With roots tracing back to 1715 in London, GlaxoSmithKline (GSK) is one of the world’s largest pharmaceutical companies. The business has nearly 100,000 employees and operates in more than 150 countries.

GlaxoSmithKline has three primary business segments:

- Pharmaceuticals (57% of revenue, 66% of segment profits): patented drugs treating bacterial, viral (including HIV), as well as respiratory, cardiovascular, urogenital, metabolic, dermatological, and immuno-inflammatory conditions.

- Vaccines (17% of revenue, 18% of segment profits): produces and distributes 25 vaccines around the world (about 800 million doses annually) to prevent diseases such as Meningitis, Hepatitis A, Hepatitis B, Tetanus, HPV, Diphtheria, Influenza, Pertussis, Measles, Mumps, Rubella, Typhoid, Varicella (Chicken Pox), Rotavirus, and Pneumococcal Pneumonia.

- Consumer Healthcare (26% of revenue, 15% of segment profits): oral health, nutrition, and skin health products (in the form of tablets, creams, syrups, and skin patches) under the Otrivin, Panadol, parodontax, Poligrip, Sensodyne, Theraflu, and Voltaren brand names

As you can see, while GlaxoSmithKline is a highly diversified company. While the vast majority of its sales are generated by its patented pharmaceutical division, the company still maintains a strong presence in vaccines and consumer products, which generate less volatile cash flow due to their lack of patent expirations.

However, it should be noted that GlaxoSmithKline’s four largest drugs accounted for 26% of the company’s sales in 2017:

- Advair (asthma): 10.4% of sales

- Triumeq (HIV-1 infection): 8.1%

- Tivicay (HIV / AIDs): 4.6%

- Relvar (asthma): 3.3%

Advair lost U.S. and EU patent protection in 2010 and 2013, respectively, and has been facing steadily declining global sales for the last four years. Sales of the asthma treatment drug are expected to drop at least 20% in 2018.

The company’s sales are highly diversified by geography with the U.S., Europe, and International regions accounting for 37%, 26%, and 36% of 2017 revenue, respectively.

Business Analysis

The pharmaceutical business is an incredibly high-margin industry thanks to several key characteristics. First, drug development is an extremely highly regulated and expensive business, with new medications often taking 10 to 15 years to get approval, and total costs potentially exceeding $2 billion per new approved medication.

Patent protection (granted from initial filing) lasts for 20 years, which means that once a new drug is approved the company has a monopoly that allows it to enjoy extremely high margins (GSK reported a 34% operating margin in its pharmaceutical segment in 2017) and impressive free cash flow.

For example, rivals such as Johnson & Johnson (JNJ) and AbbVie (ABBV) enjoyed 23% and 33% free cash flow margins in 2017, respectively.

However, Glaxo’s free cash flow margin is only 11% due to its diversification into lower margin vaccines and consumer products (as well as its decision to charge less for drugs in emerging markets), both of which lack the fat margins of patent-protected drugs.

Still, management believes that increased diversification is the key to maintaining more stable growth over time, including for its R&D investments and the dividend, which has remained frozen since 2014.

This is largely why Glaxo made a $20 billion asset swap with Novartis (NVO) in 2015, which gave its rival cancer drugs in exchange for Novartis’s vaccine portfolio and a majority stake in a joint venture that combined those companies’ consumer health businesses.

In March of 2018, Glaxo announced it was buying out Novartis stake in that joint venture for $13 billion. Glaxo paid a seemingly reasonable multiple of 11.7 times operating earnings for this deal which is expected to boost the company’s revenue growth by about 3% for 2019.

The acquisition will give Glaxo 100% of the company’s sales from highly stable products such as: Sensodyne toothpaste, Panadol headache tablets, muscle gel Voltaren, and Nicotinell patches.

However, while Glaxo continues to focus on diversifying into more stable businesses, ultimately the majority of its earnings and cash flow growth still depends on the success of its patented drug portfolio.

