Public Storage (PSA) was founded in 1972 and is America’s largest self-storage REIT, owning over 2,500 storage rental properties in 38 states and seven European countries. The company also owns a 42% stake in PS Business Parks (PSB), which leases out commercial space to small and mid-size businesses.

U.S. self-storage operations account for approximately 86% of company-wide net operating income, followed by commercial properties (6%), ancillary businesses (6% – reinsurance policies, locks and cardboard boxes), and European self-storage (3%).

In total, Public Storage serves over one million customers. The company’s business model provides great short-term visibility because customers typically sign month-to-month leases. This gives the REIT some protection against inflation because it can continually adjust rents to account for higher costs.

Business Analysis

Since inception in the early 1970’s, the storage industry has been the fastest-growing segment of the commercial real estate industry, according to the Self-Storage Association.

According to the Self-Storage Almanac, there were only 31,947 self-storage properties in the U.S. in 2000. Today, there are more than 50,000 properties.Increased population density and an aging population have helped drive the surge in storage properties, providing a nice tailwind for Public Storage. However, there’s much more to the company’s story.

Public Storage looks like a great business for several reasons, starting with its sheer size. The company is larger than its top three competitors combined and locates many of its facilities in close proximity to each other, which allows it to leverage its costs (property management, maintenance, and advertising) across the company to achieve better profitability.

Public Storage also focuses on major metropolitan areas with favorable demographics. Over 70% of the company’s same-store revenues are generated in the 20 metropolitan areas with the highest population levels. These areas are characterized by better incomes, greater popular density, and faster growth rates. They also provide consumers with easier access to storage since they are conveniently located (customers store their goods within a five mile radius of their home or business, according to the company).

Public Storage has built up 20%+ market share in many of these cities and benefits from the high visibility its locations receive, further building up the company’s brand value and recognition. Thanks to its major-market concentration and size, Public Storage can also afford to use television advertising to reach new customers, which none of its smaller competitors can pay up for because they lack scale in these markets.

The company’s well-recognized brand and market concentration, combined with the highly fragmented nature of the industry, mean that Public Storage is more likely to appear in unpaid search results for self-storage as well, lowering its cost to acquire new customers. That’s an increasingly important advantage as online marketing channels now drive more than 65% of move-ins for the company.

With that said, barriers to entry are still relatively low in the self-storage industry. However, it is harder for new rivals to enter major metropolitan areas because of their higher property costs and increased zoning restrictions.

Self-storage warehouses are also attractive because they require very little costs to operate. Unlike most other types of buildings (e.g. offices and apartments), these facilities do not need carpet or furniture or much equipment that needs to be maintained.

They also require few employees to run them because they are largely self-serve, and much of the work needed can be automated (e.g. security cameras instead of security guards; online reservations). In fact, Public Storage has just 5,500 employees compared to its 2,500+ property locations.

As a result, once a storage facility reaches a high enough occupancy level, they generate excellent profit margins, have risk spread across a large tenant base, and require little maintenance capital expenditures to maintain their appearance.

Unlike most REITs (and many other types of businesses, for that matter), the company’s unique qualities have made it a free cash flow machine over the years. Public Storage’s warehouses pay for themselves and the land owned underneath them, which is quite valuable considering the company’s focus on major metropolitan areas.

As long as people continue experiencing major life events such as an unexpected move or divorce, there will be demand for self-storage warehouses. In fact, the self-storage industry’s free cash flow per share fell by less than 5% during the financial crisis, according to a 2013 report by Bank of America Merrill Lynch.

While consumers spend less during recessions, they still need a place to store their stuff. Simply put, the industry is very stable and predictable with a slow pace of change – all good things for long-term dividend growth investors.

In addition to the company’s impressive profitability and cash flow generation, its management team, led by CEO Ronald Havner (who’s been in the top spot since the turn of the century), has remained disciplined in the company’s expansion.

That means avoiding reaching for growth by overpaying for new facilities and maintaining the most conservative approach to debt of any REIT. And despite its large size, Public Storage has just 6% market share in U.S. self-storage facilities, which number over 50,000.

The self-storage market is vast in size but also incredibly fragmented. In fact, the top five operators have less than 15% of all facilities, with the remainder owned by numerous regional and local operators. In other words, there remains a very long growth runway for Public Storage to continue expanding and consolidating the market.

Public Storage has uniquely positioned itself to take advantage of this opportunity with the way it has managed its capital structure. Specifically, management has historically raised most of the company’s growth capital not from debt or common equity, but through issuing preferred shares.

There are two benefits of funding growth this way. First, preferred stock isn’t debt, meaning that by relying on preferred shares the company keeps its balance sheet squeaky clean and thus maximizes its financial flexibility in the future.

