Founded in 1992, LTC Properties (LTC) is an internally managed real estate investment trust. The firm primarily invests in senior housing and skilled nursing facilities primarily through sale-leaseback (triple net lease) transactions, mortgage financing, and structured finance solutions including mezzanine (convertible debt) lending.

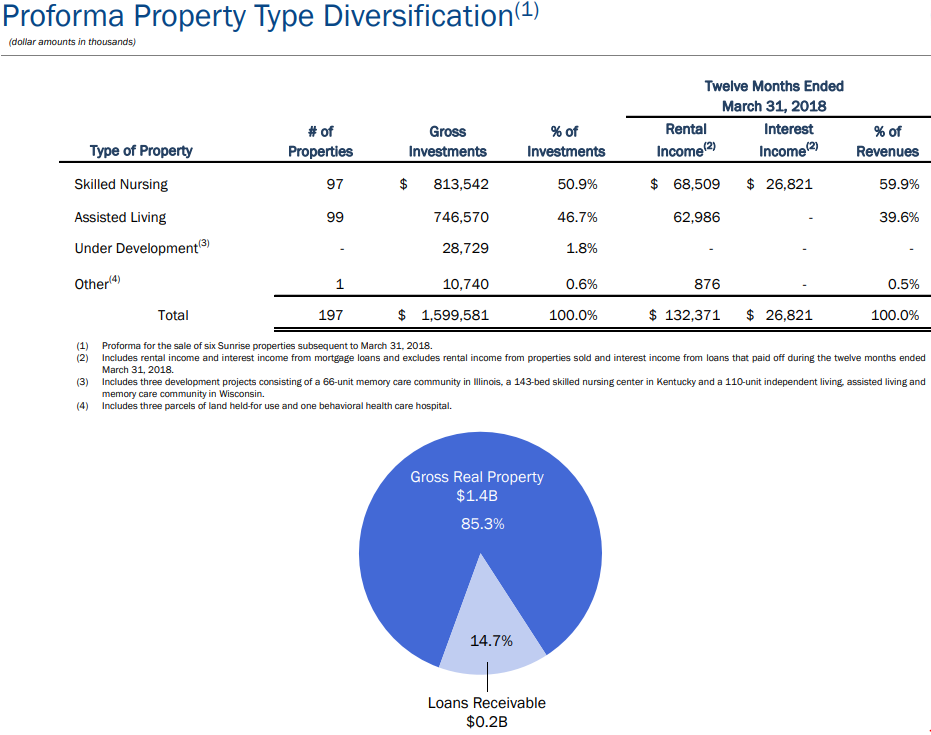

The REIT’s portfolio includes approximately 200 properties leased to 29 operators (regional and national chains) in 29 states. LTC targets states with the largest projected growth in the population of 80-plus year old Americans over the coming years (Texas, Michigan, and Wisconsin are its largest concentrations). About 70% of the firm’s properties are in America’s largest cities, with 50% in the country’s 31 largest metro areas.

The business model is primarily focused on owning senior housing properties, or SNH (40% of revenue), and skilled nursing facilities, or SNFs (60% of revenue). LTC operates under a triple net sale-leaseback model, meaning LTC will acquire a property from a facility operator and then lease back the use of that facility under long-term (10- to 15-year) master leases with annual rent escalators built in to counteract inflation.

Under a triple net lease model, the tenant is responsible for maintenance, taxes, and insurance, making LTC the landlord who collects stable, recurring, and high-margin rent (64% funds available for distribution, or FAD, margin).