In fact, management has said that its top priorities are:

- Developing its drug pipeline

- Expanding consumer medical products

- Rolling out new vaccines

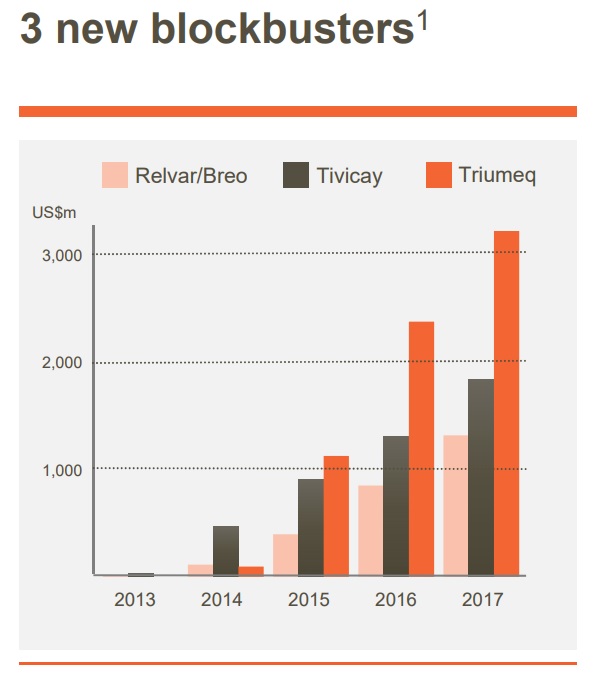

Fortunately, the company has found good replacements for its declining Advair medication. For example, combination asthma/COPD treatment Relvar/Breo and HIV drugs Tivicay and Triumeq have been seeing booming sales that totaled about $6.5 billion in 2017.

That’s more than enough to fully offset Advair’s approximately $4.2 billion in sales, a figure that is likely to continue to decline as generic competition for Glaxo’s top selling inhaler continues to hit the market.

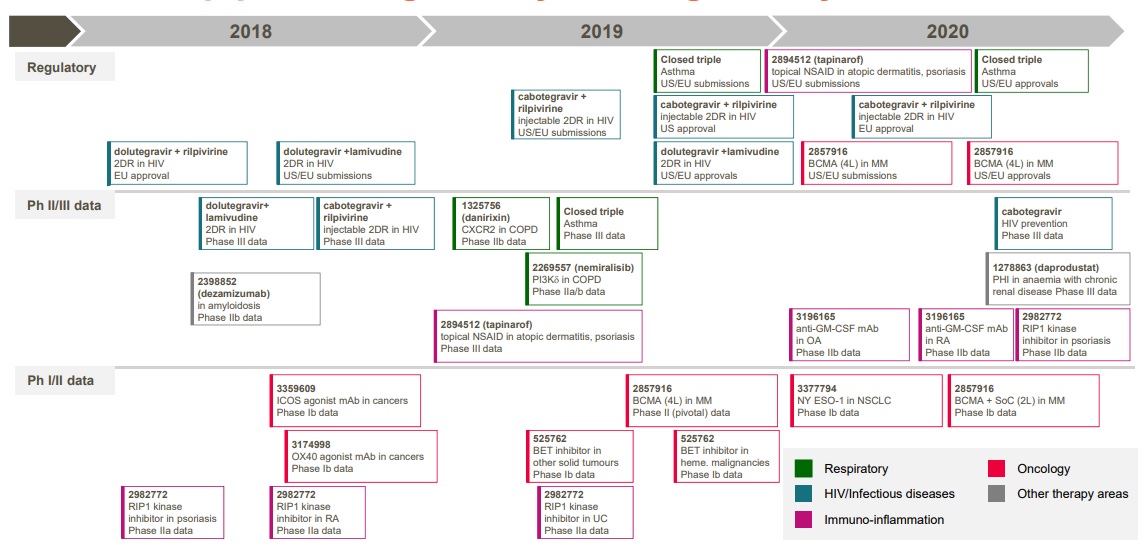

The company also has a strong drug development pipeline with 34 drugs and treatments in late stage development.

With that said, it should be noted that unlike many pharma companies, Glaxo’s pipeline is riskier. That’s because it’s not focused on expanding indications for already approved drugs but rather developing all new treatments. This increases the risk of a drug failing to ultimately receive approval.

The company also has a rather unique strategy for winning market share overseas, especially in emerging markets where healthcare consumers are not as wealthy. Specifically, Glaxo is capping its drug prices at just 25% of what it charges in developed nations (as long as manufacturing costs are covered). While this may result in stronger market share gains, it can also hurt the company’s overall profitability.

Glaxo is also investing 20% of emerging market profits into local healthcare markets in those countries by training local healthcare workers and improving public health. That’s a smart long-term strategy that can increase goodwill, help win local regulatory approval, and obtain bulk drug purchase contracts from national health systems.

