Founded in 1912, Illinois Tool Works (ITW) is one of the world’s largest industrial component manufacturers, operating over 500 facilities around the globe (roughly half of sales are in North America).

The company has grown into an extremely diversified manufacturer of specialized industrial and consumer equipment and consumables with a presence in many different end markets – automotive, construction, manufacturing, food & beverage, and more.

Illinois Tool Works consists of hundreds of businesses it has acquired over the years. It runs a unique decentralized operating structure that empowers acquired businesses to maintain most of their culture and operations while taking advantage of ITW’s resources to better serve their customers’ needs.

The company’s 85 subsidiaries operate through seven business segments:

- Automotive OEM (24% of sales, 24% of operating income):produces plastic and metal components, fasteners, and assemblies primarily for automotive original equipment manufacturers.

- Food Equipment (14% of sales, 14% of operating income):produces commercial food equipment and related services, including warewashing equipment, cooking equipment (e.g. ovens, broilers), refrigeration equipment, and more. Customers include restaurants and food retail markets.

- Specialty Products (13% of sales, 14% of operating income): the businesses in this segment produce beverage packaging equipment and consumables, product coding and marking equipment, and appliance components and fasteners.

- Test, Measurement & Electronics (14% of sales,14% of operating income): sells equipment, consumables, and related software for testing and measurement of materials and structures, as well as equipment and consumables used in the production of electronic subassemblies and microelectronics.

- Welding (11% of sales, 13% of operating income): sells welding equipment, consumables, and accessories for a wide array of industrial and commercial applications.

- Constructuction Products (11% of sales, 10% of operating income): produces construction fastening systems and truss products used primarily in construction markets.

- Polymers & Fluids (12% of sales, 10% of operating income): sells adhesives, sealants, lubrication, fluids, and polymers for auto aftermarket maintenance and appearance.

Business Analysis

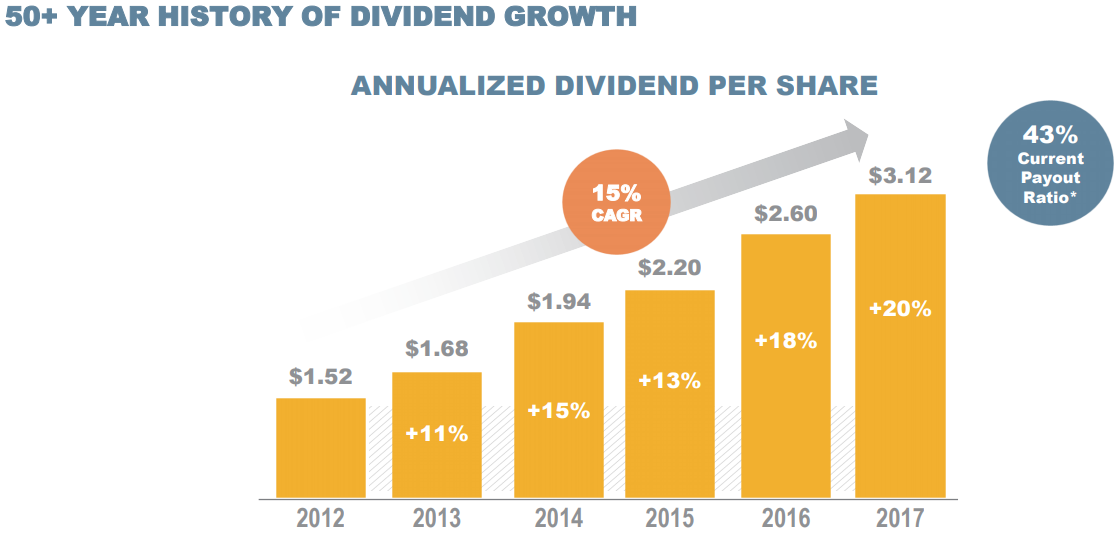

Illinois Tool Works is arguably one of the strongest, most reliable companies that a dividend growth investor can find in the industrial sector. In fact, the firm has been growing its annual payout every year since 1964 and is a member of the dividend kings group of stocks.

