatile natural resources than most developed countries. For example, 11% of Canada’s GDP is derived from the mining, oil, and gas industries, which are tied to cyclical commodity prices.

Canadian consumers are also highly indebted. The household debt/GDP ratio in Canada sits near 100% compared to less than 80% in the U.S., for example. Should the Canadian economy enter a recession, there could be a higher risk of consumer defaults on more loans.

Fortunately, higher default rates are unlikely wouldn’t put RBC at risk of failure. For example, in 2008, 2009, and 2016 (oil crash), the bank’s earnings fell 13%, 26%, and 6%, respectively. Throughout these challenging economic times, the bank remained highly profitable, and its dividend payout ratio never exceeded 42%.

However, RBC’s dividend was frozen during the financial crisis, so investors owning Canadian banks need to be prepared for potential dividend freezes in future downturns.

Also keep in mind that Canada’s extremely conservative regulators can change laws in ways that can negatively affect the bank’s profits. For example, they recently increased capital requirements by about 1% to accelerate the global banking regulations under Basel 3 that are designed to make global banks safer over time.

Higher capital requirements restrict the amount of leverage banks can use, thus lowering profitability. Should such regulations continue increasing, Royal Bank of Canada could struggle to hit its 16% return on equity target over the long term. However, RBC’s lean operations, impressive scale, and diversified mix of products and services likely position it better than almost all of its peers in such a scenario.

Finally, it should be noted that Canada has been in a large housing bubble, especially in certain key markets such as Toronto and Vancouver. Foreign investment dollars, such as from Chinese buyers, have inflated residential home prices to potentially concerning levels.

In response, Vancouver instituted a 1% asset tax on vacant properties last year. Along with stricter mortgage regulations, this has caused the housing market to cool, with home prices now drifting lower in some areas.

Some analysts are concerned that a U.S.-style housing crash might lead to large loan losses for Canadian banks, especially Royal Bank of Canada since 21% of its assets are in residential mortgages. For comparison, U.S. banks had about three times less exposure to mortgage loans when the housing bubble imploded and nearly destroyed the U.S. banking system.

However it should be noted that this risk is truly a worst-case scenario that is unlikely to ever occur. That’s because the U.S. housing crisis was largely a result of extremely speculative lending, in which even subprime borrowers with no assets, incomes, or jobs were given variable rate mortgages. These were later sold off to third parties, and leveraged credit products, such as credit default swaps and other derivatives, were built around them.

In contrast, Canadian mortgage lending is extremely conservative. For example, Royal Bank of Canada’s average mortgage FICO score is 786. To put that in context, the average U.S. FICO score is 700, and that’s a record high. In addition, the average down payment on the bank’s mortgages is close to 50%, and over 40% of its mortgages are insured. Finally, the Canadian government acts as a backstop for all mortgages under CAD 1 million.

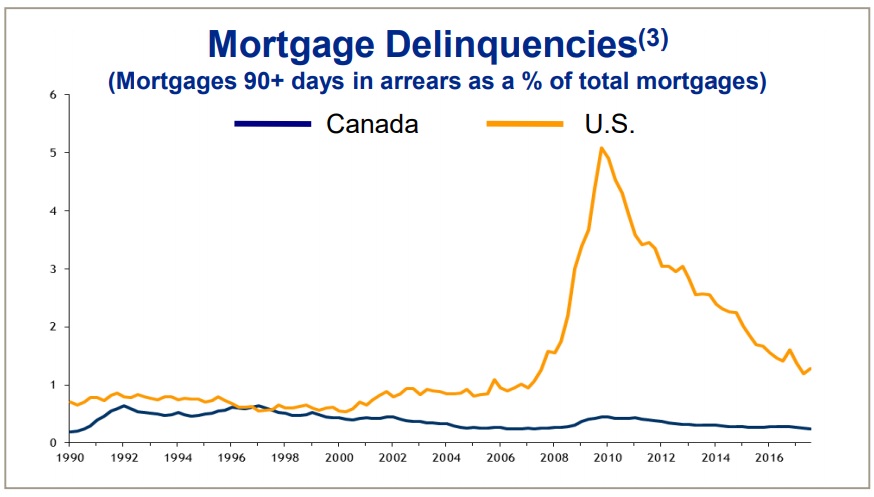

All these risk-mitigating factors make a U.S. housing crash highly unlikely. In fact, during the financial crisis Canadian mortgage delinquencies never rose above about 0.5%. Today, Royal Bank’s mortgage delinquencies are 0.19%, and its loan losses on mortgages are just 0.02%.

Simply put, recessions and stricter regulations are probably the biggest concerns investors should have when it comes to Canadian bank risk. However, these events are only likely to result in slowing or temporarily falling earnings growth rates. Barring a black swan type of scenario, Royal Bank of Canada is unlikely to actually lose money due to its very conservative banking practices.

Closing Thoughts on Royal Bank of Canada

U.S. banks violated the trust of their shareholders (and their customers) by taking extreme risks that nearly destroyed the global financial system a decade ago. And since banks are highly opaque and complex institutions, many investors prefer to avoid the sector entirely.

With that said, Canadian banking is a very different business that could appeal to even some conservative dividend investors. Strict regulatory oversight and an explicit oligopolistic mandate from the government have created enduring competitive advantages for Canada’s biggest banks.

As the largest player, Royal Bank of Canada enjoys a number of strengths including excellent economies of scale, a very conservative balance sheet, disciplined loan underwriting standards, strong market share positions, and numerous opportunities for long-term growth.

Royal Bank of Canada seems likely to be one of the most resilient banks during the next future economic downturn or crisis. Given the bank’s shareholder-friendly corporate culture, Royal Bank of Canada could be a dividend growth stock to consider for investors who are comfortable accepting some of the murkier risks inherent to the complex banking industry.

To learn more about RBC’s dividend safety and growth profile, please click here.

Leave A Comment