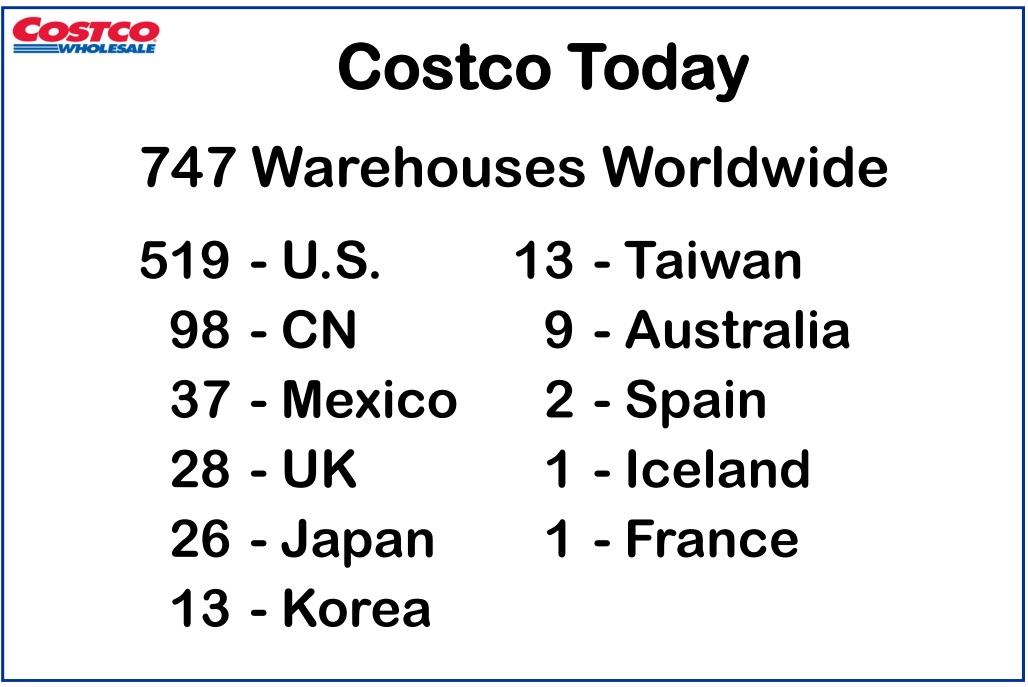

Costco (COST) was founded in 1976 and pioneered the wholesale warehouse retail business model. The company is one of the world’s largest sellers of groceries, alcohol, diamonds, electronics, prescription drugs, tires, gasoline, and even travel services. Costco operates nearly 750 store locations in 11 countries today.

While Costco is the world’s second largest retailer by sales (behind only Walmart), the firm generates the majority of its profits from its annual $60 and $110 executive membership fees which make up about 2% of total revenue but account for about 70% of income. The company has built up a base of 92.2 million cardholders around the world representing 50.4 million households.

The company is working hard to expand overseas, but the vast majority of sales and operating profits continue to come from its core U.S. operations where it conducts over 2.6 million sales transactions per day.

- US: 72% of revenue and 59% of operating income

- Canada: 14% of revenue and 20% of operating income

- Other International: 14% of revenue and 20% of operating income

Business Analysis

The retail industry is notorious for being an incredibly competitive space with razor-thin margins and very low customer loyalty. However, Costco has built an enduring business using a rather unique approach.

Simply put, the company’s membership model, use of co-branded credit cards (with Visa offering 2% to 5% cash back on various item categories), and quality assortment of on-trend merchandise have created an extremely loyal customer base.

For example, Costco’s membership renewal rate averages about 90% in the U.S. and 87% worldwide. Membership fee revenue has steadily grown at about 5% per year recently, driven by a steady rise in new members as well as a recent hike in membership fees (10% in mid-2017). This shows the pricing power that Costco enjoys, because even higher membership fees are not causing a decrease in new customers joining or a decline in retention rates.