Over the years, management has done an excellent job creating and evolving a successful corporate culture that has helped ITW grow steadily even during economic and industry downturns.

In 2013, Illinois Tool Works adopted a new restructuring plan that it has since invested over $3 billion into. The three-pronged plan included three initiatives:

- 80/20 Front to Back Process

- Customer-Back Innovation Approach

- Decentralized Entrepreneurial Culture

In 1985, the company adopted what it calls its “80/20” strategy in which the firm began careful optimization of its largest, fastest growing, and most profitable segments, while minimizing the costs and distractions from its 20% worst performing segments, most of which are ultimately sold off.

Illinois Tool Works has been an aggressive acquirer of numerous small companies, buying up more than 600 businesses over the past 25 years. While this strategy was successful, it also resulted in a rather bloated company. Management realized the need to evolve ITW’s corporate and business structures once more to improve the company’s future growth and profitability potential in recent years.

The company used advanced data-driven statistics to determine which 20% of its businesses were its weakest and biggest distractors (and operating in highly commoditized and slow growing markets), ultimately selling over 30 of them. In 2013, for example, ITW divested its industrial packages business which made boxes.

All told, the company eliminated about 80% of its least profitable product lines across all segments and divested approximately 25% of its businesses between 2011 and 2014.

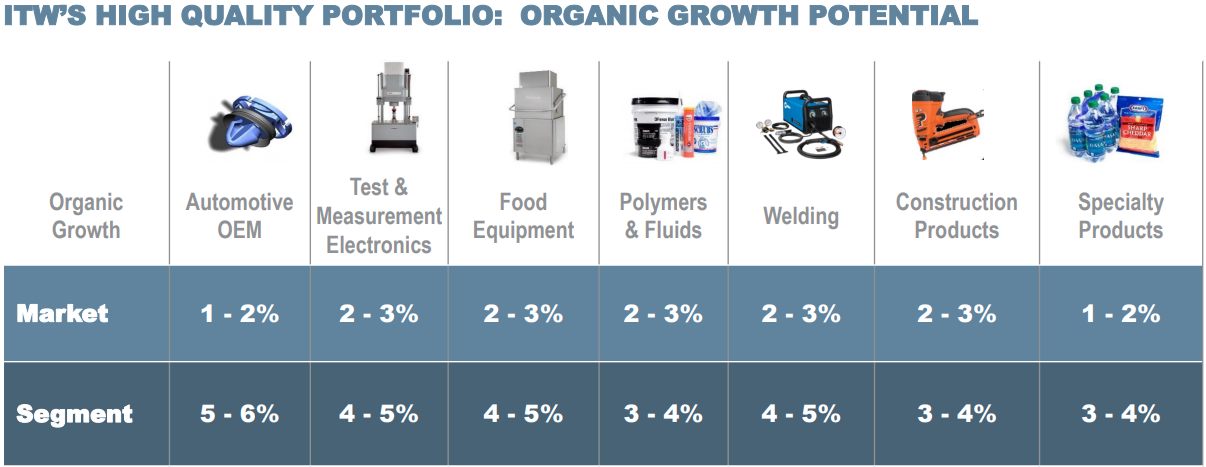

Today, Illinois Tool Works is focused on just those segments and products with much stronger organic growth potential, and its subsidiaries have organic growth potential that is faster than the industry’s average rates.

As you can see, most of the markets ITW operates in are growing at 1% to 3% annually, but the company’s own segments usually grow sales at 3% to 6% per year. Management expects the company’s superior growth to continue in part because ITW’s market share ranges from 15% to 25% in most business segments, allowing room for expansion.

In automotive, for example, Illinois Tool Works is averaging sales of $35 per vehicle. Management thinks the company can eventually increase that figure to $230 per vehicle, in part by developing products to focus on electric vehicles and to serve the fast-growing Chinese market.

