Founded in 1917, ConocoPhillips (COP) is the world’s largest independent exploration and production oil company and is nearly twice as large as its nearest rival by production. The company explores for, produces, transports, and markets crude oil, natural gas, liquefied natural gas (LNG), natural gas liquids, and bitumen in 17 countries around the world.

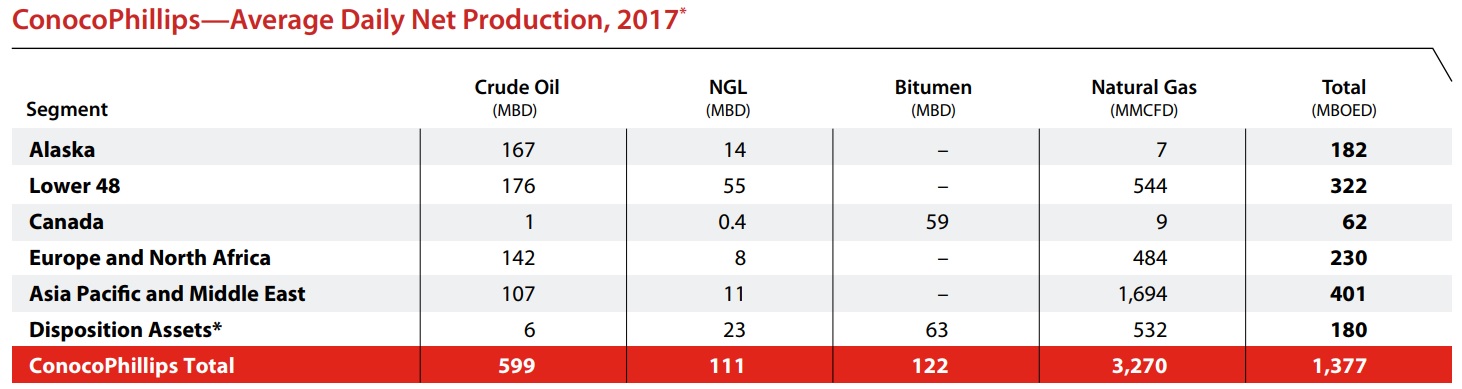

In 2017, the company averaged nearly 1.4 million barrels per day of oil equivalent production broken down as follows:

- Oil: 50% of 2017 production

- Natural gas: 38% of 2017 production

- Natural gas liquids: 7% of 2017 production

- Bitumen (viscous mix of hydrocarbons used for road surfaces and roofing): 5% of 2017 production

The firm has proven reserves of about 5 billion barrels of oil equivalent and probable reserves of 15 billion barrels, which is sufficient to cover 10 and 30 years of current production rates, respectively.The company’s production is very diversified geographically with 63% coming from outside the U.S. However, ConocoPhillips company plans to focus more heavily on U.S. shale production going forward.

Business Analysis

Independent exploration & production, or E&P, oil companies are not usually the place to look for safe dividends. Unlike integrated oil majors such as Exxon (XOM), Chevron (CVX), Royal Dutch Shell (RDS.B), and BP (BP), they lack the refining and petrochemical businesses which benefit from low oil prices (lower input costs) and provide somewhat of a cash flow hedge during oil crashes.

ConocoPhillips spun off its refining and chemical division into Phillips 66 (PSX) in 2012, leaving the remaining company as a pure-play oil & gas producer. When the price of crude oil began its prolonged plunge in late 2014, ConocoPhillips’ relatively high dependence on the price of oil ultimately forced it to slash its dividend 66% and make drastic reductions to its capex and exploration budget. The company also sold off $16 billion in assets to help pay down its debt.