Paying an annual fee also encourages customers to spend more at Costco so they feel they are getting the most possible value out of their membership. For Costco, membership fees provide a highly recurring source of high-margin revenue that allows the company to offer its customers near wholesale prices on numerous popular brands.

In fact, a Costco vendor we spoke with said that the company’s policy is to limit the markup on almost all of its products to just 15%, passing on almost all of the value to its customers (remember that membership fees generate 70% of Costco’s profits).

In addition to some of the popular brands listed below, approximately 28% of Costco’s fiscal 2017 sales were made under its private label Kirkland Signature brand. Costco makes higher margins on private label sales and has continuously improved Kirkland’s quality and reach, most recently expanding its offerings in apparel, sporting goods, fresh food and organic food items (Costco is one of the largest organic food retailers in the world).

Costco is also famous for its friendly customer service which is largely due to its forward-thinking approach to workers. Specifically, Costco takes a very long-term view and wants to minimize employee turnover, creating a company at which workers can find not only good jobs, but lifelong careers (the vast majority of hirings and promotions are made internally).

That’s one reason why in 2016 the company raised its minimum wage to $13.50 per hour. However, most employees are making an average of $22.50 within four years, and 90% of them receive healthcare and pension benefits as well.

While some analysts on Wall Street may be critical of Costco’s generous worker compensation, the company’s approach is actually another competitive advantage. According to MIT Sloan School of Management Professor Zeynep Ton, longer tenured workers who are happier, feel more appreciated, and are less worried about making ends meet make for a far better customer experience.

And the results ultimately speak for themselves. Costco’s average sales per square foot is about $1,200 compared to approximately $680 and $400 at Sam’s Club and Walmart, respectively. In fact, Costco’s sales per square foot measure is usually about two to three times that of its major rivals. The company’s annual turnover on products is also 50% to 100% greater.

Costco also makes up for its higher labor costs by focusing on having incredibly efficient supply chains and logistics. For one thing, the average Costco stocks just 3,700 items compared to 60,000 at some of its rivals.

And thanks to its enormous economies of scale and ability to source products from all over the world (produce is purchased from 44 countries), the company has been able to steadily improve its margins and profitability. That’s during a time when rivals like Kroger are slashing prices and seeing their margins decline significantly.

Costco has also been very successful at adapting to e-commerce, an area which has disrupted many of its rivals. Success in e-commerce has been driven by improved search checkout and return optimization, largely a result of analyzing the data about its members and what they buy. That’s driving improved website traffic and conversion rates. In the most recent six-month period, Costco’s e-commerce sales were up 27% excluding seasonal jumps in holiday shopping and currency effects.

The company has been focusing on integrating its existing stores into its supply chain, allowing customers to pick up items the same day that they are purchased online. Only about 40% of its U.S. warehouses are currently tied into this online platform, indicating that continued strong e-commerce growth is likely as the company continues to expand its online sales channels.

However, the biggest driver of Costco’s online success is arguably grocery delivery, which the company now offers on a same-day basis to its members from over 400 U.S. stores. By the end of 2018, same-day grocery delivery is expected to be implemented at all of its U.S. locations.

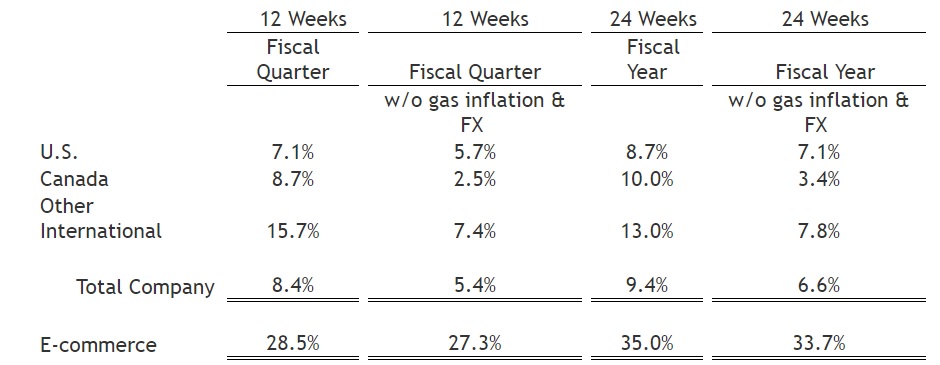

The success in e-commerce has helped fuel some of the industry’s best same-store sales, or comps, growth. Comps measure the increase in sales from stores open at least a year.

