Founded in 1981, Roper Technologies (ROP) is a diversified industrial firm specializing in high-tech software and engineering solutions for the global healthcare, food, energy, water, education, construction, and legal industries.

The company operates in four segments:

- RF Technology (40% of revenue, 35% of operating profit): radio frequency identification or RIFD communication technology and subscription software solutions.

- Medical & Scientific Imaging (30% of revenue, 35% of operating profit): diagnostic and laboratory software solutions to help in 3D imagine, computer/robot assisted surgery, and advanced data driven diagnostics.

- Industrial Technology (18% of revenue, 19% of operating profit):produces primarily water meter and meter reading technology, fluid handling pumps, and materials analysis solutions

- Energy Systems & Controls (12% of revenue, 10% of operating profit): produces control systems, testing equipment, valves and sensors

While operating around the world, 80% of the company’s revenue is generated in the U.S. Roper’s customer base is highly diversified with no single client representing more than 10% of sales. Since its 1992 IPO, Roper has increased its dividend for 25 consecutive years, making it a dividend aristocrat.

Business Analysis

Industrial conglomerates are known for their sales, earnings, and cash flow volatility, since their business models are largely tied to the health of the U.S. and global economy.

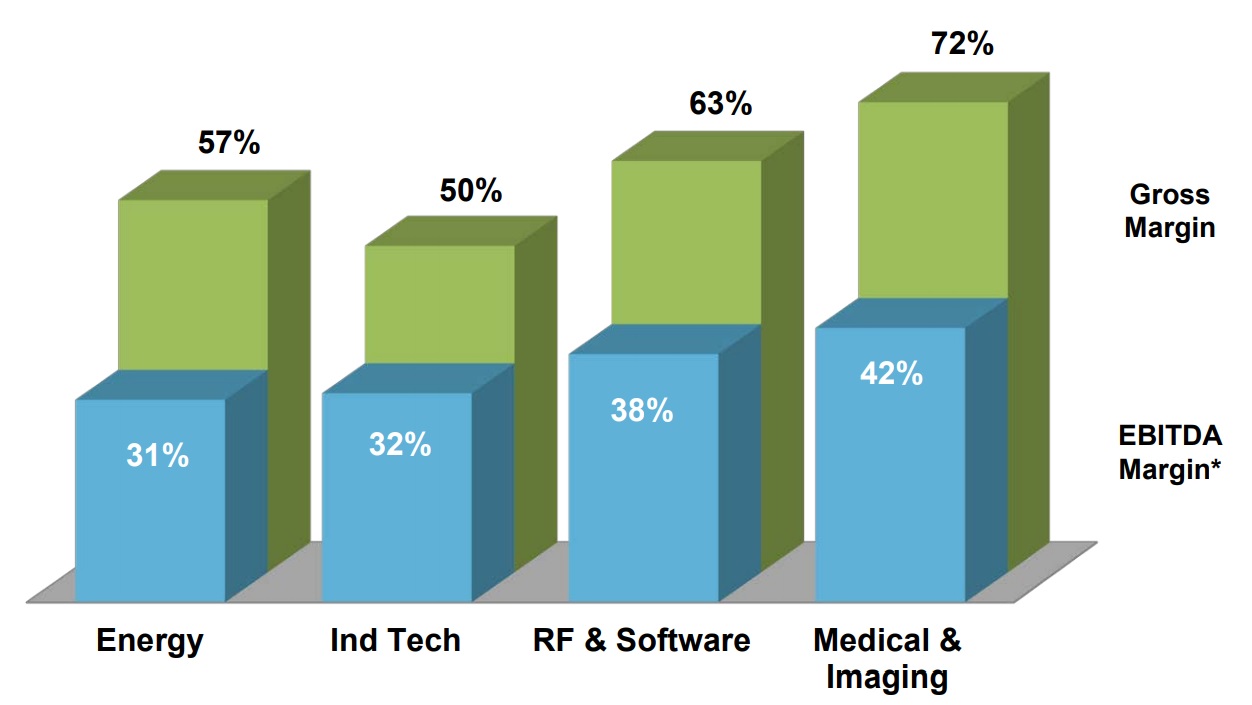

However, Roper Technologies has done a far better job than most of its larger peers at maintaining steady and fast growth in both its top and bottom lines. This is due to the company’s focus on very high-margin niches with large amounts of recurring revenue and strong customer retention rates. As you can see, each of Roper’s segments earns an EBITDA margin in excess of 30%.