For example, if Public Storage wants to make a major acquisition, such as acquiring one of its larger rivals, its strong credit rating (A from S&P) would allow it to take on a lot of very cheap debt.

This would allow the company to grow without diluting existing common shareholders and would send its adjusted funds from operations (AFFO) per share soaring, allowing for an even safer and likely faster-growing dividend.

The second benefit of preferred shares is that, unlike bonds, which eventually mature and need to either be repaid or refinanced (exposing the REIT to interest rate risk), preferred shares, especially those sold recently at low yields, are potentially perpetual. In other words, management has the ability to one day buy them back (i.e. pay them off) or not, depending on what interest rates are doing at the time.

Put another way, Public Storage’s management has taken an ultra-conservative approach to debt that helps to maximize the company’s long-term growth, results in a very safe dividend, and will likely protect it should the corporate credit market ever freeze up, as it did during the great financial crisis of 2008-2009.

For all of these reasons, Public Storage has been able to pay uninterrupted quarterly dividends since 1981 while increasing its payout each year since 2010.

Key Risks

While there are plenty of things about Public Storage for dividend investors to like, nonetheless there are two main risks to consider.

Most notably, the self-storage market still goes through ups and downs just like any other market. For example, read this excerpt from a 1990 article in The Los Angeles Times:

“Public Storage has struggled to attract investors to recent projects, owing to the sagging real estate investment market, lower yields on Public Storage’s deals and investor nervousness about Public Storage’s issuance three years ago of $135 million of junk bonds. The surge in competition has also made it harder for Public Storage to find new sites and to raise rental prices.”

The last few years have been somewhat of a golden age for storage REITs, thanks to new supply of storage facilities growing much slower than demand following the financial crisis. This has allowed very strong rental increases that still allowed occupancy rates to hit record highs.

