Kroger (KR) was founded in 1883 and is the second largest food retailer after Walmart with over $120 billion in annual sales. The company operates almost 2,800 supermarkets, of which more than 2,200 have pharmacies and nearly 1,500 have fuel centers. Kroger’s grocery stores are located in 35 states and serve more than 9 million shoppers per day.

The company’s stores operate under the brand names Kroger, Harris Teeter, Fred Meyer, Mariano’s, Pick ‘n Save, Metro Market, Pay Less, Smith’s, Owen’s, Baker’s, Fry’s, and others.

Over 25% of Kroger’s supermarket sales are generated by private label corporate brands, and approximately 44% of its private label grocery brands are manufactured at the company’s 37 food production plants. This vertical integration benefits Kroger’s margins.

In addition to supermarkets, Kroger operates (by franchisees or through its subsidiaries) 784 convenience stores, 323 fine jewelry stores, and an online retailer. All of the company’s revenue is generated in the U.S., and 97% of sales are from its core retail businesses.

Note that Kroger decided to exit the convenience store business in the fourth quarter of 2017 by selling it to the England-based EG Group for $2.15 billion. This business generated $4 billion in annual revenue and the proceeds ($1.75 billion post tax) will go toward a new $1.2 billion share buyback authorization as well as paying off $500 million in debt. Kroger’s supermarket fuel centers were not included in this sale.

Business Analysis

The grocery business is marked by severe challenges for companies including: fierce competition, razor-thin margins, high fixed costs (Kroger estimates that it costs close to $20 million to open a single supermarket location), perishable inventory, and increasing disruption caused by online grocery sales.

Consumers typically have a number of grocery chains to shop at in their local markets, and most are looking for the best quality produce available at the lowest prices. Differentiation can be difficult, and Walmart has wiped out many grocery chains based on price alone for decades.

Kroger has adapted to these challenges in part by acquiring some of its rivals in an effort to maximize its market share. Some of the company’s more notable deals in recent years were its purchases of Harris Teeter in 2014 for $2.4 billion and Roundy’s for $800 million in 2015.

Thanks to also opening numerous stores within 1 to 2.5 miles of most of its customers, Kroger is the No. 1 grocer in 46 of its 51 largest markets and No. 1 or No. 2 in 98 of its top 120 markets. The company also enjoys No. 1 or No. 2 market share position in 52 of its 69 minor markets.

As the largest player in most of its locations, Kroger’s scale helps it acquire products at lower costs and spread its fixed costs out more efficiently than smaller rivals.

However, Kroger knows that competing on price is ultimately a losing game. Instead, the company has instilled a culture focused on knowing the customer best to improve satisfaction and loyalty.

Kroger invests heavily in technology to understand what consumers are buying and to capitalize on evolving shopping trends such as healthy eating and e-commerce.

In fact, Kroger’s customer analytics and insight business, which employs over 500 people, was named one of the Top 100 places to work by Computerworld magazine in 2016.

Kroger also bought consumer research giant and longtime partner 84.51 degrees in 2015. This company is now Kroger’s in-house data analytics firm, which is fed by over 25 million digital accounts. 84.51 provides Kroger with deep insights into customer preferences and regional ordering patterns, which can be used to maximize the value of its online sales channels like ClickList and Harris Teeter ExpressLane.

These platforms offer personalized online ordering for in-store pickup at over 1,000 stores, and home delivery (through Instacart) is available at more than 850 locations. The success of these online programs helped drive 90% online sales growth for Kroger in 2017, and the company plans to add 500 new pickup locations in 2018.

It’s far too early to judge which companies will have the most success in the online grocery business, but Kroger brings a track record of getting trends right – even if it’s not the first mover.

The company is also experimenting with something it calls Scan, Bag, Go shopping technology in which customers use portable scanners to scan items as they place them in carts while shopping. The system was designed in-house and also integrates with a customer’s online profile to provide coupons and let shoppers know what is currently on sale that their past purchases indicate they might be interested in.