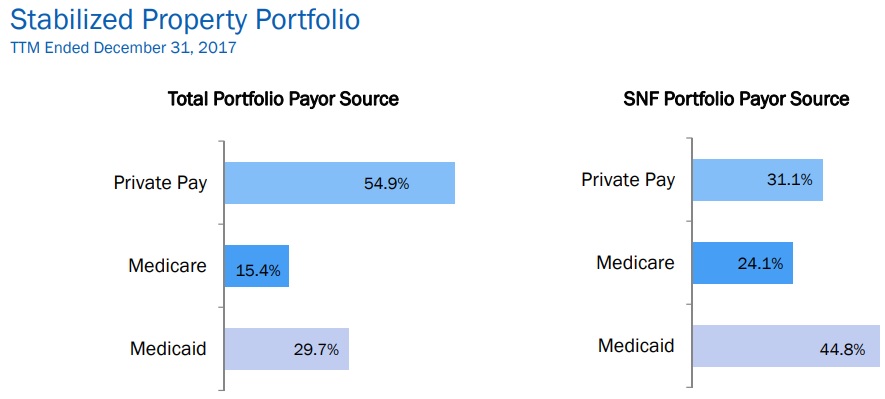

Approximately 55% of the REIT’s revenue is generated from private payers (individuals and private insurance) while the remainder is from Medicaid and Medicare. LTC’s relatively high exposure to government funding is due to its SNF properties, which generate nearly 70% of their revenue from Medicare and Medicaid programs. Senior housing properties are primarily funded by private sources.

Business Analysis

Many healthcare REITs are a potentially decent way to generate substantial dividend income (paid monthly in the case of LTC) from a major U.S. demographic trend: the aging of America’s population.

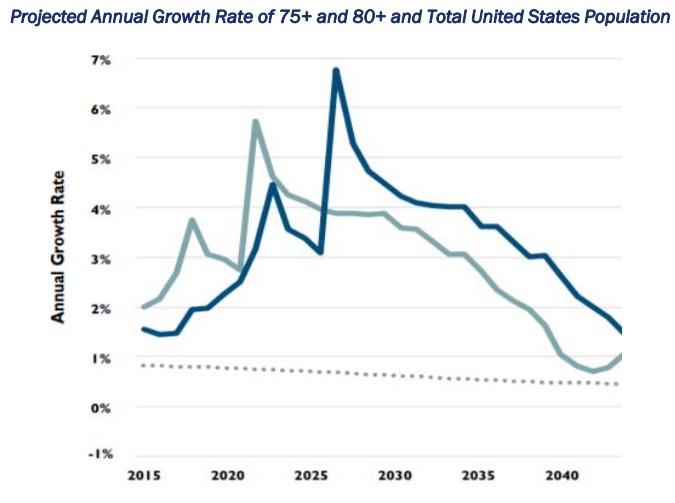

Medical REITs which specialize in senior housing and skilled nursing facilities should enjoy higher demand in the future since the growth rate of Americans aged 75+ remains much faster than the population as a whole.