In essence, Roper is less of a traditional industrial firm and more of a tech company with a capital light business model. In fact, about half of its sales are from recurring sources (consumables and subscription services). For comparison, most peers generate just 10% to 35% of their overall revenue from recurring sources. This creates extremely high margins and enhanced cash flow stability that most other industrial companies can only dream of.

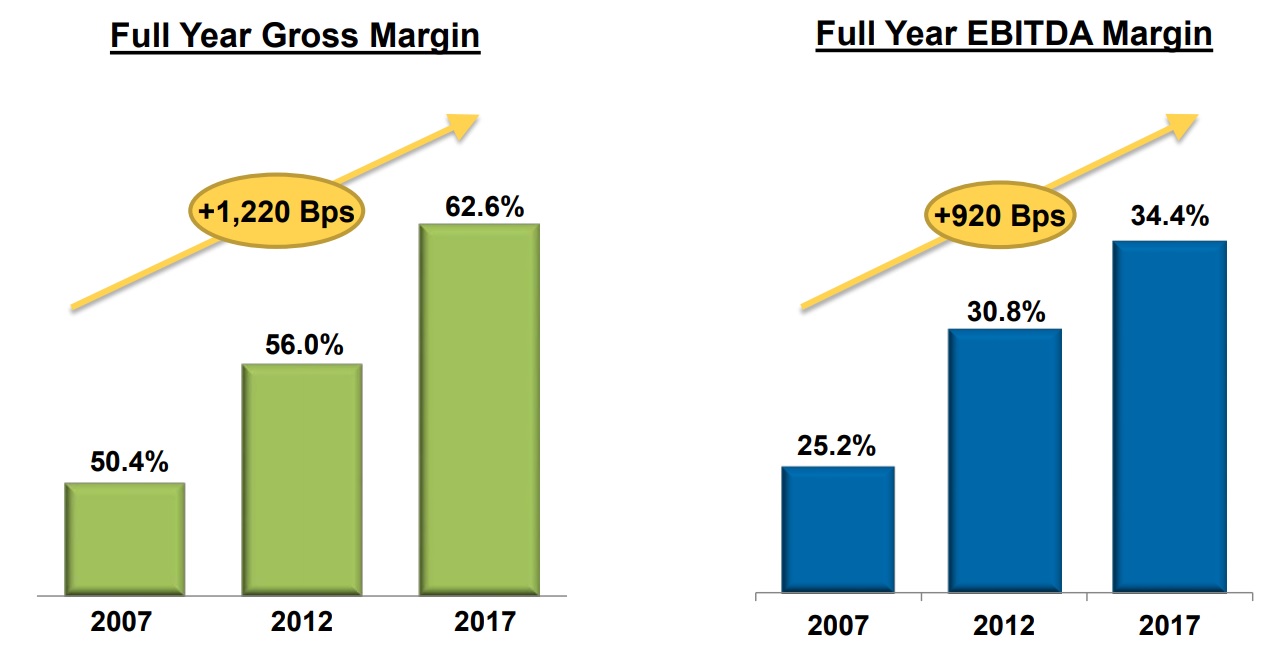

For example, in 2017 Roper spent just $53 million, or 1.2% of revenue, on maintaining or increasing its production capabilities. Rather, Roper focuses its investment efforts on R&D to keep its tech at the leading edge and thus maintain strong pricing power. In 2017, the company spent $281 million, or 6.1% of revenue, on R&D. Its total investment ratio (capex + R&D) was 7.2% of revenue compared to 9% to 12% which is common for most large industrial conglomerates.

This is why Roper is one of the most profitable industrial companies in America with truly impressive margins. The free cash flow (FCF) margin is one of the most important metrics for dividend investors because FCF is what’s left over after running the business and investing in future growth. It’s what funds dividends, buybacks, and pays off debt.

Roper’s FCF margin of approximately 25% is not only superior to most industrial firms (who typically have 10% to 15% FCF margins) but is actually higher than many tech companies such as Apple’s (22%). Roper’s FCF margin has averaged over 20% for the past decade, underscoring the efficiency of its high-margin, capital-light business model.

As you can see outlined below, Roper’s management seeks to invest in markets where the company can dominate thanks to the sophistication of its products and software. The company’s solutions tend to be entrenched in customers’ workflows and focus on mission-critical applications, creating high switching costs. When combined with their large base of recurring revenue, margins run high and generate a lot of free cash flow that management can reinvest in similar opportunities across a wide range of end markets.