The idea is that this technology (tech investment up 200% in 2017 with further plans of a 50% increase in 2018) allows customers to avoid scanning items at busy checkout lanes. Scan, Bag, Go will be rolling out to 400 stores in 2018 in large markets like: Atlanta, Cincinnati, Columbus, Dallas, Houston, Louisville, Nashville, and Michigan.

Overall, Kroger’s goal is to maximize economies of scale and then pass on cost savings in the form of lower prices. The company calls this its “customer first” approach and claims it’s the key reason for its impressive streak of 13 years of rising market share.

In anticipating of tax reform passing in the fall of 2017 (which would cut its tax rate from 33% to 22%), Kroger announced its “Restock Kroger” growth plan. The plan includes several initiatives and will be funded primarily by Kroger’s $250 million in annual tax savings and cost reductions.

First, Kroger plans to maximize the use of its large data collection, via its 84.51 platform. This deep data collection and analytics business is what allows the grocer to send over 3 billion personalized shopping recommendations to customers each year.

Specifically, management wants to use more granular shopping data from its membership programs to optimize what products it stocks and where, as well as better compete on price. Since 2001, Kroger has invested $4 billion into its Smart Pricing initiative which helps it to avoid losing customers by matching prices of rivals who may be undercutting it at nearby competing stores.

This first part of the “Restock Kroger” plan also wants to highlight the company’s private label “Our Brands” products which made up 26% of total sales in 2017. Kroger sells over 15,000 products under its own private labels, which carry higher gross margins. If Kroger can win more customer loyalty to its brands, then it might be able to increase its buying power over suppliers and ease the price wars it’s currently waging with rival grocers.

The second part of the plan is to invest heavily into its stores to make them more profitable in a future dominated by automation and online sales. For example, Kroger will be redesigning the front end of many of its stores to offer more self checkout lanes. In 2017, the company did a pilot program at 20 stores that it deemed a success and will be rolling it out to 400 more stores in 2018.

