Dominion Energy surprised many investors when it announced plans to acquire SCANA (SCG) in a $14.6 billion all-stock deal on January 3. SCANA’s stock rallied more than 20% on the news, but Dominion’s stock declined around 4%. The deal is expected to close during the third quarter of 2018.

SCANA ran into trouble in 2017 when regulators decided to consider suspending over $440 million per year in rates that the company charges customers for its failed nuclear reactor units.

SCANA and its partner Santee Cooper spent the past decade building these reactors for roughly $10 billion, but the project isn’t even half-finished today. Worse, $9-16 billion was estimated to be needed to finish the work. As a result, the companies decided to pull the plug on the project.

SCANA was being investigated for its handling of construction of the reactors, and regulators were looking at suspending a rate hike that was previously approved to help SCANA collect billions of dollars it already spent on this unfinished work (the company continued taking payments).

If that outcome were to occur, not only would SCANA’s high dividend almost certainly be eliminated, but bankruptcy wouldn’t be out of the question. In other words, SCANA was clearly facing major uncertainties.

Simply put, SCANA found itself in a position of severe distress. The company’s stock price tumbled nearly 50% until Dominion stepped in with a bid, looking to capitalize on a unique opportunity. The question many investors have now is what they should do with Dominion.

Large acquisitions come with large risks. More often than not, the acquiring company ends up overpaying and overestimating the benefits from a major acquisition while underappreciating the integration challenges that wait.

In this case, Dominion’s management deserves the benefit of the doubt given the uniqueness of the situation, SCANA’s distressed valuation, and the transaction’s contingency on regulatory approval for Dominion’s proposed nuclear solution. SCANA simply doesn’t have other options, and Dominion’s proposal may very well be the best option for regulators, allowing Dominion to gain attractive regulated assets at a great price. Dominion is also very familiar with South Carolina since it already has a pipeline business and some solar farms in the state, as well as a strong presence in the southeast region of the U.S.

Dominion has offered to pay SCANA’s customers $1.3 billion (about $1,000 per customer) and reduce their monthly bills by 5% (valued at nearly $600 million) to help make up for customers who have been overcharged for a number of years to fund SCANA’s failed nuclear project. The company will also absorb about $1.7 billion in costs from the uncompleted plant that weren’t in SCANA’s utility rates yet.

Added all up, Dominion is paying around $7.43 billion excluding debt for a company that would have cost it $14 billion last summer with a similar deal premium, according to The Wall Street Journal.