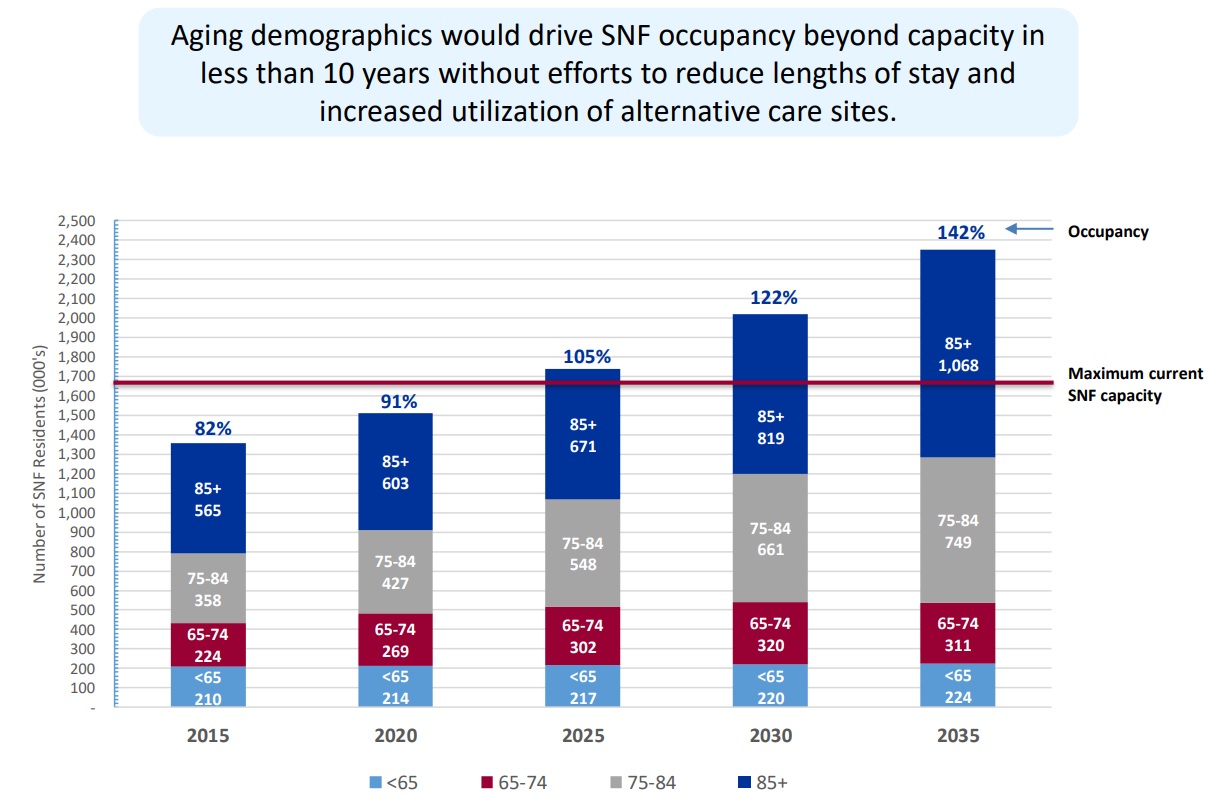

That trend is expected to last through at least 2050 and will mean that by 2040 the population of 75-plus year old Americans will more than double to reach about 40 million people by 2040. And since SNF capacity hasn’t changed much in the past decade, demand for SNFs is expected to exceed supply by around 2023 and continue rising for many years.

Tighter industry conditions would presumably result in stronger tenants and more opportunities for profitable growth in LTC’s largest segment (skilled nursing facilities drive 60% of revenue).

The same trends hold true for senior and assisted living, as well as specialized memory facilities dedicated to assisting the rising number of patients suffering from Alzheimer’s and other forms of dementia.

LTC is led by Wendy Simpson, an 18-year veteran of the REIT with over 25 years of experience in the medical industry. The REIT prides itself on a disciplined approach to growth that is predicated on good risk management and capital allocation discipline.

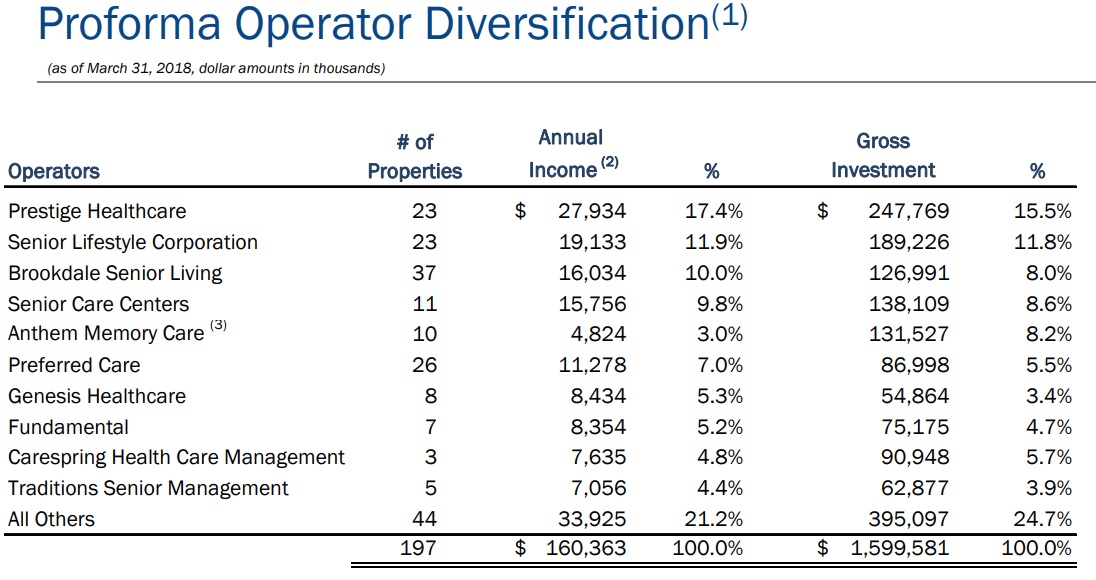

LTC is opportunistic in its investments, which includes a strong focus on good underwriting (making good deals) with an increasingly diversified group of regional and national operator chains. As you can see, only three of LTC’s tenants each generate at least 10% of the firm’s total income, which is less customer concentration than many of its peers.

