Founded in 1966 in London (with roots going back to 1859), Pentair (PNR) is one of the world’s leading liquid pump, valve, and control system manufacturers with operations in over 30 countries. On May 1, 2018, the company completed the spin-off of its electrical business from its water business (which made up 57% of sales in 2017).

The new electric-focused company is called nVent (NVT), while Pentair continues trading as a pure play water and fluid products company. The firm builds filters, pumps, valves, controllers, and actuators for moving, purifying, controlling, and storing water and other fluids for commercial, industrial and residential purposes.

Pentair sells its products to agriculture, food service, and food & beverage industries, as well as various industrial clients and residential users (such as homeowners with pools).

In 2018, Pentair expects to generate $3 billion in revenue split between residential (60% of sales), industrial/infrastructure (20%), and commercial (20%) customers. Overall, about 75% of sales are to water, food, and energy end users, and approximately 70% of revenue is from consumable and recurring aftermarket sources (maintenance contracts).

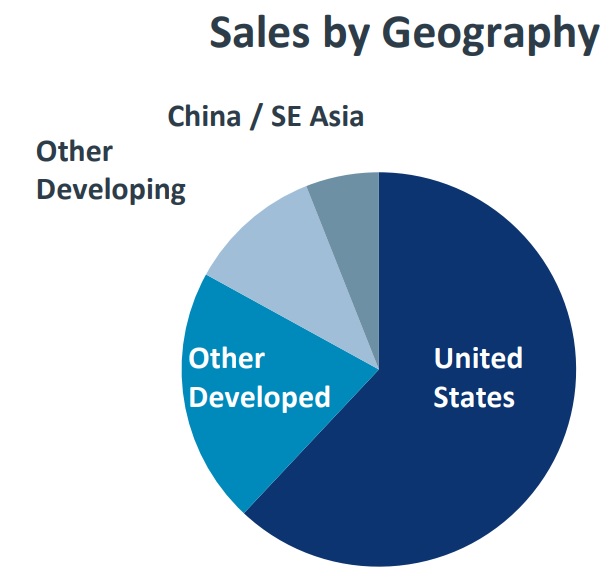

About 80% of the company’s sales come from developed markets, with roughly 60% originating in the U.S. Emerging markets, including China and Southeast Asia (including India), represent the company’s largest growth markets.

Note that due to the nVent spin-off, which significantly lowered the firm’s ongoing cash flow generation, Pentair reduced its dividend by 50% in the second quarter of 2018. However, adjusted for the spun off shares (which also pay a dividend), Pentair retains its dividend aristocrat status thanks to 42 straight years of annual payout increases.

Business Analysis

In order for any company to be able to consistently grow its dividend for decades, it must have several factors working to its advantage.

Pentair’s advantages primarily come from its long-standing customer relationships (Pentair has over 50 years of operating history), focus on profitable niches, reputation for quality, wide assortment of products, technical know-how, and sizable distribution network.

Pentair also has a large global installed base, which provides meaningful aftermarket revenue. Following the spin-off of its electric business, which had volatile sales and earnings, about 70% of Pentair’s revenue now comes from recurring sources (fast consumables and aftermarket).

In other words, the company’s future revenue, earnings, and free cash flow should be far more stable over time, supporting Pentair’s growth plans which include bolt-on acquisitions. The company’s markets are highly fragmented, so it has plenty of opportunity to continue consolidating the industry.

One reason why well-run industrial companies often make good dividend growth stocks is because their management teams are skilled at using the industry’s cyclical downturns to restructure and improve their business models.

Post spin-off, Pentrair’s CEO Randall Hoggan (who was CEO for 17 years) retired and was replaced with John Stauch. Stauch served as CFO for the past decade and worked closely with Hoggan on navigating the company throughout various dips in industrial demand.

He’s considered an expert on industrial turnarounds and especially well-versed at optimizing supply chains and improving operating results for smaller bolt-on acquisitions. In fact, Stauch was a big driver of the company’s substantial improvements in profitability over the past few years (operating margin doubled from 8% in 2012 to 16% in 2017).

A key to that turnaround was the company’s Pentair Integrated Management System (PIMS), which is grounded in lean methodologies. Pentair began its initial lean deployments in 2005 and believes lean operations are now part of its DNA, driving productivity throughout the enterprise.

PIMS led Pentair to refocus its efforts on higher margin and faster growing product lines. In other words, the company began more intentionally pursuing higher-quality and more profitable growth rather than growth for its own sake.