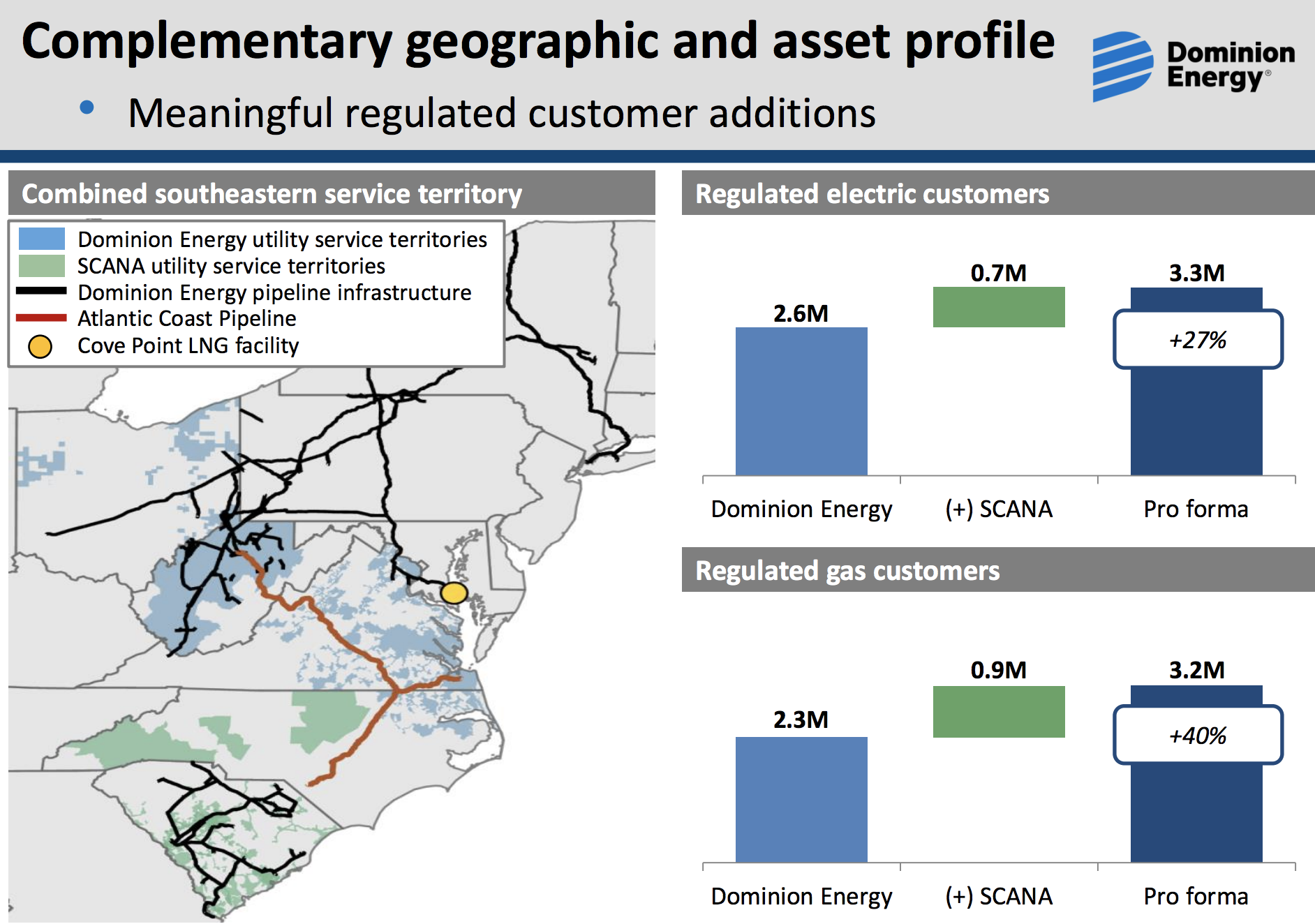

If regulators sign off on Dominion’s proposal, it would lift away significant uncertainty and add an attractive core utility franchise to the company’s regulated footprint. Specifically, Dominion’s base of regulated electric and gas customers would grow by 27% and 40%, respectively.

Despite the company’s high payouts and its assumption of SCANA’s $6.7 billion of debt, Dominion expects the deal to be immediately accretive (i.e. it will boost earnings per share) once it closes in the third quarter of 2018. Management believes Dominion’s 2017-2020 EPS compound annual growth rate will also rise to at least 8% from a previous range of 6% to 8%, and the outlook for 10% annual dividend growth through 2020 remain intact.

Overall, it’s hard not to like the increased scale, diversification, and regulated utility operations that Dominion will enjoy. Investors can also find some comfort given that the transaction is contingent upon regulatory approval for Dominion’s nuclear solution, reducing some of the risk that SCANA faces, and that management remains committed to deleveraging.

However, it’s fair to have some reservations about the unknown liabilities Dominion could be inheriting related to SCANA’s partially-completed nuclear plant, depending on what type of cleanup and restoration work the government might require in the future. It will take years before the outcome of this merger can be judged, but for now, holding Dominion as part of a well-diversified income portfolio seems reasonable.

Business Overview

Dominion and its predecessors have delivered energy since 1898. Today the company is one of America’s largest diversified utilities, with a portfolio of more than 26,000 megawatts of electric generation, 66,000 miles of natural gas transmission, gathering, storage, and distribution pipeline, and over 64,000 miles of electric transmission and distribution lines. Simply put, the business makes money by producing and transporting energy.

After acquiring Questar, a major natural gas distributor, for $5.9 billion in late 2016, the combined company serves more than 6 million utility and retail energy accounts. Should Dominion’s acquisition of SCANA prove successful, the company’s base of regulated gas and electric customers would increase from 4.9 million to 6.5 million.

Dominion Energy operates via three business units:

Dominion Generation (54% of profits): Owns all of the company’s power generating facilities, which serve its own electric utilities in Virginia and North Carolina to provide cleaner, cheaper electricity. This segment also contains Dominion’s small merchant power division and renewable energy fleet, which product and sell electricity to other utilities under long-term power purchase agreements (PPAs).