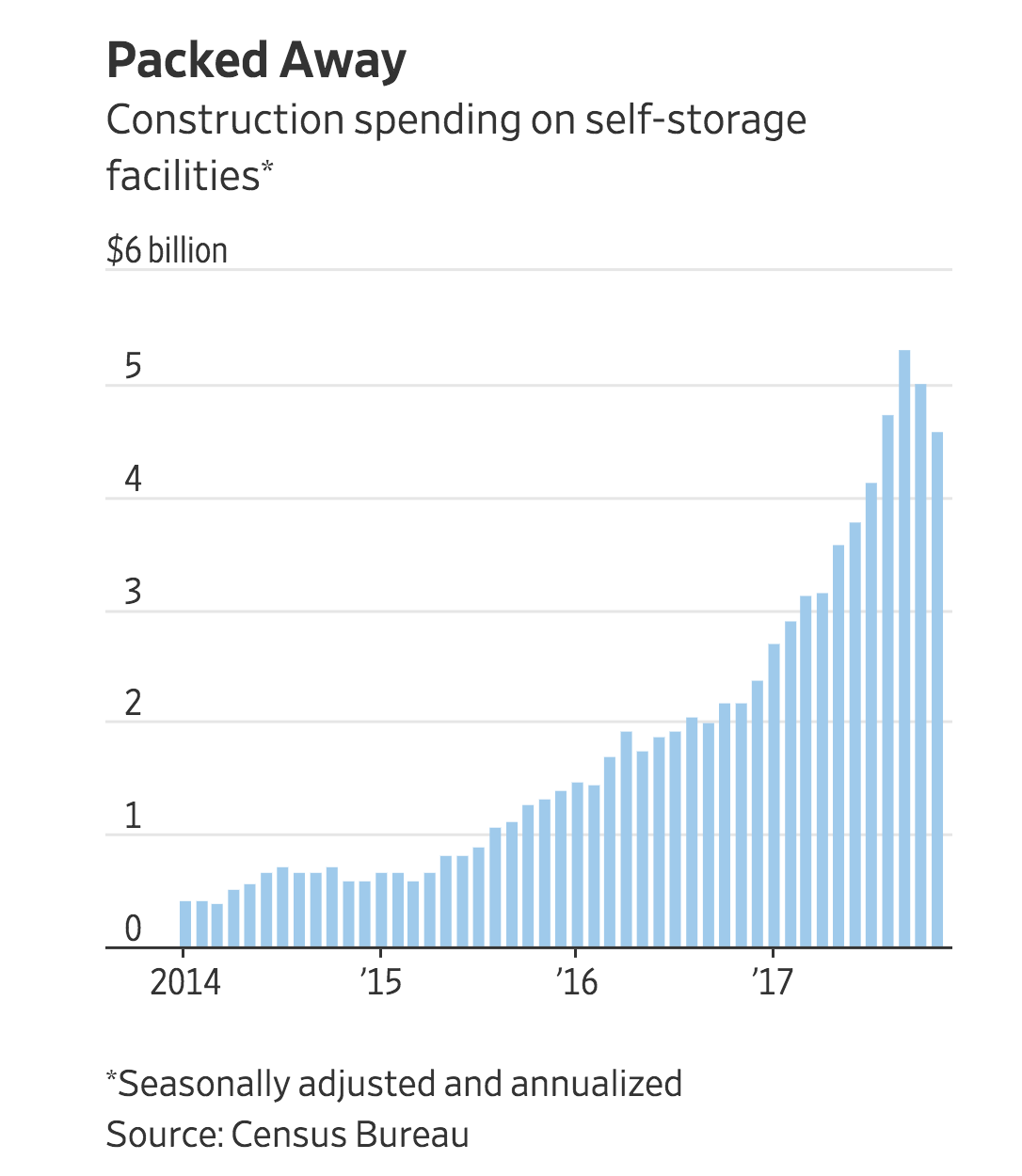

According to the Self-Storage Almanac, the industry’s occupancy rate has improved from about 80% in 2008 to more than 90% today, for example. However, the strong economics of this business are attracting new supply.

As you can see below, courtesy of The Wall Street Journal, construction spending on self-storage facilities has surged over the last few years. In fact, spending is at unprecedented levels that far exceed even the pre-financial crisis period, which never saw annual spending exceed $1.5 billion.

While supply pressures mount, the outlook for self-storage demand is also becoming murkier. Specifically, millennials are waiting longer to get married and buy homes, causing overall U.S. household formation to slow, and millennials also tend to own fewer material things than baby boomers, opting to spend on experiences and travel instead.

But the public storage industry is still expected to continue growing over the long term, thanks to America’s aging demographics. Between 2012 and 2060, America’s population of those over age 65 is expected to grow by nearly 50 million, according to U.S. Census Bureau projections.

Many older Americans are expected to downsize out of large homes to much smaller homes and apartments, especially to help with retirement funding, which creates a secular growth catalyst for public storage facilities.

However, it’s really hard to know when the growing supply and demand imbalance will abate. Until then, continued rent growth and occupancy rate deceleration seems likely, causing storage stocks to see their valuation multiples re-rate lower.

Fortunately, as industrial real estate prices have increased over the last few years, Public Storage’s disciplined management team has done the right thing by refusing to chase overpriced growth opportunities.

However, that has resulted in fewer growth opportunities, making the business all the more dependent on strong pricing power, which is weakening as well. Investors need to be prepared for top line growth to slow unless a decline in storage REIT prices allows management to acquire one of its major rivals such as Extra Space Storage (EXR), CubeSmart (CUBE), or Life Storage (LSI).

Finally, interest rates are a risk factor to keep in mind when evaluating almost any REIT because these businesses lean heavily on issuing debt and equity to fund their growth projects. When rates rise, REITs can face higher financing costs.

Fortunately, Public Storage has very little debt for a REIT, so the concern here isn’t so much with higher interest costs. Rather it’s that preferred stock investors, who provide almost all of the REIT’s growth funding, will demand higher interest rates on future preferred shares.

After all, if risk-free 10- and 30-year Treasury bonds see their yields rise to 4%, 5%, or even 6% in the years ahead, then the days of Public Storage being able to lower its funding costs by refinancing its preferred shares with ever lower yields will be over.

In addition, while Public Storage’s dividend is among the safest of all REITs, nonetheless higher rates on U.S. Treasury bonds mean that Public Storage’s share price might experience additional downward pressure, since investors almost always demand some kind of yield premium to compensate for the higher risk of investing in volatile stocks over Treasury bonds.

That could be great news for income investors who have a long time horizon and can take advantage of these higher yields. However, risk averse investors with a shorter holding period, such as retirees who need to periodically sell shares to fund living expenses, need to keep this share price risk in mind as they evaluate companies in this sector.

Closing Thoughts on Public Storage

There’s a lot to like about Public Storage. Its business is recession resistant, generates great cash flow, owns premier real estate locations, is managed very conservatively, has a solid balance sheet, and should have a long runway for growth given the industry’s fragmentation.

However, concerns over new industry supply are unlikely to dissipate anytime soon, especially as they continue weighing on the company’s growth prospects. The good news is that investors are largely aware of this risk and have already re-rated the valuation multiples of self-storage stocks lower.

What’s less certain is how long this imbalance will persist, especially since the industry is largely in uncharted territory from a supply perspective. Public Storage appears to have the financial strength and discipline to withstand almost any headwind while continuing to pay reliable dividends, but an investment in the company could require a good deal of patience as the storage industry’s unique fundamentals continue to adjust.

As always, maintaining a well-diversified portfolio with reasonable position sizes is especially important in these situations.

To learn more about Public Storage’s dividend safety and growth profile, please click here.

Leave A Comment