Firms in the triple net lease medical REIT industry act as somewhat of a hybrid between a financial company and landlord. LTC provides capital to operators in exchange for income producing assets with fixed long-term revenue streams. The contracts are nearly all master lease agreements, meaning that an operator must pay full rent on all their properties including those that might not be profitable.

The REIT also uses cross collateralization agreements (corporate guarantees) to protect itself against operators that get in trouble and default. Approximately 97% of LTC’s rent is covered by such agreements.

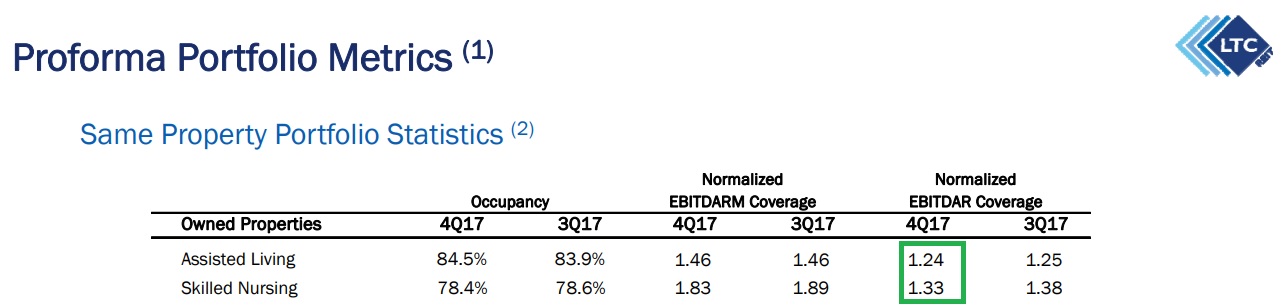

Since the stability of LTC’s funds available for distribution, or FAD (similar to free cash flow for a REIT), is predicated on the health of its operators, the REIT usually targets operators with an EBITDAR (earnings before interest, taxes, depreciation, amortization and rent) coverage ratio of 1.2 to 1.5. In the SNH and SNF industries, a rental coverage ratio of 1.2 or higher is considered healthy and sustainable, demonstrating management’s conservatism.

LTC essentially wants to buy properties from healthy operators who will make good tenants by being able to pay their gradually rising rent on time. These properties (and mortgage loans) usually generate cash yields of 7% to 9% compared to the REIT’s current average cost of capital of about 5%. As a result, each investment earns a gross investment profit of 2% to 4%.