Dominion Virginia Power (18% of profits): Operates regulated electric transmission and distribution franchises in Virginia and North Carolina, providing power to about 2.6 million customer accounts.

Dominion Energy (28% of profits): Operates one of the largest natural gas storage systems in the country (over 1 trillion cubic feet of capacity) and 15,000 miles of natural gas transmission, gathering, and storage pipelines that distribute natural gas to 2.3 million customer accounts in Ohio, West Virginia, Utah, Wyoming, and Idaho.

This segment also acts as the general partner and sponsor of Dominion’s midstream MLP, Dominion Midstream Partners (DM), which provides a tax efficient, low cost funding method for the company’s ambitious natural gas growth plans. That includes such mega-projects as the Cove Point LNG export terminal and Atlantic Coast Pipeline.

While the majority of the company’s revenue and earnings are derived from Dominion Generation, don’t let that scare you into thinking that the company’s revenue and earnings aren’t derived from secure sources.

In fact, over 90% of Dominion’s overall sales are from its regulated operations, with the rest mostly coming from long-term power purchase agreements. In other words, Dominion’s revenue, earnings, and cash flow are still quite stable. Note that SCANA would further increase Dominion’s mix of regulatory business.

Business Analysis

For over 120 years, Dominion has been reliably and affordably generated and delivered energy for its customers. More impressively, the company has paid uninterrupted dividends for close to 90 years.Dominion’s durability has been driven by management’s disciplined and conservative approach to investing capital, which has resulted in almost all of the company’s business being driven by predictable regulated activities.

Regulated utility companies are essentially government regulated monopolies. Building and maintaining power plants, transmission lines, and distribution networks typically costs billions of dollars to cover a particular region. Since the number of customers in a service territory is only so big and typically grows very slowly, it is usually uneconomical to have more than one utility supplier.

Competition is further limited by state utility commissions, which have varying degrees of power over the companies allowed to construct generating facilities. Despite the monopoly status of most regulated utilities, their profit potential is limited because state commissions control the price they can charge for their services.

This is done to keep prices reasonable for consumers while providing utility companies with enough of an incentive to earn a reasonable return on their investments made to provide safe and reliable service.

As a result, it’s very important to analyze the geographic regions that a utility company operates in. Some states have more favorable demographics and regulatory bodies.

Fortunately, Dominion Virginia Power benefits from a friendly regulatory environment in its core Virginia and North Carolina electric markets. That’s thanks in large part to the relatively fast population and business growth rates in these states, which causes regulators to want to incentivize expanded infrastructure spending through higher-than-average allowed returns on capital, as well as increasing electric rates over time.

Besides operating in generally attractive regions characterized by constructive regulatory relationships, Dominion has made significant efforts in recent years to branch out into faster-growing businesses, particularly the highly profitable natural gas distribution business.

For example, take Dominion’s 2016 acquisition of Questar, a Rockies-based integrated natural gas distribution company. Questar’s utility residential rates run about 20% below the U.S. average, demonstrating its efficient operations, and the combination significantly expanded Dominion’s presence out west.

Essentially, the deal gave Dominion better balance between its electric and gas operations while also improving the company’s scale and diversification by geography and regulatory jurisdiction.

Dominion’s strategic investments have made it one of the cleanest energy companies in the country. Solar accounts for more than 5% of its total generating capacity, and environmentally-friendly, cost-effect gas-fired plants are a large component of Dominion’s power strategy. As a result, the company’s low carbon emissions rate is in the top quartile among energy producers in the U.S.

