Founded in 1922, Raytheon (RTN) is a defense contractor and technology leader specializing in defense, civil government, and cybersecurity solutions. The company operates through five segments:

- Missile Systems (29% of sales, 31% of income): develops and supports a range of weapon systems, including missiles, smart munitions, close-in weapon systems, projectiles, kinetic kill vehicles, directed energy effectors, and combat sensor solutions.

- Integrated Defense Systems (22% of sales, 28% of income): specializes in air and missile defense, large land- and sea-based radars, and systems for managing command, control, communications, computers, cyber and intelligence. It also produces sonars, torpedoes, and electronic systems for ships.

- Space and Airborne Systems (24% of sales, 26% of income): is a leading provider of radar and sensor systems on airborne and space-based platforms. The business also provides communications, electronic warfare, high-energy laser solutions and special mission aircraft for the network-centric battlefield. Also provides Research advancements range from linguistics to quantum computing.

- Intelligence, Information, and Services (23% of sales, 14% of income): designs and delivers solutions and services that leverage its deep expertise in cyber, analytics and automation. Software, systems integration, and the support and sustainment of Raytheon and other companies’ systems for intelligence, military and civil applications are delivered across four domains: space, cyber, mission readiness, and multidomain battlespace management command and control.

- Forcepoint (2% of sales, 1% of income): this cybersecurity business focuses on understanding people’s intent as they interact with critical data and intellectual property wherever it resides. Forcepoint’s Human Point System enables customers to understand the normal rhythm of user behavior and the flow of data throughout an organization to rapidly identify and eliminate risk for thousands of enterprise and government customers.

Raytheon serves the U.S. Department of Defense (DoD), the U.S. Intelligence Community, the U.S. Armed Forces, the Federal Aviation Administration, the National Oceanic and Atmospheric Administration, Department of Homeland Security, NASA, and other international customers.

While Raytheon sells all over the world, in 2017 68% of its revenue came from the U.S. In total, 67% of sales were to the U.S. DoD and 13% to foreign militaries.

Business Analysis

Large defense contractors often enjoy a wide economic moat around their businesses. However, their sales and earnings can be cyclical due to swings in annual defense spending resulting from budgetary negotiations. This is why the industry has periodically experienced waves of bankruptcies including in the 1960’s and the early 1980’s.

After the collapse of the Soviet Union, the DoD drastically reduced spending, resulting a wave of industry consolidation that the Pentagon believed was crucial to creating a few large but financially sound contractors. As a result, Raytheon has just four major U.S. rivals: Lockheed Martin (LMT), General Dynamics (GD), Northrop Grumman (NOC), and Boeing (BA).

Besides a limited amount of competition, Raytheon enjoys four other major competitive advantages.

First is the highly complex and mission-critical nature of Raytheon’s defense systems, which are proven technology that it can sell not just to the DoD, but also to U.S. allies such as Saudi Arabia and Japan. In addition, Raytheon has been winning contract awards for its Patriot missile systems from numerous European countries including Sweden and Romania.

The specialized nature of these defense systems creates high switching costs since Raytheon isn’t just selling individual weapons to its clients but entirely integrated systems. For example, the Patriot Missile Defense System (the world’s most popular missile defense system) includes interceptor missiles, radar detection hardware, and software to integrate complex systems together. Once a customer chooses Raytheon, it’s unlikely to go through the hassle of switching to a rival system.

Raytheon’s second major competitive advantage is that the company has experience navigating the complex and byzantine labyrinth of U.S. government procurement contracts, which raise the industry’s barriers to entry. The Federal Acquisition Regulation (FAR), for example, sets forth policies, procedures, and requirements for the acquisition of goods and services by the U.S. government.

Raytheon is also well versed in the DoD’s Defense Federal Acquisition Regulation Supplement (DFARS). These regulations impose a broad range of requirements, many of which are unique to government contracting, including various procurement, import and export, security, contract pricing and cost, contract termination and adjustment, audit, and product integrity requirements.

Foreign sales to allies are also strictly regulated with many deals being brokered by the DoD itself via the U.S. Defense Security Cooperation Agency (DSCA), which is run by the Pentagon. That’s especially true when it comes to classified products that have their own unique regulations for design and sale. In 2017, approximately 17% of Raytheon’s sales were classified weapons systems.

All told, this maze of government regulations means that the defense contractor industry enjoys relatively little major competition with just a few key players dominating each specific niche. For instance, Raytheon’s Patriot Missile Defense system only competes with Lockheed Martin’s offering. And in ship defense systems, Raytheon only competes with General Dynamics and Lockheed.

The company’s third competitive advantage is economies of scale, specifically in the missile systems that Raytheon is known for. For example, the company is able to spend a substantial amount on R&D ($734 million in 2017, or about 3% of sales), focusing activities in emerging areas such as data analytics, hypersonics, machine learning, nanotechnology, quantum mechanics, and sensor systems. Simply put, Raytheon is as at the cutting edge of missile technology.

Raytheon also has very large and advanced manufacturing capabilities that few rivals can match which. This helps the company deliver its defense systems at a competitive cost while also bolstering its profit margins. Thanks to its scale, trusted reputation, and engrained position with U.S. and foreign governments, Raytheon’s backlog exceeded $38 billion at the end of 2017, providing the firm with plenty of growth opportunities to execute on over the coming years.

Finally, Raytheon derives a competitive advantage from its strong balance sheet. The company’s conservative leverage earns it an A credit rating that helps it borrow at a relatively low interest rate. As a result, Raytheon has more flexibility to invest in R&D, make acquisitions, and of course return more of its growing cash flow to shareholders via share repurchases and dividends. In fact, the business has increased its dividend for 14 consecutive years.