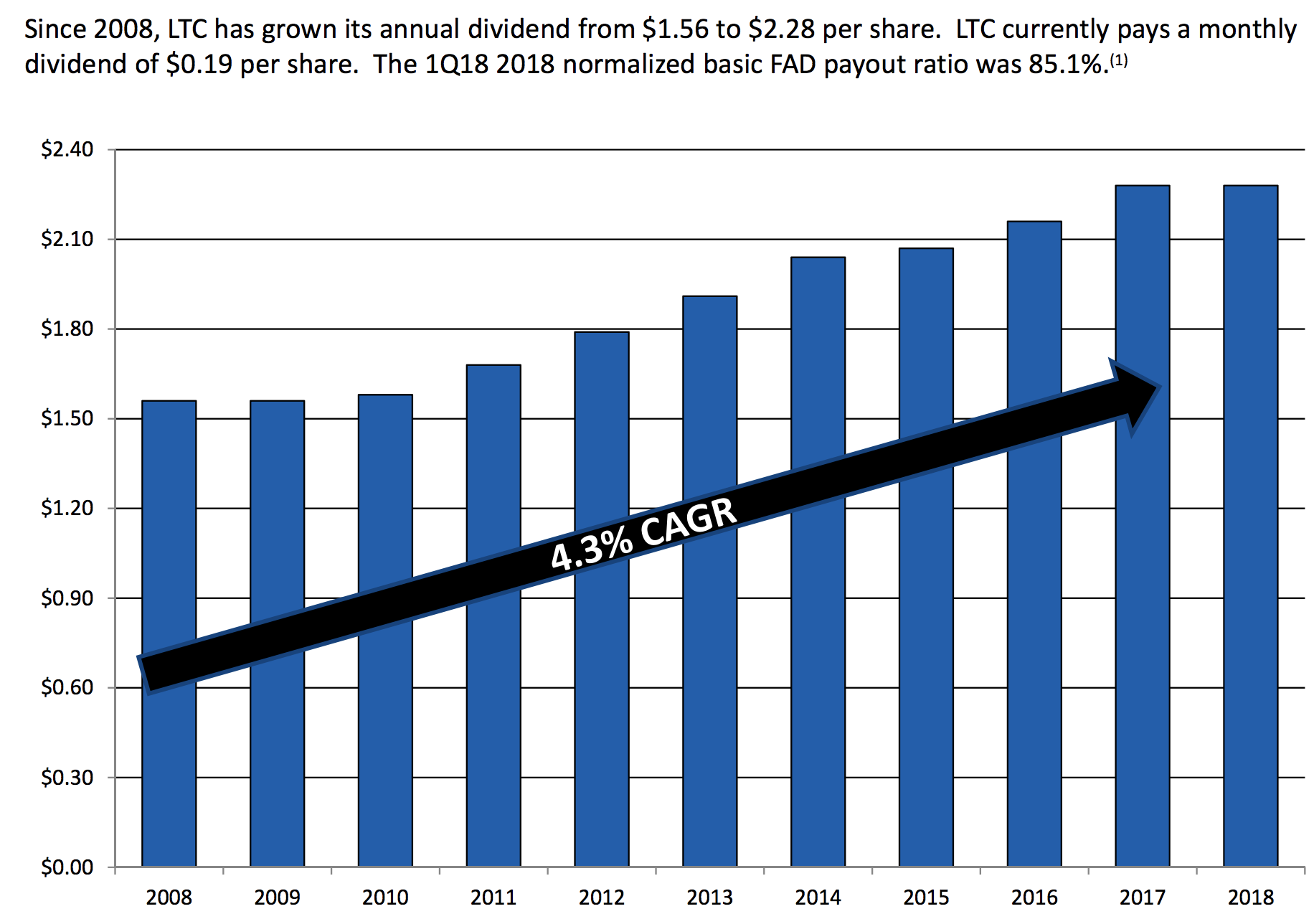

Over the last decade, LTC has proven itself to be capable of delivering consistent dividend growth of just over 4% per year. However, at times, such as during the financial crisis and in the past two years as the SNF and SNH industries have struggled, the firm’s dividend has remained frozen but covered by FAD per share (LTC’s current FAD payout ratio near 85% is a reasonable level for this industry).

The current trouble facing the SNF industry has largely stemmed from changes that the Centers for Medicare and Medicaid Services (CMS) has been making since 2011. Specifically, in an effort to both cut costs and improve patient outcomes, the government has been transitioning from a pay-for-service model to a more outcome-based approach.

This shift has resulted in shorter stays and lower reimbursements that have immensely stressed many operators’ margins. The aging population trend that is the backbone of the investment thesis for this industry is still several years away, too. As a result, SNF occupancy rates have declined from around 86% in 2014 to under 82% today as operators struggle with excess capacity. At the same time, rising labor costs in the medical field have been squeezing margins.

Not surprisingly, LTC and other SNF-focused REITs have been forced to undergo restructuring in the form of renegotiating leases with certain troubled operators. LTC has been recycling its portfolio in recent years, meaning replacing weaker operators with stronger ones, or selling older properties to use the proceeds to purchase newer ones leased to healthier occupants.

There are some signs the industry could be turning around thanks to higher government funding approvals and recent changes in CMS policy. Specifically, the latest budget deal will actually increase funding for SNFs by 1.6%.

More importantly, CMS seems to be nearing the end of its transition period and has settled on what it calls a patient-driven payment model (PDPM) that will go into effect in 2019. PDPM is generally viewed as favorable for the SNF industry because it will focus more on complex and higher margin care. That is expected to result in higher per diem day rates for the first 20 days of stay and includes provisions that allow the average SNF to cut annual costs by $12,000 per year.

What about senior housing, the other major component of LTC’s business representing 40% of its revenue? While senior housing is far less dependent on government funding, that industry too has suffered in recent years for different reasons.

Specifically, developers have overbuilt private payer supply which has caused industry occupancy to fall to a six-year low. Due to the high fixed costs of operating a facility (including paying rising labor costs), the slump in occupancy has been squeezing margins and lowering rental coverage ratios for the REIT’s operators.

In fact, LTC’s sixth largest operator, Anthem Memory Care, recently defaulted on its rent. The REIT has had to restructure its agreements with the company for the nine facilities it leases to it (two more under construction).