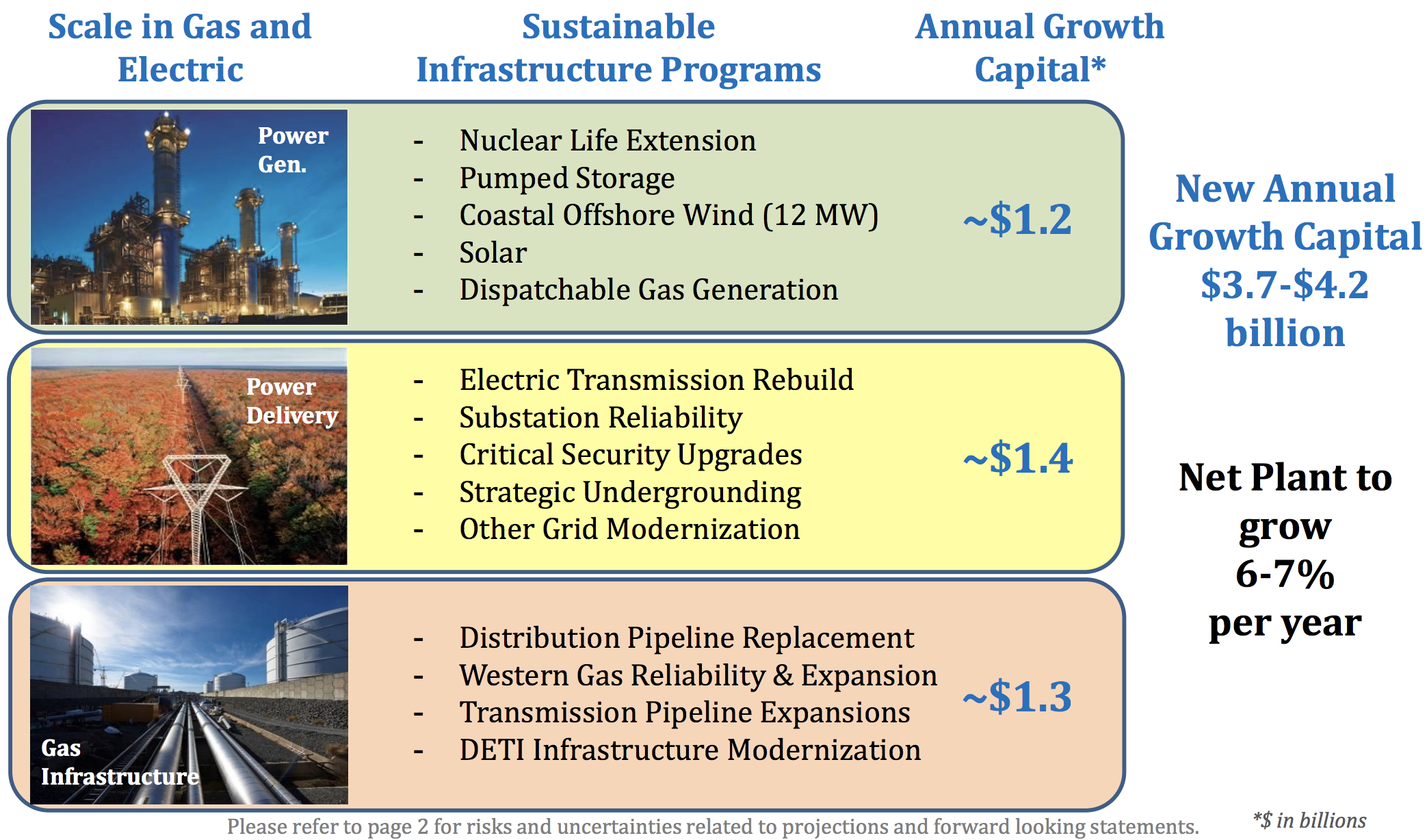

Management has big plans for the future as well, including some of the most ambitious projects in the industry, with as much as $20 billion in growth capital spending planned through 2020 (about $4 billion annually).

Most of the company’s investments are going into the natural gas side of the business, which is expected to enjoy several long-term tailwinds thanks to structurally lower U.S. natural gas prices that have resulted from fracking significantly lowering domestic production costs.

As a result of cheap natural gas, utilities are increasingly shifting to cleaner-burning, more efficient fuels to reduce emissions, international demand for U.S. natural gas is growing, and more pipelines are needed to transport natural gas to utilities across the country. Dominion is playing in all of these areas.

The company recently completed a $4 billion project to add gas liquefaction capabilities at its Cove Point terminal in Maryland. Customers in Japan and India can now load liquified natural gas (LNG) onto tankers for shipment to supply their energy needs. Dominion’s liquefaction capacity is full subscribed for offtakers under 20-year contracts and went into service in late 2017, providing another stream of predictable cash flow for many years to come.