To measure the firm’s performance, management uses its own proprietary metric called cash return on investment (net income + depreciation & amortization minus maintenance capital over gross investment), or CRI, which it believes is a better representation of Roper’s capital allocation strategy. That’s due to the very high tech nature of its business model, as well as the high rate of acquisitions that Roper has historically pursued.

In 2017, the company estimates its CRI was up 300% since 2003. Very few businesses in America have managed to achieve such significant and profitable growth, and shareholders have been rewarded with annual total returns more than doubling the S&P 500’s gains over this period.

The reason management is focused on CRI instead of the more standard return on invested capital (ROIC) metric is because companies that make lots of acquisitions can have artificially low returns on invested capital. It takes time for a new purchase to scale up and start contributing significantly to a company’s net earnings. And Roper is among the most acquisition-happy companies in its industry.

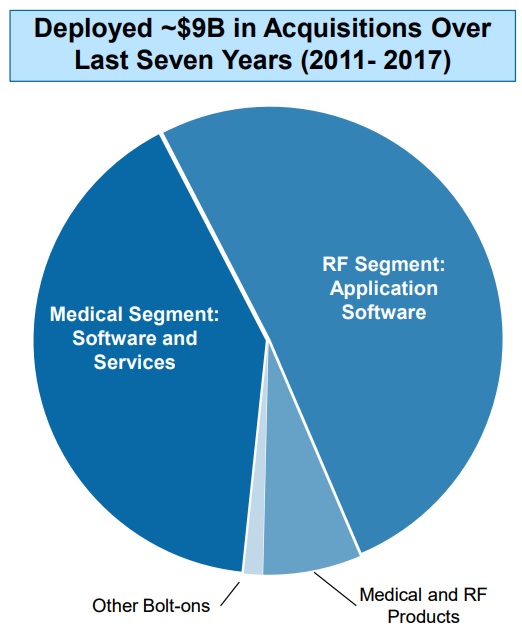

For example, between 2011 and 2017 Roper spent about $9 billion on acquisitions (25 purchases between 2013 and 2017), mostly focused on RF software and medical imaging software companies ($4 billion for 40 companies). These acquisitions have been increasingly focused on software companies with subscription-based business models that use three- to seven-year contracts and enjoy 97% to 98% customer retention rates. Between 2018 and 2021 the company expects to spend another $7 billion or so on further purchases.

That includes the recent $1.1 billion acquisition of PowerPlan, whose software platform integrates detailed financial and operational data to help enhance operational efficiency, minimize tax obligations, improve cash flow, and mitigate compliance risk for financial companies and asset managers. Basically, PowerPlan helps financial companies maximize profits while avoiding running afoul of complex government regulations. The company uses long-term subscriptions and has 98% retention rates. Roper expects PowerPlan to provide $150 million in revenue and $60 million in free cash flow over the next 12 months, representing 3% revenue growth and 6% FCF growth.

There are three key factors to Roper’s acquisition-driven growth strategy. First, the company’s management, led by CEO Brian Jellison (a 17-year veteran of the company with 37 years of industry experience), is highly disciplined in what companies it pursues.

For instance, Roper is careful to only buy companies whose products and services fit nicely with its increasingly software-as-a-service focused business model and whose sales can be quickly increased by plugging the new acquisition into its existing distribution network. In addition, the companies it buys need to have wide moats resulting in high profitability (50+% gross margins) and strong organic growth potential.

In addition, the companies Roper acquires usually have strong network effects and sticky ecosystems. For example, Roper sells RFID tags for toll roads and helps track shipments in the trucking industry. The high upfront cost of installing these systems, combined with its strong lead in proprietary software management systems to run these systems, means that customers are unlikely to switch to a rival supplier. Most of the companies Roper buys are the dominant player in their niches typically commanding 50% to 85% market share.

Roper has proven to be very good at acquiring companies with strong management teams who can operate autonomously (similar to the Berkshire Hathaway model) and can leverage the company’s existing and fast-growing asset base to achieve cost savings and boost margins over time. This explains the very high CRI and the company’s steadily rising and industry-leading margins.

The second factor key to Roper’s growth strategy is its strong balance sheet, which gives the company access to low-cost capital needed to fund its acquisitions. The company’s debt metrics are generally higher than the industry average, reflecting Roper’s extensive use of debt to acquire so many companies so quickly.