Solid growth will be supported by the second component of management’s plan: a customer-back approach to product development. In business for over a century, ITW maintains very long-term relationships with many of its customers. Deeply understanding its customers’ needs helps Illinois Tool Works determine which areas it should focus its R&D budget on.

For example, in 2017 the company spent $225 million on new product development, or just 1.6% of revenue. However, because of how targeted that spending was, ITW’s relatively small investment generated over 1,600 patents, increasing the firm’s total patent portfolio by nearly 10%. More impressively, over half of ITW revenues covered by patents or proprietary trade secrets

Simply put, Illinois Tool Works is able to efficiently direct its resources with laser-like precision and generate strong intellectual property that yields higher-margin products. Most of the company’s tailor-made components focus on mission-critical applications. Customers are often reluctant to switch suppliers and risk disruption to their businesses, especially since ITW’s components typically represent a relatively small proportion of a product’s total cost.

The final part of the restructuring initiative streamlined management. Due to its hundreds of acquisitions over the years, Illinois Tool Works had over 800 regional subsidiaries. Efficient management became a major challenge.

As a result, ITW streamlined those subsidiaries into 85 global divisions and gave management simple but clear organic growth, operating margin, and return on invested capital targets to hit each year. Rather than micromanage its business units, Illinois Tool Works lets them operate autonomously, which is a similar strategy that Warren Buffett’s Berkshire Hathaway (BRK.B) uses to great success.

One of the major focuses managers were given was strategic sourcing of components and raw materials from the lowest cost providers. By leveraging the company’s scale, yet adhering to its strict quality standards, the firm generated a 3% reduction in supply costs. Thanks to such initiatives, Illinois Tool Works has been able to achieve $1 billion in annual cost savings since 2013.

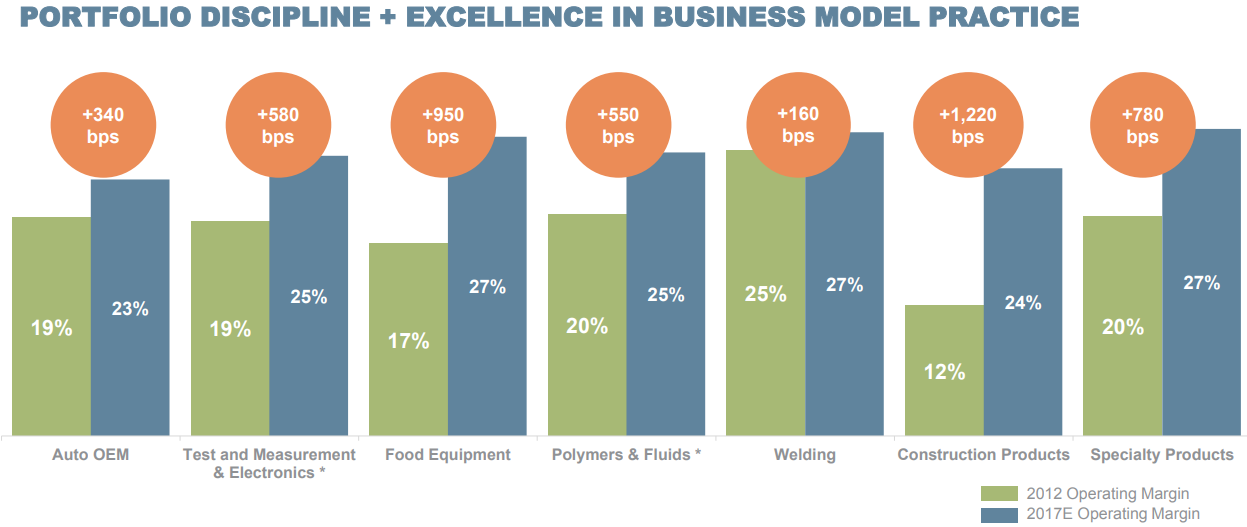

The results of the firm’s three-part turnaround plan have been impressive. Operating margins improved meaningfully across each segment over the last five years, for example.