Dominion also kicked off a $1.3 billion project in June 2016 to construct a gas-fired plant in Virginia. Its Greensville County Power Station is expected to be in-service December 2018. The project is over 60% complete today and remains on time and on budget.

Finally, construction began on the 600-mile Atlantic Coast Pipeline in late 2017. This pipeline will transport low-cost natural gas supply to utilities in Virginia and North Carolina, enhancing the reliability of utilities service, reducing costs for customers, and lowering emissions. Dominion has a 48% stake in this $5+ billion project, which is expected to be completed in the second half of 2019.

Significant investment is clearly going into the natural gas side of the business, which is where Dominion’s midstream MLP comes in.

Dominion Energy is the general partner and sponsor of Dominion Midstream Partners, which means that, in addition to owning over 60% of its limited units, it also owns the highly lucrative incentive distribution rights, or IDRs. These rights grant it a growing share of the MLP’s marginal distributable cash flow (the MLP equivalent of free cash flow) as its distributions increase over time.

Importantly, Dominion is able to sell or “dropdown” its midstream assets to Dominion Midstream Partners, which raises funds from external debt and equity markets. This allows Dominion to recoup the costs of constructing these valuable, long-lived, and cash flow-rich assets.

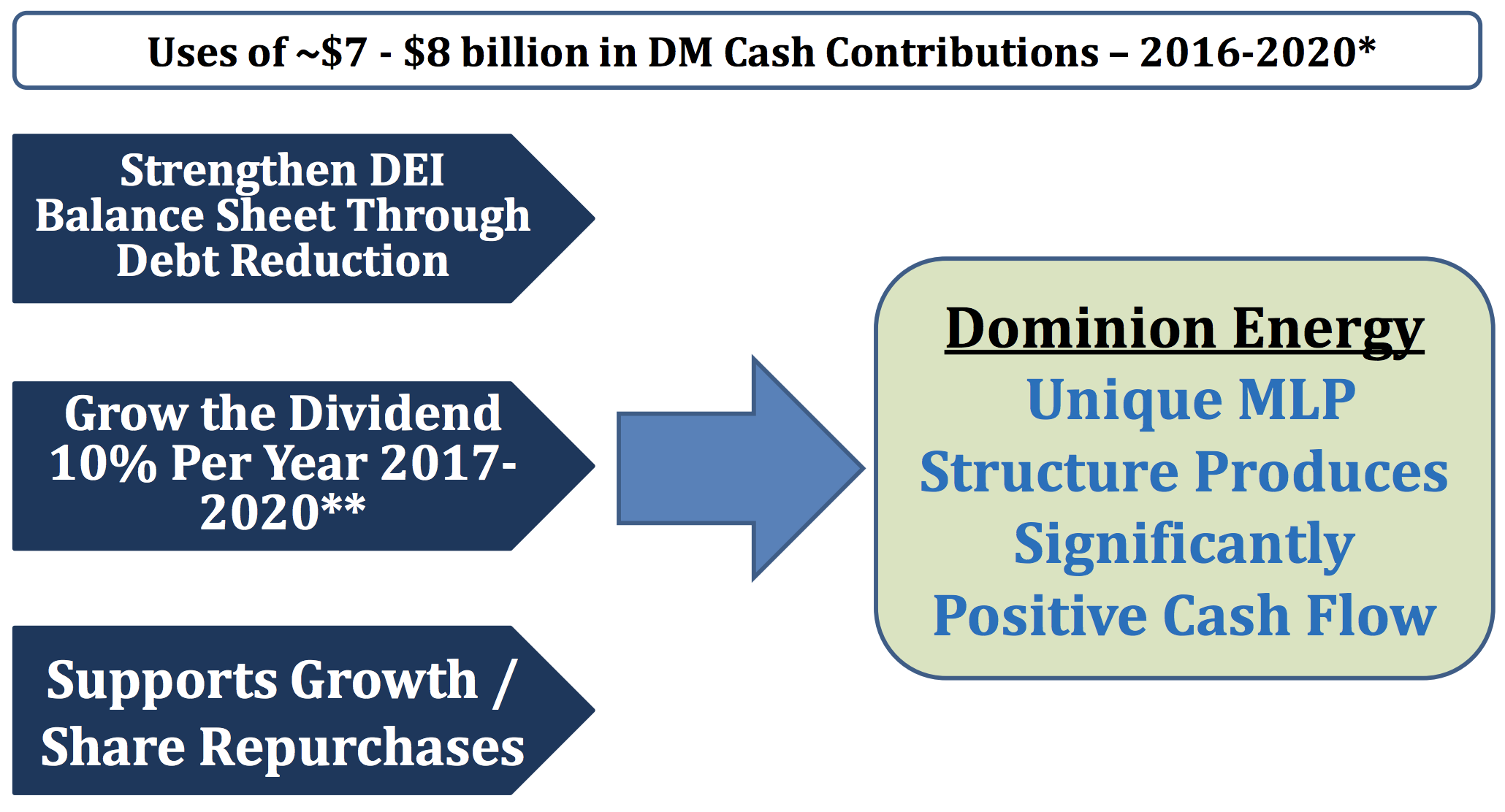

Since Dominion retains a massive stake in Dominion Midstream, the vast majority of the cash flows generated from these assets end up right back in its coffers, able to fund further growth initiatives and pay down debt.

Between $7 and $8 billion in cash is expected to flow from Dominion Midstream to go to Dominion Energy through 2020, which will help with management’s plans to strengthen the balance sheet, increase dividends at a strong pace, and buy back shares. Thanks to these dropdowns and the increased ability to reduce debt they provide, Dominion enjoys a strong investment grade credit rating with a stable outlook from S&P and Moody’s.