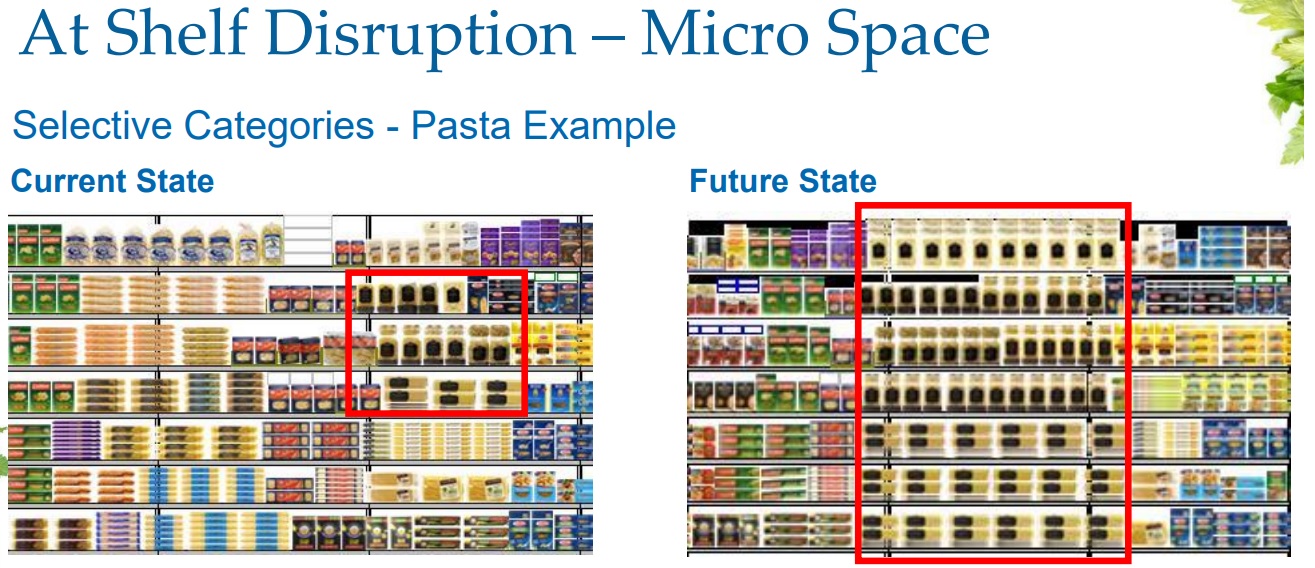

In addition, the company will be investing in the Internet of Things, or IoT, meaning internet-connected sensors, advanced video monitoring, and data analytics, all with the focus of helping customers shop more conveniently and checkout faster. These investments will also allow the company to optimize its shelf space to boost overall sales.

The company believes that this advanced data approach can create alternative sources of profits as well, including media and advertising revenue from in-store displays.

Kroger also wants to reinvest more in its workers, including an extra $500 million targeted between 2018 and 2020. The idea is to increase pay but also make Kroger more of a career and less of a job, with employees climbing the ladder to create better customer experiences (via happier and more productive workers).

Kroger estimates that most of its managers have been with the company for 12.3 years and wants to increase that figure significantly going forward. To accomplish this, the company plans to pay its workers an average of $20 per hour in wages and benefits by 2020, up from an average compensation of $14 per hour today.

The grocer will also offer employees a higher 401K match and help pay for a portion of employees’ continuing education, including GEDs, MBAs, and certification programs.

By attempting to lower its employee turnover, the company hopes to create a more experienced workforce with greater institutional memory that will help Kroger better compete in this fast-changing industry. This is similar to the successful approach that Costco (COST) has taken since its founding.

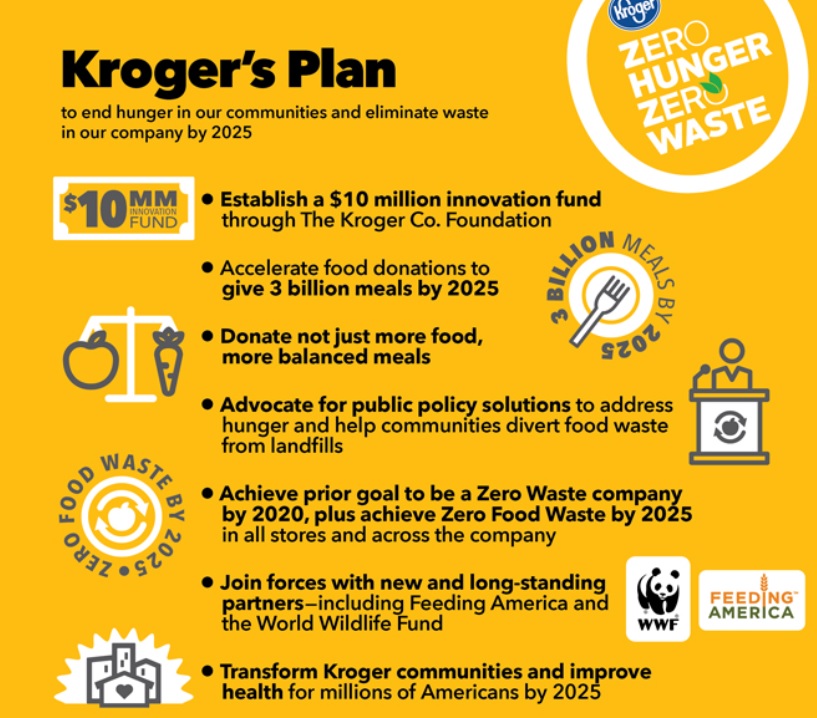

Finally, Kroger plans to increase goodwill in its communities as well as eliminate food waste via its Zero Hunger/Zero Waste Plan.

About 40% of US groceries go uneaten and get thrown out. Kroger plans to partner with various charities and utilize its 84.51 data platform to try to maximize how much of this thrown out food gets donated to the Americans who are in need. The plan will be part of the company’s broader cost-cutting initiative to improve its supply, logistics, and retail operations to reduce costs and stabilize margins.