The goal of PIMS is to continually optimize the company’s two main competitive advantages. The first is economies of scale, including increasing efficiency in production, and sourcing of inputs from all over the globe. This scale comes from Pentair’s strong market share in its various water businesses (5% to 20% depending on product). That might not sound like much, but the industrial industry is very fragmented, so even the biggest players usually only command 10% to 20% market share in any given product line.

The firm’s second competitive advantage is its strong customer relationships that help create pricing power. That’s partially due to Pentair’s skilled sales force which maintains very long relationships with industrial and commercial clients, as well as distributors of residential water products.

Pricing power is also created due to the fact that Pentair’s water control systems serve as mission-critical inputs for most of its end users. For example, the company builds offset valves for handling toxic waste, as well as components that go into blowout preventers for the energy industry.

Given the serious nature of these use cases (and potentially enormous legal liabilities that result from failure), customers are often more concerned with reliability and durability than price. The ultimate cost of each component is also a relatively small part of the overall price of a customer’s fluid management system, lowering the incentive for customers to pressure Pentair on the prices it charges.

Pentair has spent many years focused on higher margin and more specialized components, including customer-specific filters and flow system components. This helps create higher switching costs as well because finding a new supplier who can tailor-make new systems is both expensive and time consuming. Meanwhile, the company’s consumables (mostly filters) are also specialized and enjoy above-average margins.

To help prevent other companies from stealing market share, Pentair spends about 4% of its revenue on R&D each year to continue innovating and offering superior products. For context, the typical industrial company invests 2% to 3% of sales into R&D each year. This spending is what allowed Pentair to invent the triple inverted valve (zero leakage), as well as the IntellFflo energy efficient variable speed pumps which now dominate the residential pool market.

Specialized products, strong customer relationships, and ongoing commitment to R&D are the main reasons why Pentair is able to retain such a loyal, large, and growing customer base. All while enjoying a 19% operating margin in 2017 (on the water business) compared to the industry average below 10%.

Going forward, the company is focused on two key growth strategies. First, Pentair wants to increase the stability of its cash flow even further by offering more integrated systems. This would make Pentair a one-stop shop that offers more value compared to being just a specialized component supplier.

This strategy also fits into the company’s growing aftermarket maintenance business, which represented about 30% of the Pentair’s sales in the past year. Pentair’s long operating history means it has an enormous installed base of fluid control infrastructure in place. This creates the opportunity for increased sales of maintenance and service contracts that represent stable and recurring revenue.

Finally, Pentair is focused on winning new business thanks to the huge need for new global water infrastructure today and in the future. For example, Pentair estimates that its current addressable market for existing water and fluid products and services is about $40 billion.

However, according to the World Bank, between 2016 and 2040 the world’s population is expected to increase 25%, or by 2 billion people. As a result, the world will need $94 trillion in new infrastructure ($97 trillion to meet the UN’s sustainability goals), including $51 trillion in Asia. China ($28 trillion), India, and Japan will have the largest needs, which is why Pentair’s management has specifically outlined Asia as its key growth priority in the coming years.

Water infrastructure, needed for the growing population of people living in urban areas, is going to be a major component of that spending. According to the American Society of Civil Engineers, in the U.S. alone annual spending on water infrastructure, to both expand and replace aging systems, will rise to $153 billion per year by 2040.

And according to the OECD, by 2040 the world will need to spend an additional $6.7 trillion (on top of what’s already planned) to expand and improve the world’s access to clean water. In other words, Pentair’s future growth runway is both large and long.