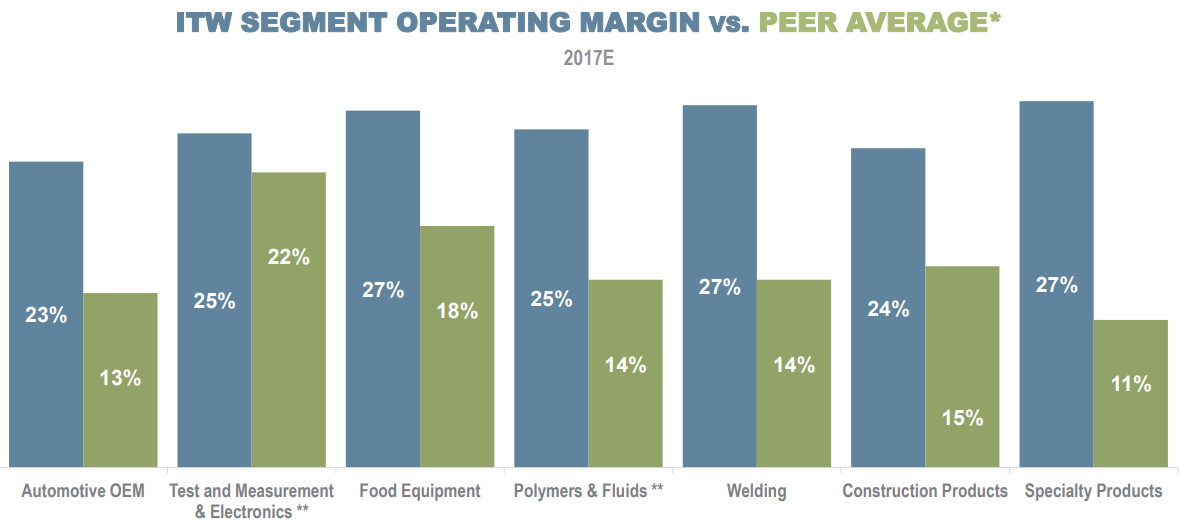

In fact, each of the company’s segments has some of the highest profitability in their respective industries.

Company-wide operating margins increased from 17% in 2012 to 24% in 2017, allowing management to reward investors with fast dividend growth while still retaining over half of its free cash flow to reinvest in its business later on.

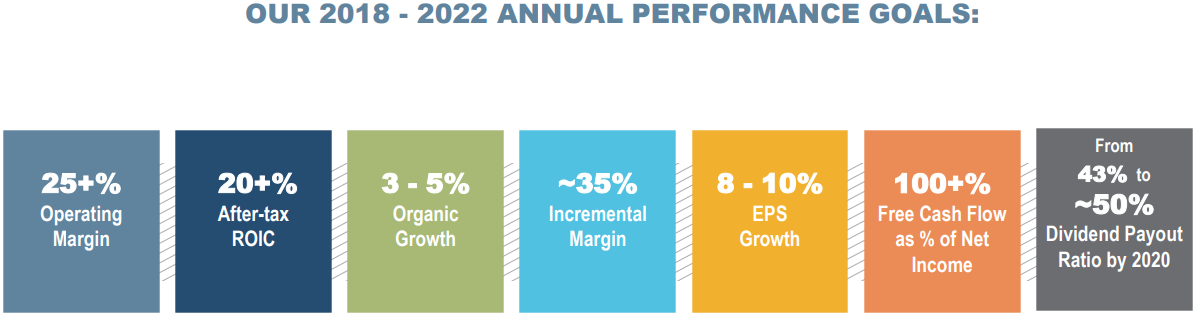

Going forward, management has three points of focus. First, the company wants to use about 25 to 30% of its operating cash flow to reinvest in organic growth. Second, ITW wants to continue increasing its dividend (35% to 40% of operating cash flow) and extend its industry leading payout growth streak. Finally, the firm plans to continue acquiring small businesses (30% to 40% of operating cash flow).