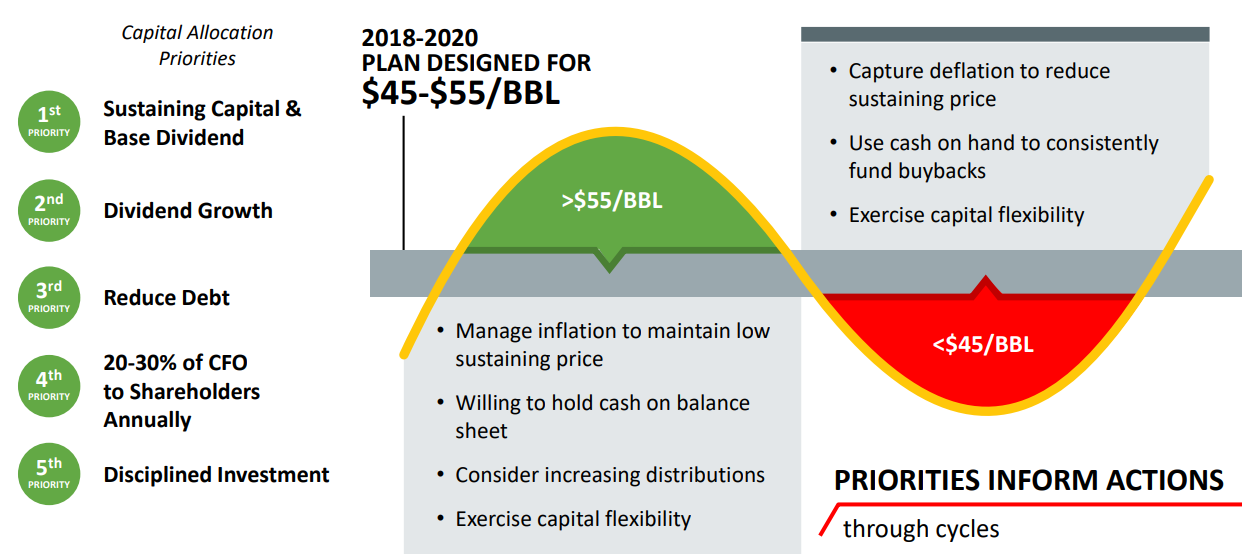

However, management has learned from its mistakes and has drastically changed its priorities to coincide with much lower potential future oil prices.

For example, the company’s top priority going forward is to maintain enough production to sustain ConocoPhillips’ current dividend. Management believes it needs 1.15 million barrels per day of production at $40 oil to do so. Therefore, Conoco has budgeted $3.5 billion a year in capex to maintain that base production rate.

ConocoPhillips’ goal is to not maximize production overall, but rather production per debt-adjusted share, or DASh. In other words, production divided by debt divided by share count. While admittedly somewhat complicated, this is a unique approach in the E&P industry that is intended to reward Conoco for reducing debt, repurchasing shares, and avoiding the urge to increase production at any cost.

Based on this proprietary metric, the company’s production per DASh increased 19% in 2017, thanks mainly to repaying 30% of its long-term debt.

In the first quarter of 2018, production per DASh increased another 16% thanks to a small (3.6%) increase in production, but mostly due to paying down another $2.7 billion in debt.

By the end of 2018, Conoco plans to pay off another $2 billion in debt thanks to the strong recovery in oil prices. At the end of the year, ConocoPhillips expects to have $15 billion in debt, and about $10.5 billion in net debt (debt minus cash). Management ultimately wants to maintain a more conservative debt/operating cash flow ratio of 2.0 or below.

As deleveraging continues, Conoco estimates it can sustain its dividend on a free cash flow basis (while maintaining production) at an average oil price of about $40 per barrel. This is due to the company’s relentless focus on maintaining low operating costs and a strong balance sheet. The company also plans to focus more heavily on oil during periods of high prices and not hedge its production to capture maximum upside cash flow potential.

Through 2020, and assuming an average oil price of $50 per barrel, the company is projecting:

- 5% annual production growth (60% from fast-growing U.S. shale)

- A breakeven sustaining price of $35 per barrel (cost to produce oil)

- A dividend breakeven oil price of under $40 per barrel

- Over 10% decrease in debt per share

- Greater than 20% returns on invested capital

The majority of the company’s production growth investments will focus on unconventional resources, mostly low-cost shale oil in the U.S. Management expects production from the Eagle Ford (East Texas) shale formation and Permian basin (West Texas) to increase by annual rates of 25% and 60% through 2020. Unconventional sources make up 8 billion barrels of oil equivalent, or BOE, of the company’s 15 billion BOE probable reserves. The company believes it can extract these reserves at $35 per barrel or less.

ConocoPhillips is very focused on lowering its production costs and believes it can reduce its cost of supply (cost to get a barrel out of the ground) by 10% in U.S. shale, 15% in LNG and oil sands, and 20% from conventional sources like Alaska, Asia, and the North Sea by 2020.

All told, the company expects its disciplined capital allocation plan to double its annual free cash flow from 2017 to about $5 billion by 2020, assuming $50 oil. If successful, the company’s free cash flow payout ratio would fall to 30%, providing a solid margin of safety. And management believes that at $60 oil, which is a distinct possibility given that oil is currently at $70 per barrel, the company might see its free cash flow soar to about $8 billion.