In the vaccine segment, Glaxo is excited about the sales potential of shingles vaccine Shingrix. In the U.S. alone it’s estimated that there are 100 million adults that need shingles vaccines. About 60 million of those people have either not been immunized or are due for a booster. Shingrix could help Glaxo maintain its global lead on vaccines, which the company sold $7.2 billion of in 2017.

The vaccine has proven to have greater than 90% efficacy in trials thus far, and Shingrix has received approval in the U.S., Canada, the EU and Japan. The company is rolling it out in 2018 and hopes to win market share quickly.

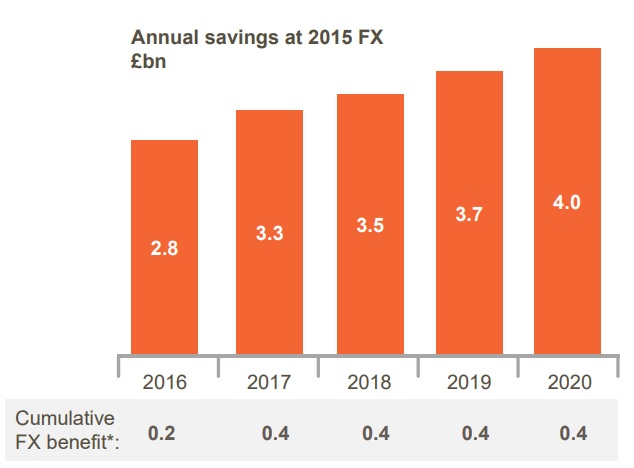

The other side of profit growth is Glaxo’s strong focus on maximizing efficiencies of scale by streamlining its manufacturing and distribution channels. Glaxo announced a major restructuring effort in 2015 that it hopes to result in 4 billion pounds in annual cost savings by 2020. The majority of this restructuring is now complete and management says it’s on track to achieve its cost cutting targets.

All told, Glaxo expects that its combination of new drug launches, vaccine rollouts, and cost cutting should allow it to grow revenue at mid to high single-digit pace through 2020 and achieve mid to high single-digit EPS growth.

If management hits those targets, then it would mean that Glaxo is just a few years away from decreasing its free cash flow payout ratio below the 75% or so that management has said is the trigger for future dividend growth.

In other words, Glaxo is potentially poised to become a far more attractive high-yield income stock in the coming years. However, investors need to realize that the company faces numerous challenges that could derail its growth efforts.

Key Risks

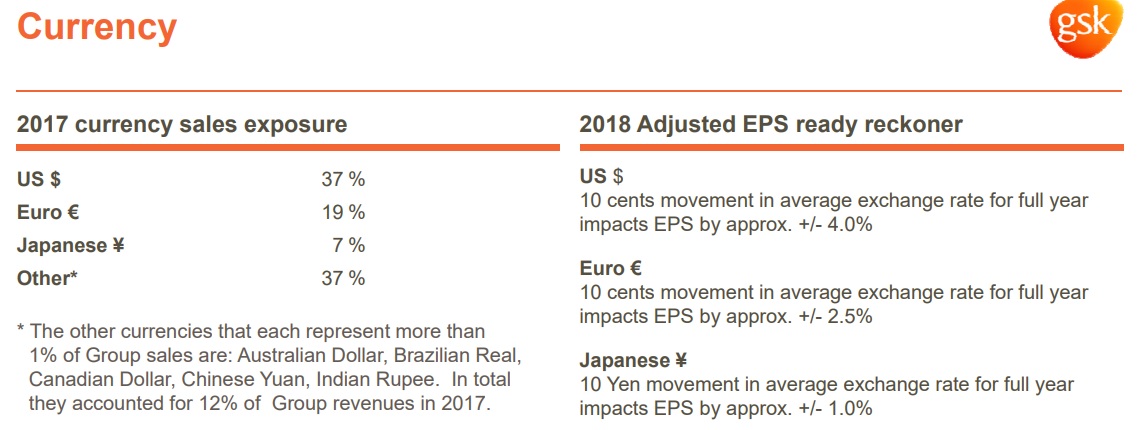

First, income investors should note that while there is no UK dividend withholding tax, as a UK-based company, Glax exposes U.S. investors to significant currency risk. While Glaxo’s dividend has been very stable over time (it’s never been cut in over 20 years), the effective amount of dividends American shareholders receive can be highly variable.

This currency risk is also seen in the company’s profits, due to its highly global business. For example, in 2017 Glaxo enjoyed a 5% boost to adjusted EPS thanks to favorable swings in global currencies.