Fortunately, LTC’s overall tenant rental coverage remains relatively safe, especially on the senior housing side of the business which is enjoying higher and slowly rising occupancy (due to positive demographic trends).

However, while the skilled nursing portfolio has adequate rental coverage, LTC’s operators are still struggling with lower occupancy (industry average is about 80%) and falling rental coverage due to declining margins.

During the first quarter conference call, management indicated that this negative trend in rental coverage might continue for a few more quarters before stabilizing. The REIT is thus guiding for about a 2% decline in cash flow per share in 2018 before it hopefully returns to growth in 2019.

In other words, LTC is in a turnaround year. Investors will need to be patient as the industries in which it operates find a bottom and management adapts to challenging industry conditions.

The good news is that during LTC’s turnaround plan, the firm’s dividend will likely remain safe. In addition, the REIT continues to enjoy a strong balance sheet and has ample access to low cost liquidity (cash and remaining borrowing power on its credit revolver with an average interest rate of 3.2%).

LTC has $800 million in total liquidity and enjoys far better relative debt metrics than most of its peers, providing more flexibility to help it weather tough times.

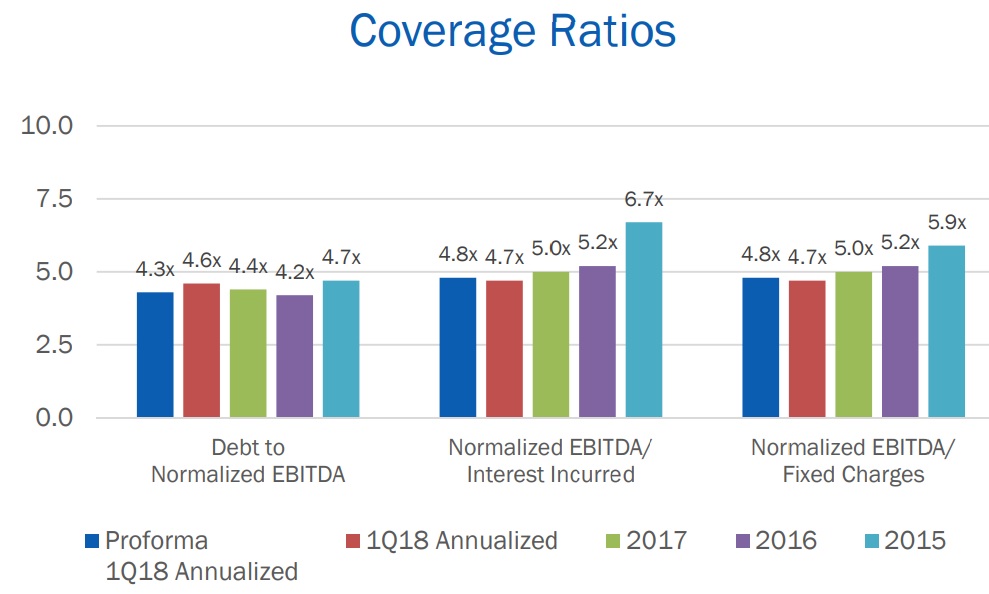

For example, LTC’s debt/EBITDA ratio of 4.3 is down significantly due to the recent sale of its troubled (and older) Sunrise leased properties. That’s compared to an industry average leverage ratio near 6.0. In addition, LTC’s fixed charge coverage ratio (EBITDA minus unfunded capital expenditures and distributions divided by total debt service) is 4.8, compared to most of its peers whose fixed charge ratios average 3.5.

As importantly, these ratios have remained relatively stable over time despite the challenges facing the industries in which LTC operates.

Management remains committed to recycling its lower quality properties with weaker tenants while acquiring and investing in newer properties leased to stronger operators at profitable rates. The firm currently has an investment pipeline of $50 million, and analysts expect that to accelerate in 2019 to drive close to 10% growth in cash flow per share.

Over the long term, LTC seems likely to deliver low to mid-single-digit annual growth in FAD per share. Rising demographics will hopefully improve the industry’s occupancy rates eventually, and slightly faster growth in government reimbursement rates under the CMS’s latest policy proposals should begin taking holding in 2019.

If these growth drivers play out as expected, management executes on its turnaround plan, and industry conditions don’t get any worse, than LTC Properties might make a decent high-yield source of monthly dividend income.