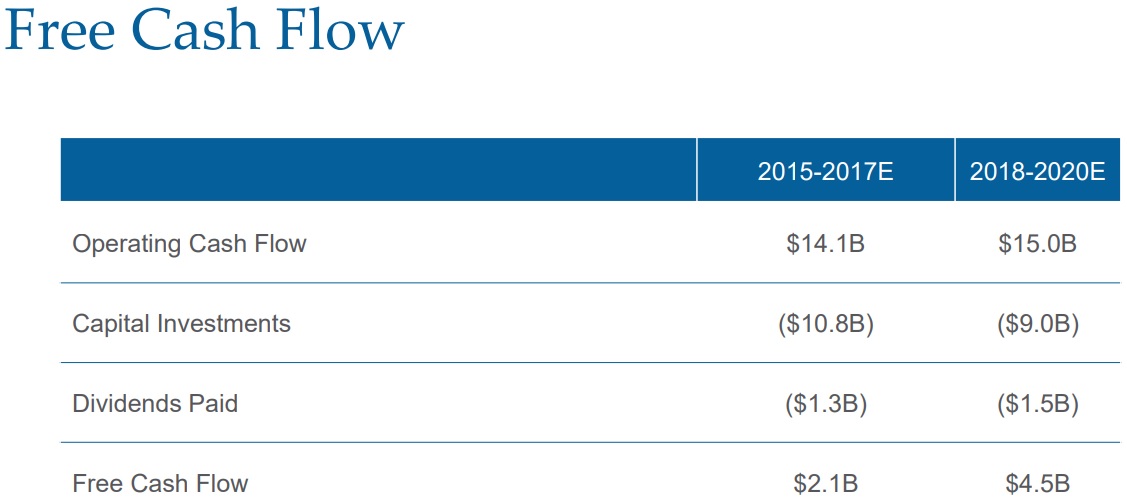

All told, the company thinks that “Restock Kroger” will cost $9 billion over the next three years but will allow it to cut $400 million in total costs over that time (about $133 million in annual saving). This, combined with a lower corporate tax rate and moderating capital investments, is why Kroger thinks it can double its free cash flow over the next three years.

That’s an impressive goal and, if successful, will go a long way to allowing Kroger to keep increasing its payout as it has been doing for every year since 2006.

Overall, as long as Kroger continues to invest in its existing supermarket locations and stay on top of evolving customer shopping preferences, the company should remain relevant and be positioned to protect its market share.

However, Kroger faces numerous challenges that could make profitable growth harder to come by going forward.

Key Risks

Kroger’s business results can be impacted by a number of transitory factors over the short term.

Poor weather, low food inflation, lackluster consumer confidence, and volatile fuel margins are just a few of the key uncontrollable factors that can hurt Kroger’s earnings any given quarter.

However, over the long run, none of these issues should impact Kroger’s earnings power and growth opportunities.

In fact, Kroger has grown its market share for 13 consecutive years, fueled in part by acquisitions. Despite its top line success in this challenging industry, the company has struggled to grow its earnings and free cash flow in recent years. Management expects earnings per share to be flat or slightly down in 2018 compared to 2017, too.

Despite its enormous scale, Kroger is struggling in a highly competitive environment and is currently embroiled in a price war for market share. Management has said that cutting prices to compete on market share is how it “invests in price”. Pricing actions are unfortunately a necessity since rivals such as Aldi and Lidl, private grocery chains that focus on bare bones stores and offering the lowest possible cost, are planning major U.S. expansions in the coming years.

The company’s price cuts are coming at time when Kroger is increasing its spending to improve its growth (especially online) and reduce its costs. However, these investments will take several years to bear fruit. As a result, Kroger’s operating margin in 2017 was a miniscule 1.7%, its lowest level since 2012, and shareholders’ faith in management’s long-term plans is being tested.

The Wall Street Journal put it well:

“The largest U.S. supermarket chain is struggling to invest in online operations and introduce new products at its 2,800 stores while also generating enough profit to keep investors happy.”