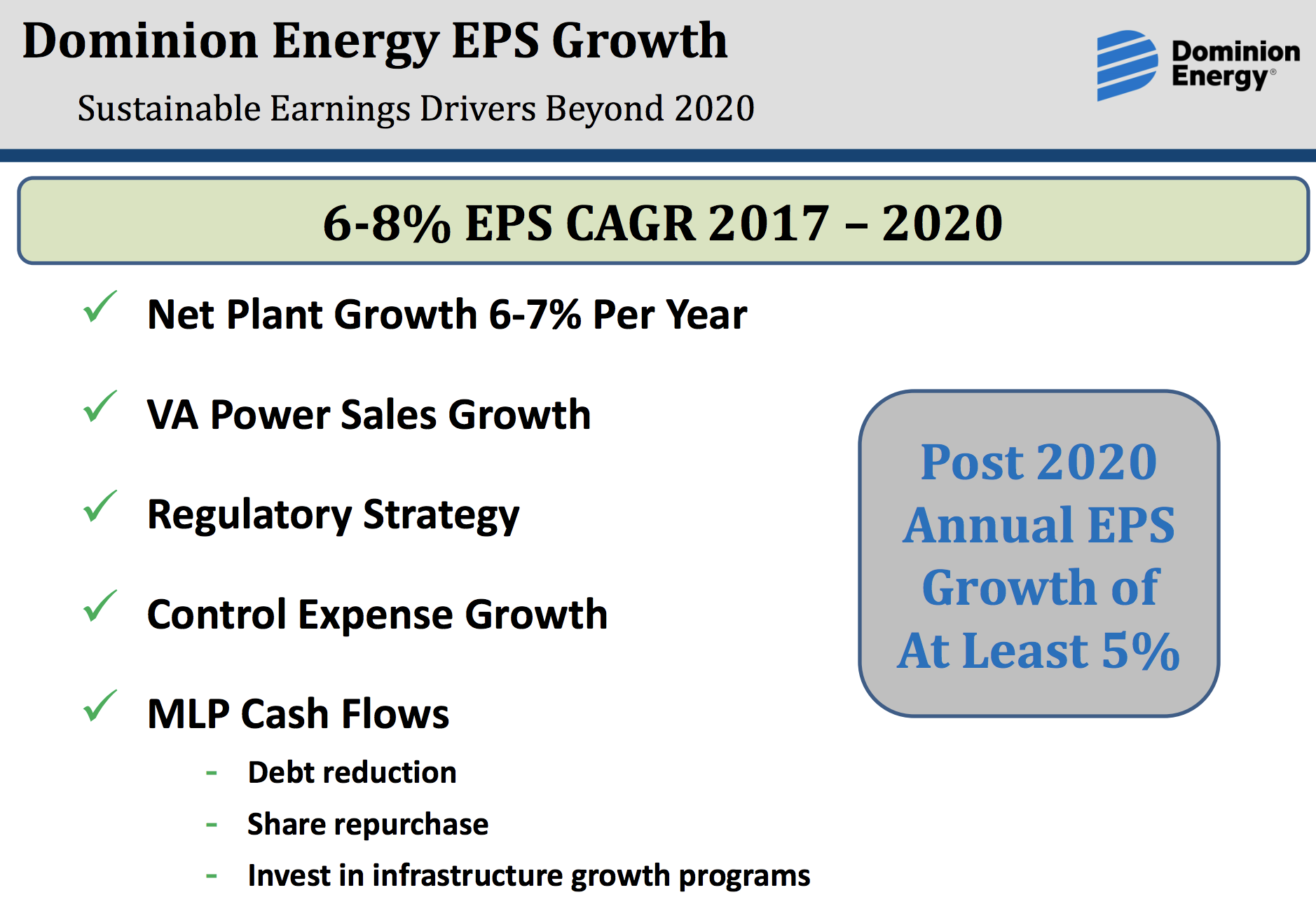

All told, Dominion Energy expects that its major investments will be able to generate operating earnings growth of at 6% to 8% per year through 2020. Assuming the SCANA deal closes in the second half of 2018, annual earnings growth is expected to increase to at least 8%. The company’s dividend is also projected to compound 10% annually through 2020, with management targeting a safe regulated payout ratio at up to 75%.

Overall, Dominion’s strong base of regulated assets, disciplined management team, industry-leading profitability, attractive portfolio of growth projects, lengthy history of paying dependable dividends, and exposure to favorable secular themes (cleaner energy, low-cost gas, renewables) make it one of the more appealing utilities in the sector.

Key Risks

There are several risks to be aware of with Dominion Energy.

First, while the company’s cash flow is highly stable, changes in the weather and power prices can affect short-term results. Milder weather can reduce demand for electricity and gas services, for example, and Dominion’s merchant power business can face challenging market conditions from time to time.

None of these issues seem like risks to Dominion’s long-term earnings power, and fortunately, the growth initiatives coming online over the coming years should result in solid earnings growth.

More importantly, Dominion is betting big on U.S. natural gas prices remaining low with its planned growth projects. Fortunately, this seems likely to remain the case thanks to advances in fracking technology, which have boosted domestic gas production. However, if prices fall too low, third-party producers could curtail production of their natural gas that Dominion depends on gathering, processing, and transporting.

Like every other utility, Dominion also faces execution and regulatory risks from its major growth projects. The company has proven to be a quality operator over the years, and all of its projects remain on track for now. Dominion also has strong relationships with regulators, although developments with SCANA need to be watched.