During the holiday season, for example, Costco’s core U.S. business, excluding volatile fuel sales, was up 5.7% compared to Walmart and Target’s (TGT) 2.6% and 3.6% comps, respectively. And looking out at the last six months, you can see that the company’s worldwide comps were even better, about two to three times greater than its major peers.

Costco Same-Store Comparable Sales

That impressive growth trend is not a fluke either, with the company’s most recent sales figures indicating accelerating comps, driven largely by the company’s excellent execution on e-commerce and faster growth in non-North American stores. International growth was strongest in Mexico, Japan and the UK.

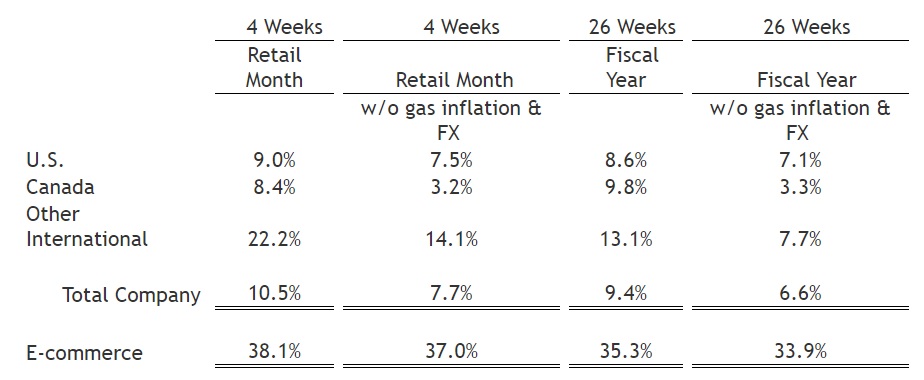

Costco Same Store Comparable Sales (March 2018)

Note that in March 2018, Costco’s online sales grew nearly 40%, which is about double the rate of growth that Amazon (AMZN) reported in its most recent quarter. This indicates that Costco is expanding its market share in online sales, providing evidence that management’s e-commerce strategy is working.

The end result is that Costco has managed to generate some of the industry’s best revenue growth while expanding its earnings at an even faster clip in recent quarters. This is a testament to Costco’s ability to continue improving its margins via greater economies of scale, despite strong pricing competition in the industry and greater e-commerce sales. (Due to shipping costs most retailers find online sales less profitable, but so far that doesn’t appear to be the case for Costco.)

Looking further out, there are three components to Costco’s long-term growth potential. First, the company needs to maintain its strong merchandise assortment and customer service in order to continue generating high retention rates while periodically raising membership prices. Thus far the company has proven very successful in this regard.

The second component is continued execution on e-commerce which can drive very strong same-store comps growth. Finally, growth will come from ongoing store expansion both domestically and internationally. Costco plans 23 net store openings in fiscal year 2018. That’s in contrast to Walmart which has announced that it’s planning on closing about 10% of its Sam’s Club warehouses.

Note that Costco is very disciplined about how it opens its stores. For example, the business only targets countries where it believes customers will be attracted to the wholesale warehouse shopping experience. And even then the company is increasing its overall store base by just 2% to 4% a year.

Costco’s moderate pace of store expansion partially reflects the mature state of big box retail, but it also means the company doesn’t have to stretch its balance sheet to fund its expansion. In fact, Costco enjoys an A+ credit rating from S&P and is able to borrow at an average interest rate of 2.0%, far lower than most peers.