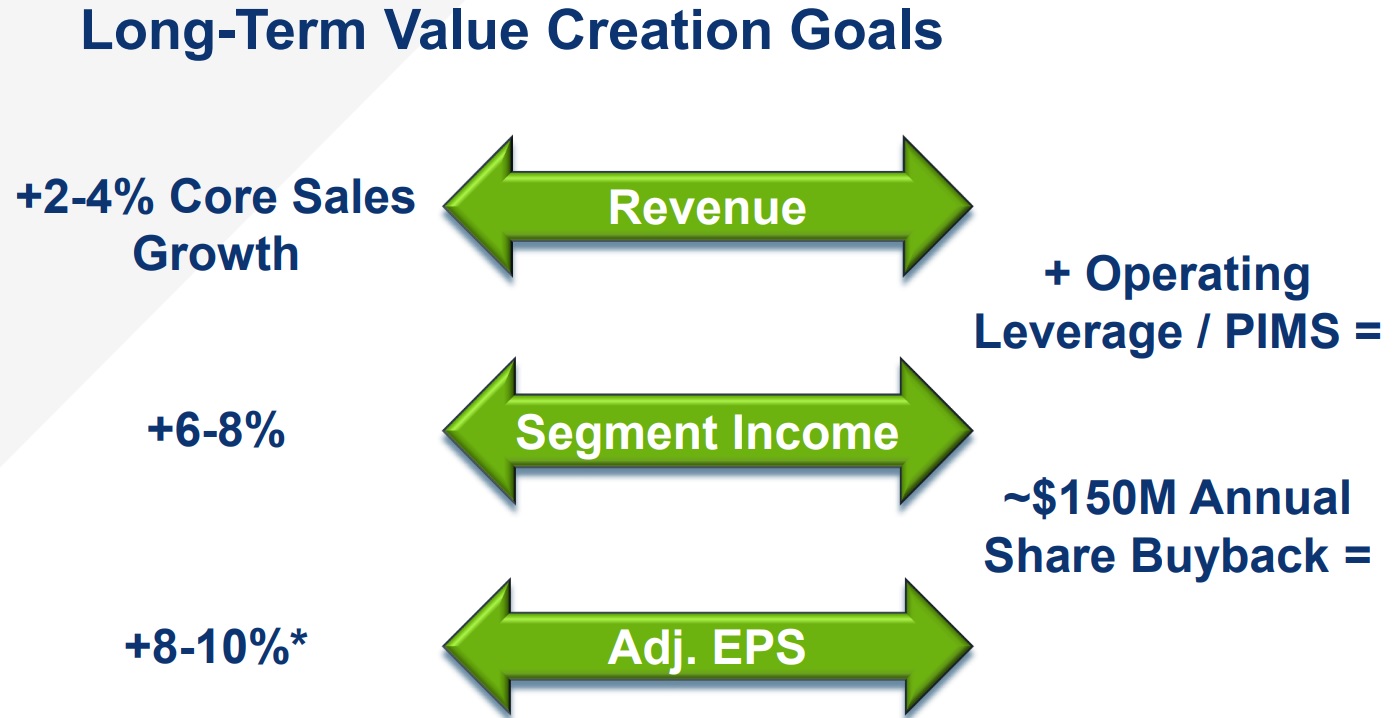

Thanks to these drivers, the company believes it can achieve organic sales growth of 2% to 4% per year, which seems reasonable. Organic growth will be augmented with small to medium-sized acquisitions that fit well into Pentair’s existing and planned product lines.

Management believes that when combined with rising profitability from a greater focus on high-margin products and maintenance contracts, this should allow Pentair to generate about 8% to 10% long-term earnings growth.

Pentair’s dividend will likely grow at a similar high single-digit pace over the coming years. However, there are several challenges that could get in the way of management’s long-term goals.

Key Risks

There are several risks Pentair will need to deal with in the future.

First, as the business focuses more on growing its sales in emerging markets, Pentair will have higher exposure to fluctuating currency exchange rates which can impact its reported sales and earnings growth. Currency fluctuations tend to balance out over time, but they can create short to medium-term headwinds.

The second risk is that while the new and more focused Pentair should enjoy less volatile sales and earnings, it will still have some exposure to cyclical industries such as oil & gas (10% of sales in 2017). That might not sound like much, but keep in mind that during an oil crash sales to these customers can potentially fall by as much as 25% to 50%.

Thus, having just 10% of sales dependent on the energy industry could still result in a 2.5% to 5% decline in overall revenue. For a company whose long-term organic revenue growth target is 2% to 4%, that represents a potentially significant short-term risk. Fortunately, Pentair’s 42-year dividend growth record indicates that even under such challenging conditions the payout would likely remain safe, though growth might slow to a trickle until its customers recover.

Finally, be aware that while Pentair isn’t known for flashy acquisitions (which often don’t work out), it has periodically made big strategic moves such as its $4.9 billion merger of Tyco International’s flow control division in 2012. The risks with any big purchase are that management can overpay and expected cost synergies might not appear, destroying shareholder value. The stakes are arguably higher today since Pentair is a smaller standalone business following its spin-off of nVent.

Closing Thoughts on Pentair

Pentair has spent over half a decade building up a trusted global brand for mission-critical water infrastructure, filtration products, and fluid management systems. The company’s long relationships with customers, strong history of R&D-driven innovation, and increasing mix of high-margin recurring revenue should help drive strong earnings and free cash flow growth in the coming years.

And with the world’s water infrastructure needs expected to boom in the decades ahead, Pentair’s impressive dividend growth streak is likely to continue for the foreseeable future.

To learn more about Pentair’s dividend safety and growth profile, please click here.

Leave A Comment