Key Risks

While Raytheon enjoys a number of advantages in its key businesses, there are nonetheless several risks to keep in mind.

First and foremost is the company’s very high dependence on U.S. defense spending, which accounted for 67% of sales in 2017. Due to the large national budget deficit, Congress is frequently changing budgetary appropriations including on defense spending.

For example, in 2011 Congress enacted the Budget Control Act of 2011 (BCA), which established specific limits on annual appropriations for fiscal years (FY) 2012–2021. The BCA has been amended a number of times leading to fluctuations and unpredictability in annual DoD funding levels. That includes a 7% decline in 2013 and no growth in 2014 and 2015 before rising 5% and 3% in 2016 and 2017, respectively.

In February 2018, Congress struck a two-year budget deal that boosted U.S. DoD spending by 15% for 2018 and 2% more in 2019, representing a total increase of about $75 billion.

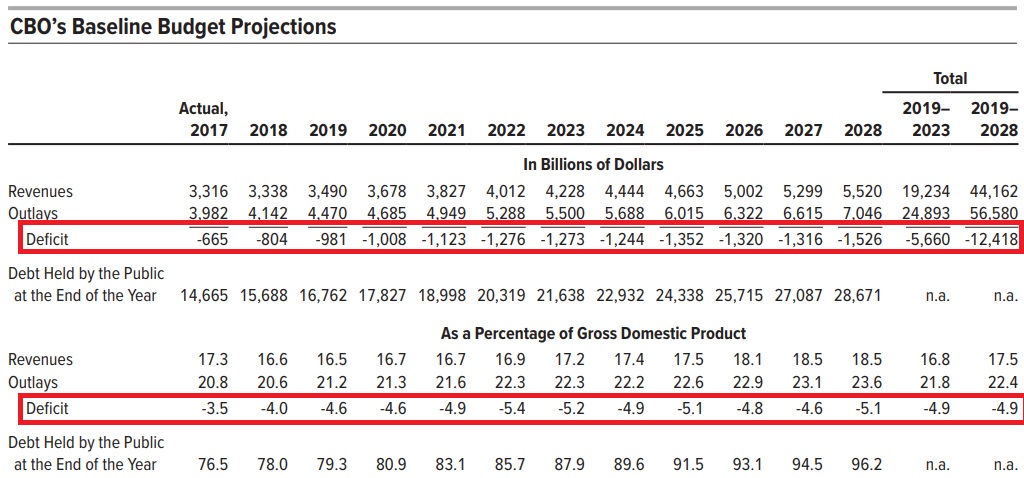

However, given major concerns about annual deficits (the Congressional Budget Office projects to the deficit to run over $1 trillion per year by 2020), there is always a risk that future deep cuts in defense spending could hit Raytheon hard and make growth expectations miss their marks.

And even assuming that U.S. defense spending doesn’t get significantly reduced, the complex nature of the firm’s government contracts (Raytheon has several thousand) that have their own risks. That’s because U.S. government contracts generally permit the government to terminate the contract, in whole or in part, without prior notice, at the U.S. government’s convenience or for default based on performance.

A convenience cancellation (say due to budget cuts) will provide Raytheon with some compensation. But if it defaults on the performance terms of a contract, then the company can owe the government money and increase its risk of failing to win future contract awards.

It’s also worth mentioning that 63% of Raytheon’s contracts are fixed price in nature, meaning that the company is given a set amount of compensation for its products and services, regardless of its ultimate costs. Any cost overruns (which occur frequently in this industry) are born by Raytheon in the form of lower profits and margins. In 2007, Congress made fixed-price contracts the standard unless the DoD could prove that a no-bid, cost-plus contract was necessary for national security.

Finally, while Raytheon is a leader in its industry, the company faces competition from several major rivals, including overseas companies that have close ties with their governments. Raytheon may fail to win future contracts with key U.S. allies if those governments decide to take a protectionist stance and award the contract to domestic or other allied national firms. Or to put it another way, Raytheon, like many U.S. defense contracts, is exposed to geopolitical and foreign political risk.

Overall, Raytheon seems very likely to continue playing a major role in defense systems in the U.S. and abroad. The company’s results are certainly sensitive to trends in defense spending, especially in America. However, Raytheon’s relatively high mix of international revenue (32% of sales) and lack of dependence on any single defense program help insulate it from any major disruption in the future.

Furthermore, very few companies are qualified to navigate the minefield of government regulations and relationships needed to compete in this space. When combined with Raytheon’s cost-effective scale, massive backlog, and reputation for reliability with its mission-critical defense systems, the business should remain a force for many years to come.

Closing Thoughts on Raytheon

The world of defense contractors is complex, with major industrial conglomerates that enjoy dominant market positions but also face multiyear cycles of volatile sales and margins as defense budgets oscillate. Raytheon, as one of America’s big five contractors, has proven itself well-suited to navigating the challenging nature of this industry.

While all defense contractors face challenges in a world where U.S. budget deficits might crimp DoD spending over the next decade, the budget deal reached in early 2018 will boost spending over the next couple of years. Not surprisingly, Raytheon’s short-term outlook is quite positive, and the firm’s dividend looks very safe with above-average growth potential.

Raytheon appears to be a solid company to consider for a long-term dividend growth portfolio. However, investors must remember the spending cycles the industry tends to experience over time. The best opportunity to buy a business like this is likely when the market is growing pessimistic about short-term defense budgets.

To learn more about Raytheon’s dividend safety and growth profile, please click here.

Leave A Comment