However, management has warned that in 2018 the company might face a reversal of these trends that could negatively impact adjusted EPS growth by as much as 6%. Fortunately, currency risk is unlikely to affect Glaxo’s long-term earnings power.

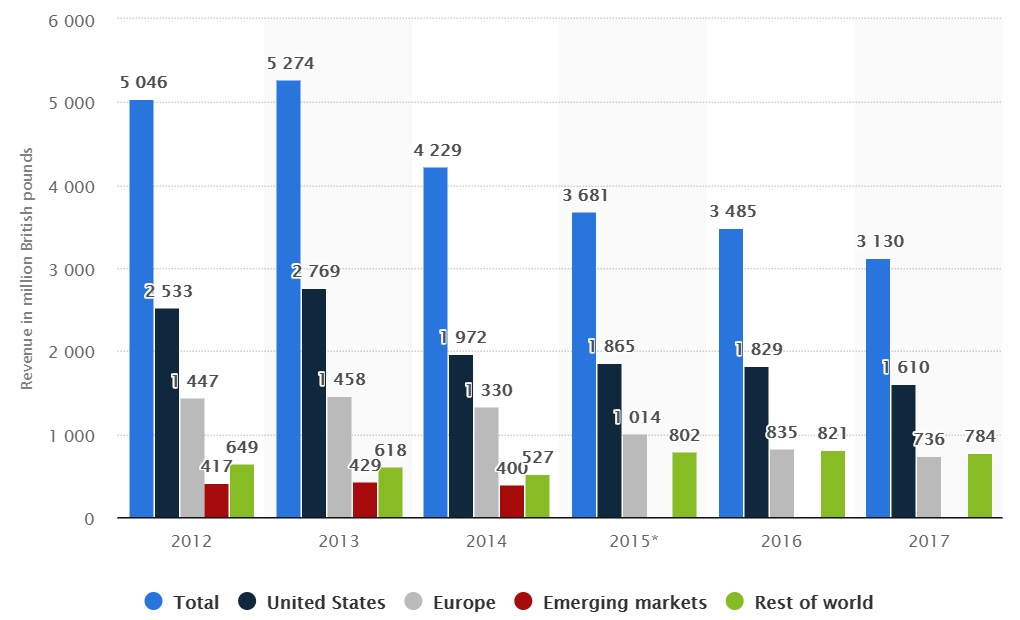

Next, be aware that like all pharmaceutical companies, Glaxo faces steep drop offs in sales and earnings when its patented pharmaceuticals lose patent protection. Advair, Glaxo’s largest drug accounting for around 10% of company-wide sales, lost protection in 2010 in the U.S. and 2013 in the EU. Up until now, generic competition has been slow to develop in a meaningful way, but that could be changing.

Mylan (MYL) and Novartis (NVS) are racing to bring generic versions of the inhaled medication to market, and management says that even if no competitor arrives, Advair sales in 2018 are expected to decline by 20% to 25%. That continues a trend of steadily falling sales for Glaxo’s most important drug.

Global Advair Sales Over Time

Fortunately, Glaxo thinks that other drugs will be able to pick up the slack and drive adjusted EPS growth (on a constant currency basis) of 4% to 7% for the year.

However, in the event that a generic rival does hit the market, then the pharmaceutical segment’s adjusted EPS would only expect 0% to 3% growth. This highlights the kind of large uncertainty that surrounds the sales and earnings growth of all drug companies when key products lose patent protection.

This is a key reason why Glaxo has been so aggressive in diversifying into more stable businesses such as consumer healthcare. Before deciding to buy out Novartis stake in its joint venture, Glaxo was considering buying Pfizer’s (PFE) consumer products business for up to $20 billion, which could have potentially jeopardized the firm’s dividend. This brings up another risk to consider, the heavy M&A nature of the pharmaceutical business.

Since drug development is so expensive, time-consuming and uncertain (only one in 10,000 potential new compounds/treatments make it to market), drug companies often have to buy their way to growth. As a result, pharma companies often make big acquisitions to acquire a rival’s drug development pipeline and existing cash flow streams.

However, all large acquisitions come with risk. For one thing, a company might overpay for a rival, stretching the balance sheet to a point where the dividend may be pressured. Achieving synergistic cost savings becomes essential in those cases, since whether or not a deal ultimately proves accretive to EPS and free cash flow per share can depend on the successful merging and streamlining of two drug maker’s supply chains, manufacturing capabilities, and R&D units.