Kroger’s financial flexibility is also somewhat strained by its balance sheet. The company has a net debt/EBITDA (leverage) ratio near 4.0 (including unfunded pensions and off-balance sheet debt), which is meaningfully above the industry’s average and management’s target leverage range. Kroger does have a BBB investment grade credit rating, but it is just two levels away from junk bond status.

Given the capital intensity of the grocery business and Kroger’s large debt burden, the company may need to use its growing free cash flow to pay down its debt rather than grow the dividend quickly, especially if interest rates rise.

And that’s assuming Kroger’s turnaround plans meet management’s objectives, which is far from certain. Even if they do, the company still faces major competitive challenges.

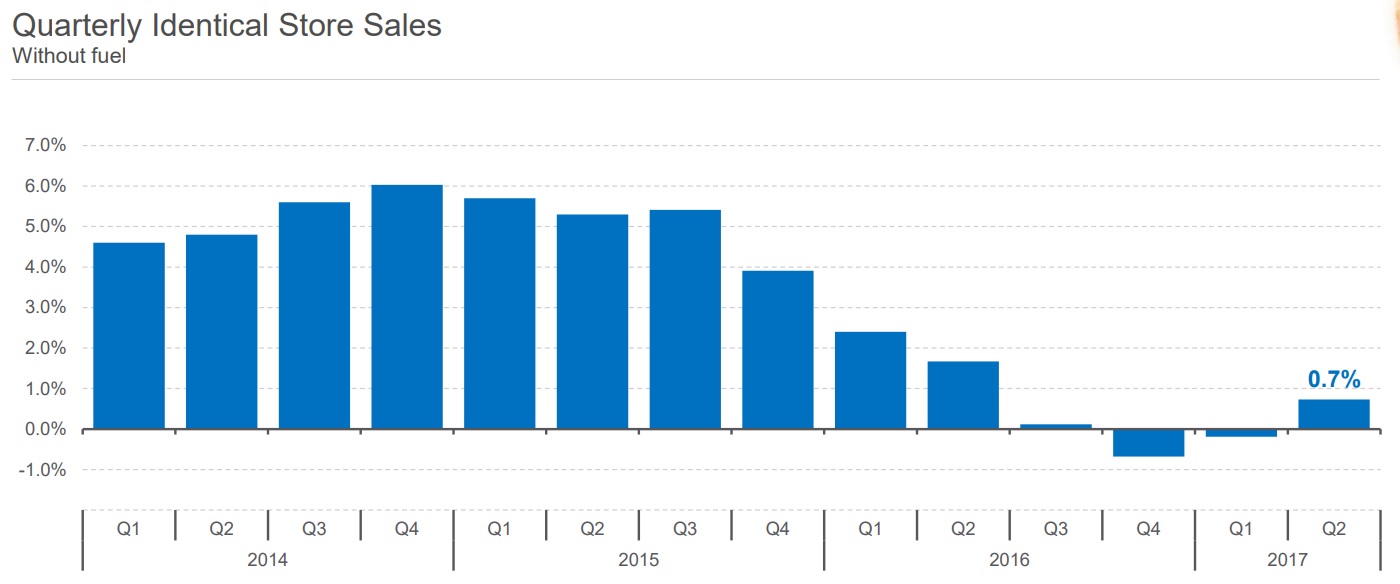

Despite the success of ClickList and nearly doubling of online generated sales in 2017, for example, Kroger’s same-store comps (excluding volatile fuel sales) were just 1%. And in 2018, management expects 1.5% to 2% same-store sales growth.

While 2% comps growth is an improvement compared to the last few years, the more competitive nature of the industry likely means Kroger’s glory days of 4% to 6% comps are permanently behind it.

The chart above shows the struggles that a large grocer like Kroger has. The mature nature of the business means that earnings growth primarily comes from continued expansion (opening or acquiring more stores) and margin improvements such as cost cutting (economies of scale).

Kroger’s existing market positions are strong, but profitably expanding into new areas is very difficult. Without acquisitions, Kroger’s store count has essentially remained stagnant for more than a decade.