Rather than pursue large, needle-moving (and often overpriced and hard to manage) deals, Illinois Tool Works plans to buy one to three companies per year for between $100 million to $500 million each. Each purchase is intended to be very disciplined, targeting only firms with highly specialized products backed by strong patents. In other words, ITW is hunting for businesses which fit well into its existing 80/20, customer-back innovation, and decentralized management framework.

For example, in 2016 the company spent $450 million on German company ER&C, which makes automotive connectors and fasteners. The company had $500 million in sales in 2017 and 11% operating margins. However, thanks to ITW’s 80/20 and customer-back initiatives, management expects that subsidiary to grow sales 3% annually (to $575 million) and achieve 20% operating margins over time.

In addition, each bolt-on acquisition must be selling products in one of the company’s key segments and have better than industry average organic growth potential. This policy was implemented after management’s determination in 2012 that growth through acquisitions was an unsustainable and less profitable way to maximize earnings and cash flow.

Today, management expects ITW to achieve 3% to 5% annual organic growth with ongoing cost cutting measures sustaining 8% to 10% long-term earnings and free cash flow growth.

Note that due to management’s long-term 50% free cash flow dividend payout ratio target, the company’s dividend is likely to grow slightly faster than free cash flow per share over the next three years.

In 2018, management is expecting 17% growth in free cash flow per share, meaning that an 18% to 20% dividend hike is possible, in line with 2017’s increase. But over the long term, ITW expects to achieve 8% to 10% annual dividend growth.

Overall, Illinois Tool Works is a company that is built to last. The company’s disciplined management team and refocused operations certainly help, but its diverse product lines, end markets, and geographies are also major strengths.

When one industry is weak, another is usually strong, smoothing out earnings and providing consistent free cash flow for the company with which to reinvest in the highest-returning businesses. It’s hard to see a future in which ITW no longer becomes relevant – its hands are in too many pots, most products are protected by patents and sold in slow-changing markets, and its decentralized operating structure helps its numerous businesses run more efficiently.

Key Risks

Despite the company’s strengths, there are several risks to keep in mind.

Over the short term, ITW’s results can be affected by the health of the global economy, input cost inflation, and foreign currency exchange rate fluctuations (roughly half of sales are generated overseas). However, none of these issue should impact ITW’s long-term earnings power.

More significantly, there is risk that Illinois Tool Works may have overdone it on cost cutting, especially when it comes to R&D and capital investment. In 2017, the firm spent a total of 4.2% of revenue on designing and producing new products. However, per Morningstar, its largest rivals, Danaher (DHR), Honeywell (HON), and 3M (MMM), spend between 9% to 11% of sales on R&D and capital investment each year.

Cutting too close to the bone could cause ITW to miss its long-term financial targets. It’s also worth pointing out that the company’s renewed emphasis on organic growth and need to run a more consolidated operational structure (rather than letting its acquired businesses remain largely autonomous) is a deviation from the company’s prior successful growth strategy and could have knock-on effects down the road.

Fortunately, Illinois Tool Works has not built its impressive track record on short-sighted strategies to drive unsustainable margin expansion and bottom line growth. So it’s unlikely that management has knowingly underinvested in innovation and growth.

However, going forward it is possible that the company decides it needs to ramp up R&D and capex spending, which could result in slower than expected cash flow and dividend growth.

Closing Thoughts on Illinois Tool Works

Few companies can match Illinois Tool Works’ track record of delivering strong but sustainable dividend growth for more than 50 consecutive years. Despite the firm’s wide reach, management has carefully selected the markets in which the business competes, ensuring ITW earns a high return on its invested capital.

While the company has certainly evolved in a meaningful way in recent years, most notably consolidating its regional subsidiaries and moderating its focus on acquisitive growth, ITW’s disciplined and conservative operational principles remain. Investors can likely expect solid dividend growth from Illinois Tool Works for many years to come.

To learn more about ITW’s dividend safety and growth profile, please click here.

Leave A Comment