The company’s strong balance sheet and disciplined approach to store expansions also has another benefit for income investors: Costco is able to grow its dividend quickly and very consistently.

Costco’s quarterly dividend has grown from 10 cents per share when it was initiated in 2004 to 57 cents after the most recently announced 14% increase. That’s 13.2% annual dividend growth over 14 consecutive years of rising dividends.

While Costco’s relatively low yield may rule the stock out for those looking to live off dividends immediately, the company has appeal as a long-term dividend growth investment.

With Costco’s current dividend consuming about 25% of its free cash flow and its earnings projected to rise at a low double-digit pace, the company should be able to deliver double-digit dividend growth for the foreseeable future.

Overall, Costco is a competitively advantaged firm thanks to its economies of scale, intentionally limited product selection, quality in-store experience, strong balance sheet, and loyal base of shoppers who provide high-margin, recurring membership fee revenue.

However, as impressive as Costco’s unique business strategy has proven so far, there are still risks that investors need to keep in mind.

Key Risks

There are several risks to Costco’s continued success.

First, the company’s business model is highly dependent on its membership base, whose recurring fees provide nearly three quarters of the company’s operating profit.

Up until now, Costco has shown no signs that it’s periodic (every five to six years), membership fee hikes are hurting its retention levels. However, there is a risk that Amazon’s very popular Prime membership, which recently surpassed 100 million members worldwide and 72 million in the U.S., might eventually pose a threat.

That’s because Costco’s membership model is built around offering customers numerous avenues of value. Not just the ability to shop at highly discounted prices for bulk goods, but also purchase discounted gasoline prices, use its travel agency, pick up medications at the pharmacy, replace a car’s tires, and use its popular co-branded credit cards.

However, Amazon Prime, which originally started out offering free two-day shipping, has expanded its offerings to include free video and music streaming, and even free two-hour delivery in certain markets (and discounted one-hour delivery). With Whole Foods under its wings, Amazon could increasingly encroach on grocery-focused retailers.

Amazon is also raising its membership rates which means that Costco customers might eventually feel the need to decide between one membership or another. After all, the ultimate value proposition of each membership is to save money on low-cost merchandise.

Note that Target is launching its own membership model as well, which indicates that Costco’s unique value proposition may face stronger competition in the coming years. That will make continued execution on supply chain management and customer service essential to retaining its market share in a profitable manner.

Even as Costco gets more efficient, there is no guarantee that it will be able to keep growing its margins. In retail, cost savings often end up being passed onto consumers. That’s especially true in the age of Amazon where CEO Jeff Bezos is famous for saying “your margin is our opportunity.”

Another risk to consider is commodity price volatility, especially as it relates to Costco’s popular private label Kirkland brand, which generates about 30% of the company’s sales. Input costs are cyclical over time and thus could reduce margins, at least in the short to medium term, on a major source of the company’s sales.

It’s also worth mentioning that most of Costco’s biggest long-term growth opportunities are overseas. However, there are lots of risks associated with international expansion.

In new markets, Costco lacks the kinds of economies of scale that it enjoys in the U.S. where it’s had decades to develop its supply chain. The popularity of the suburban warehouse shopping model is also somewhat unproven in other countries, where homes and vehicles are smaller.

While the company has done a good job with overseas growth so far, it’s starting from a small base of stores. In other words, we don’t yet know how large Costco’s overseas market potential really is.

Closing Thoughts on Costco

In a retail world that’s being disrupted by the rise of e-commerce, Costco has proven that its membership-focused business model is a solid way to build enduring competitive advantages.

The company certainly faces numerous threats from fast-moving rivals like Amazon, but management’s long-term focus on customer satisfaction, a very happy labor force, and disciplined growth has proven to be one of best approaches to retail success thus far.

Despite a low yield that makes the stock unsuitable for some investors, Costco appears to be a solid long-term company to consider for most dividend growth portfolios.

To learn more about Costco’s dividend safety and growth profile, please click here.

Leave A Comment