This wasn’t always the case for Kroger. At the end of 1993, Kroger had 2,200 locations. Its footprint expanded by more than 60% over the next decade to hit 3,600 locations in 2004. Since then, organic store count (excluding its larger acquisitions of Harris Teeter and Roundy’s) has essentially treaded water near 3,600 locations (including its convenience stores, which are being divested).

In other words, future earnings growth will need to come from same-store sales growth (online orders, technology improvements, favorable food inflation and fuel margins), continued share repurchases, and the expansion of newly-acquired store concepts such as Mariano’s.

If I would ever consider investing in a retailer that operates in extremely competitive markets, I would prefer if the company had a differentiated enough concept to profitably continue growing its store count.

Tesco, a large grocery retailer based in Britain, highlighted just how difficult it can be to profitability expand operations. The company attempted a multibillion-dollar expansion into the U.S. that resulted in a bankruptcy filing in 2013.

Even worse, Tesco began losing market share to competitors Aldi and Lidl in its home market, sparking a major pricing war. Tesco ultimately slashed its dividend by 75% despite having increased its dividend for more than 25 consecutive years.

While demand for grocery products is usually stable, pricing pressure can be extreme enough to crimp profitability. Since most of Kroger’s costs are fixed, a drop in grocery prices is especially painful, and it’s harder for the company to adapt its business model.

Meanwhile, major rivals like Target (TGT), Walmart (WMT), and Amazon (AMZN) are investing just as aggressively into optimizing their online sales channels, including for groceries.

Those companies have been seeing success as well with online sales growth of 20% to 60%, but margins have not been improving as a result. The lack of profit growth isn’t too surprising since retail and grocery margins have historically been low. The high level of competition often results in most cost savings and efficiencies eventually getting passed on to consumers.

With that said, Kroger is arguably one of the best-managed grocers in the industry thanks to its scale, vertical integration, strong customer satisfaction ratings, focus on technology, long operating history, and somewhat differentiated in-store experience.

However, the business faces a number of challenges outside of its control and operates in a brutal industry. Investors considering the stock need to closely watch how it responds to an increasingly competitive retail environment and the secular changes that are impacting how consumers shop (e.g. e-commerce).

Closing Thoughts on Kroger

Kroger has proven itself to be a survivor and innovator in a cutthroat industry. While the firm’s dividend appears safe and is likely to grow slowly over time, investors need to realize that the grocery industry has become far more competitive in recent years, thanks largely to the rise of online rivals like Amazon and low-cost grocers such as Aldi and Lidl.

And with other traditional retail giants, such as Walmart, Target, and Costco, also gunning for the same grocery customers and engaging in price wars, Kroger will have to continue investing heavily in its technology, stores, and workforce in order to remain competitive.

The company’s investments are a prudent long-term move by management to protect Kroger’s market share, but they will weigh on the firm’s profitability for at least a couple of years. And that’s assuming Kroger’s technology investments successfully position the company to be a leader in online grocery, which is far from guaranteed.

At the end of the day, it’s hard to pull the trigger to invest in a supermarket chain. While Kroger has rewarded shareholders with tremendous returns over the last decade, profitable growth could is likely to be more challenging over the next 10 years due to increased competition, stagnant new store growth, and evolving consumer shopping preferences.

Kroger seems like more of a mature, defensive cash cow, but its low dividend yield does not reflect that status. For now, investors may be better off invested in other quality dividend stocks that have greater pricing power, healthier balance sheets, stronger moats, faster dividend growth profiles, and numerous opportunities to increase their long-term earnings power.

To learn more about Kroger’s dividend safety and growth profile, please click here.

Moved out of KR and bought PEP on 5/7/2018. I agree with KR’s competitive vulnerability and found PEP to be head and shoulders above KR on Simply Safe metrics. Also believed KR at fair value or higher and PEP to be undervalued. Trying to sell high and buy low. Although PEP is in the Top 20 Portfolio and am moving my portfolio to more closely align with the Conservative Retirees Portfolio, I think it is a fit.