However, there are several risks to the company’s plan, which ultimately makes LTC Properties a medium-risk stock that may not be appropriate for very conservative investors.

Key Risks

Despite management’s bullish outlook, LTC faces short, medium, and long-term risks.

In the short term, there is the risk that continued deterioration in its SNF business will extend the firm’s turnaround period, meaning the company will have to continue selling properties with weaker tenants. This kind of portfolio churn can result in flat or even falling cash flow per share, especially for a smaller REIT such as LTC.

For one thing, LTC has a relatively high concentration of rent coming from its largest operators, meaning they have stronger bargaining power in the event that their margins and rental coverage ratios decline.

In addition, LTC’s SNF property portfolio has an average age of 22 years, which is relatively old (the firm’s assisted living properties are 11 years old on average). Remember that tenants are responsible for maintenance under LTC’s business model, so older properties are more expensive to run. This not only puts additional pressure on a tenant’s margins, but it also makes them less likely to renew leases when they expire or accept further rental hikes.

LTC has some major lease expirations coming up in 2020 and 2021 when 17.7% of its revenue will be up for renewal. While the newer properties LTC is buying have an average age of 5 years or under, its large legacy portfolio (mostly from mid-1990’s) could ultimately result in the REIT having a hard time negotiating rents at similar rates in a few years.

That’s unless the SNF industry has indeed turned the corner and is performing better in a few years as America’s population ages further and boosts occupancy rates. While numerous medical REITS have reported that industry conditions appear to be stabilizing, it’s still too early to tell whether or not SNFs and medical REITs in general have turned the corner.

For one thing, CMS’s new patient-driven payment model doesn’t go into effect until 2019, which is why management expects SNF rental coverage to continue to decline through most of 2018. In addition, LTC’s SNF facilities are struggling with below average occupancy that has yet to bottom.

Even when it does, at its current low levels SNF operators are likely to continue struggling with profitability thanks to accelerating wage growth. In the medical field, and especially in the stressful SNF industry, wages are likely rising even faster. This could offset some of the benefits from rising occupancy levels fueled by strengthening demographic trends.

Perhaps most importantly, there is always the risk that CMS (the Federal government) will decide to change its payment model yet again as it has been doing for seven years now. Meanwhile, those cost savings that PMPD are supposed to usher in are theoretical averages, and there is no guarantee that LTC’s operators will actually be able to accomplish them. Remember the new Medicare/Medicaid policy won’t go into effect until next year, and cost savings take time to orchestrate.

In the meantime, while LTC isn’t in a liquidity trap like some other medical REITS, be aware that close to 20% of its debt is variable rate. Therefore, rising interest rates represent a potential risk as well, especially given the firm’s falling cash flow over the short term.

REITs can only grow their dividends safely over time if FAD per share is rising because the cash yield on new properties and loans is higher than their total cost of capital. LTC’s share price has been lowered by the REIT bear market which has hit medical REITs especially hard.

While LTC can still grow profitably for now, rising rates reduce its margins on new investments, meaning FAD per share growth might be lower than investors expect. Factor in the uncertainty surrounding how successful LTC’s turnaround will be, how long until the SNF and SNH industries recover, and its large lease maturities in 2020 and 2021, and LTC’s dividend might remain frozen for several more years.

Meanwhile, investors must contend with the government’s ongoing desire to reign in Medicare and Medicaid spending, which could come under increasing pressure over the long term.

Closing Thoughts on LTC Properties

The underlying business model of triple net lease medical REITS is, in principle, an enticing way for investors to gain generous and rising income while benefiting from the secular trend trend that is America’s aging population.

LTC appears to be one of the better choices in this industry thanks to its strong balance sheet, conservative management team, and dividend, which is likely to remain safe during the current turnaround.

However, keep in mind that those factors might just make LTC one of the nicer houses in a bad neighborhood. There is still a lot of uncertainty surrounding the short and medium-term health of the SNF and SNH industries which means that LTC’s long-term growth is far from assured.

Investors who are comfortable with the risks facing this industry might want to consider National Health Investors (NHI), Ventas (VTR), or Welltower (WELL) instead. These firms are larger, possess stronger property portfolios, and have less exposure to government funding, making them more appealing for conservative income investors.

To learn more about LTC’s dividend safety and growth profile, please click here.

Leave A Comment