But all corporate cultures are slightly different, and synergistic cost savings can end up falling sort of expectations. In addition, even the most promising drug candidates that a pharma company may buy could end up failing during clinical trials.

For example, rival AbbVie paid $9.8 billion for Stemcentrx in 2016. That deal was made primarily to acquire its promising Rova-T cancer drug which was expected to be capable of generating up to $5 billion in annual sales by 2025.

However, recent disappointing drug trials have caused AbbVie to pull early approval filing in the EU. And now there is concern that Rova-T might prove to be a loss for AbbVie that could cost shareholders billions. Glaxo faces the same regulatory approval threats with its own drug development pipeline.

In addition, we can’t forget about political and regulatory risk. For example, the high cost and rich margins enjoyed by patented drugs often attracts the ire of politicians looking for a quick and easy way to lower ballooning healthcare costs.

“One of my greatest priorities is to reduce the price of prescription drugs. In many other countries, these drugs cost far less than what we pay in the United States. That is why I have directed my Administration to make fixing the injustice of high drug prices one of our top priorities. Prices will come down.” – President Donald Trump

The president has also said in the past that drug makers were “getting away with murder”, which is a sentiment that is shared by many people and populist politicians around the globe.

Even if outright price controls are not put in place, don’t forget that in many countries, a substantial amount of healthcare funding is either directly controlled or heavily subsidized by national governments. In other words, outside the U.S. drug makers like Glaxo usually face far lower margins because national healthcare systems negotiate bulk purchases at substantially reduced rates.

In the U.S., Medicare/Medicaid, which cover about 50% of Americans, have yet to do this. In fact, current US law forbids bulk price purchases. However, that law could potentially be changed since it represents a relatively less controversial way to lower soaring medical costs.

And with an aging population that is expected to drive healthcare spending higher by $2 trillion per year by 2025 in the U.S. alone, many expect that drug maker margins will come under increasing pressure in the future. In fact, Johnson & Johnson has said that it is facing exactly this kind of pressure and is seeking to grow pharmaceutical profits not from higher drug prices but greater sales volumes.

Even private payers, such as insurance companies, HMOs, and Pharmacy Benefit Managers (PBMs) are increasingly desperate to find ways to lower rising costs. This is why an ever-larger wave of consolidation in the medical industry is happening, including CVS Healthcare (CVS) announcing the $69 billion acquisition of health insurer Aetna (AET).

Rumors are also circulating that Walmart (WMT) or Walgreens Boots Alliance (WBA) may be looking to acquire insurer Humana (HUM), for up to $40 billion. Increased consolidation in the medical space means that drug makers’ largest customers are likely to get increasing pricing power in the future.

Meanwhile, Berkshire Hathaway (BRK.B), JPMorgan Chase (JPM), and Amazon (AMZN) have announced they are partnering on a new non-profit company to provide lower cost medical care to their companies’ employees.

The point is that while the world’s aging and growing population means that there is a lot of potential growth opportunity for drug makers and medical companies, the healthcare industry is also going through one of the largest periods of rapid change and disruption in its history.

When you combine that with the inherent boom and bust cycle of pharmaceutical company earnings created by patent expiration cliffs, massive competition from rival products that target the same conditions, and incredibly high R&D costs, you get one of the most complex and difficult industries for dividend investors to understand.

And given that management has said that it doesn’t plan to increase the dividend until the Galxo’s free cash flow payout ratio declines to about 75% (from 82% in 2017), it’s likely that the company’s dividend will remain frozen for at least a couple of years as management’s priorities are elsewhere right now.

Conservative income investors may be better off sticking with only the most time-tested and diversified blue chips in this industry, such as highly diversified dividend king Johnson & Johnson.

Closing Thoughts on Glaxosmithkline

GlaxoSmithKline is one of the largest and most diversified drug makers in the world. The company has a long history of successfully navigating one of the world’s most rapidly changing and difficult industries, and rewarding investors with highly stable dividends along the way.

That being said, the business faces a number of potential threats to its plans to grow its sales, cash flow, and dividends. While Glaxo’s generous payout is likely to be safe and stable over time, the many challenges inherent to the pharma industry mean that the company is unlikely to deliver the steady dividend growth that many income investors are looking for.

With substandard profitability, slower growth prospects, and an inferior dividend track record to peers such as Johnson & Johnson, investors may be better suited looking elsewhere for exposure to this complex but highly defensive industry.

To learn more about Glaxo’s dividend safety and growth profile, please click here.

{kind=link}

Leave A Comment