A final risk worth mentioning is related to Dominion’s dependence on capital markets. Specifically, because Dominion occasionally uses its shares to pay for acquisitions (as well as fund some of its growth projects), the company’s growth is somewhat at the mercy of its share price.

Meanwhile, its largest source of funding, Dominion Midstream, is far more exposed to this risk because its high-payout business model requires it to continually raise equity capital from investors.

In other words, in the event of really weak share prices, Dominion could find itself with insufficient liquidity to fund its aggressive growth plans. This could be especially true in a rising interest rate environment, which raises the cost of debt and makes utility shares relatively less attractive to income investors (potentially reducing the amount of cheap equity capital Dominion has access to). The company’s liquidity position looks solid today, and its investment grade credit rating also helps.

Closing Thoughts on Dominion Energy

Few regulated utilities offer a generous yield and strong dividend growth prospects, but Dominion appears to be one of them. As the company’s projects continue coming online over the years ahead, Dominion should enjoy some of the strongest long-term growth in the sector while continuing to possess many of the defensive qualities that make utilities a popular component of retirement portfolios.

With that said, investors need to keep a close eye on developments with SCANA. While this opportunistic purchase holds promising potential, SCANA is in a very messy position with its partially-completed nuclear project, which could create future troubles for Dominion. When combined with Dominion’s elevated leverage and major growth projects, management’s ability to execute is more important than ever over the coming years.

To learn more about Dominion’s dividend safety and growth profile, please click here.

Leave A Comment