However, Roper still maintains a solid BBB+ credit rating from Standard & Poor’s thanks to its relatively stable and cash rich business model. As a result, the company’s average interest rate is just 3.9%, and Roper’s has over $2 billion of total liquidity it can use to pursue more acquisitions.

Unlike most dividend aristocrats, Roper also retains a very high amount of its free cash flow to further help its growth strategy. Most industrial companies distribute 40% to 60% of their free cash flow as dividends. Roper’s FCF payout ratio sits below 20%, meaning that it retains over 80 cents of every dollar of FCF it generates after paying dividends. The company can use this cash to reduce debt or fund more acquisitions.

To put it another way, despite growing its dividend very fast (13% annually over the past 20 years and 20% over the past five), Roper still retains the vast majority of its free cash flow to fund its ambitious growth efforts. As the company’s cash positions quickly piles up over time, Roper is able to borrow more aggressively at relatively low interest rates since the bond market knows the company can quickly pay its loans off.

Over the long term, analysts expect Roper to continue growing its revenue at about 8% per year (including 1-2% from acquisitions), which is in line with its historical norms. Thanks to the firm’s high and growing margins, that revenue growth is expected to translate into 12% to 13% EPS and FCF per share growth. Roper’s already high margins are expected to continue rising as more of its business comes from more profitable software subscriptions, which are expected to make up about 33% of its total sales in 2022 according to Morningstar.

And given the company’s extremely small payout ratio, Roper will likely deliver low to mid-double-digit annual dividend growth over the long term. That makes Roper one of the fastest growing dividend aristocrats in America and potentially an appealing long-term income growth investment.

Key Risks

There are three key risks to be aware of with Roper. First, while the firm generates about 80% of revenue in the U.S., it still has significant currency exposure. For example, in recent years currency fluctuations have resulted in 200 to 300 basis point swings in reported sales and cash flow growth rates based on whether or not the U.S. dollar was rising or falling against local currencies in which Roper operates overseas.

When the dollar rises in value against other currencies, Roper’s prices are higher to its overseas customers (potentially slowing sales growth), and also sales and profits are worth less in U.S. dollars. However, this risk is unlikely to affect Roper’s long-term earnings power.

A more significant medium-term risk is that while 50% of Roper’s sales are from recurring products and services, the other half remains cyclical and tied to the health of certain key industries, especially in its older (and more capital intensive) energy and industrial technologies segments. As the company’s software-as-a-service, RFID, and medical imaging businesses grow over time, Roper’s revenue and cash flow volatility should be reduced. However, for at least the next few years, Roper’s growth rates will remain tied to the broader U.S. and global economies.

Roper’s biggest potential risk is due to its acquisition-focused growth strategy. Buying up other companies creates execution risk on several fronts. First, Roper is focused increasingly on high-tech software companies. While these firms often come with high-margin and FCF rich subscription business models, they can also be rather expensive (especially in today’s world of low interest rates and high asset prices).

As a result, Roper is at risk of overpaying for current but especially future acquisitions. For instance, in December 2016 Roper paid $2.8 billion for software company Deltek. That represented a hefty forward price-to-sales ratio of 5.2 and a price-to-cash flow ratio of about 14.

The recent PowerPlan purchase was for 7.3 and 18.3 times forward sales and cash flow, respectively, indicating that Roper is finding it has to pay ever richer multiples to keep buying the kind of companies it wants. This creates more pressure on the company to make sure the new management teams are able to operate in Roper’s decentralized style and achieve their cost cutting and growth targets. Otherwise, Roper’s high-priced deals might take many years to pay off assuming they do at all.

Closing Thoughts on Roper Technologies

As far as industrial dividend aristocrats go, Roper Technologies is one of the most impressive. Not only has management proven to be highly adept at growing the company at a breakneck pace through well-executed acquisitions, but the firm has consistently been able to generate some of the industry’s highest margins.

In addition, most of Roper’s subsidiaries enjoy entrenched market positions and generate superb free cash flow given their focus on capital light software and recurring revenue. And thanks to the fast growth rates and fragmented nature of the industries in which it operates, Roper’s growth runway is likely to remain long and strong for the foreseeable future.

While Roper’s paltry dividend yield may rule the stock out for many income-focused portfolios, the company appears to be one of the most attractive industrial businesses for long-term dividend growth investors to consider.

To learn more about Roper’s dividend safety and growth profile, please click here.

Leave A Comment