Sustained higher oil prices would allow Conoco to continue paying down its debt, raising its dividend, and buying back shares even more aggressively. However, even with rising oil prices, Conoco’s dividend seems unlikely to grow much beyond a mid-single-digit annual pace over the long term.

Simply put, management seems to be taking a much more conservative approach to capital allocation. Rather than maximizing oil production and dividend growth, the company is focusing on long-term sustainability in all oil price environments.

But even with such a more disciplined growth approach, there are risks to consider that might make ConocoPhillips a poor choice for income growth investors.

Key Risks

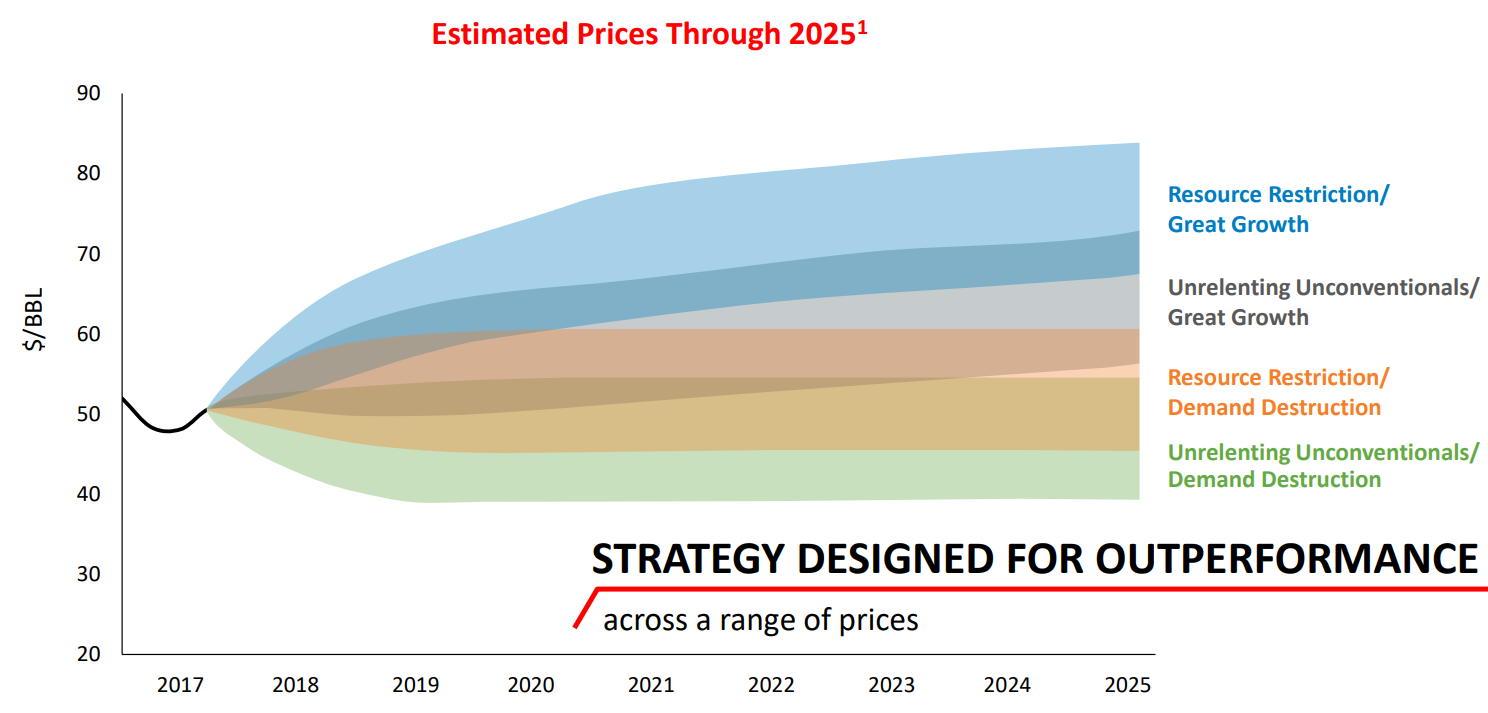

The price of oil is ConocoPhillips’ biggest business driver over any relatively short period of time, and no one can forecast where the price of oil will go. In fact, even Conoco’s internal projections show that the company is preparing itself for a highly uncertain future when it comes to oil prices.

The company has simulated long-term prices based on a range of scenarios depending on the rate at which U.S. shale oil production grows and global oil demand changes. The firm concludes that oil prices will likely average between $38 and $82 per barrel through 2025.

Note that while the high end of that range would likely spell incredible profits and potentially strong dividend growth, the low end could stress the company’s ability to maintain its current dividend.

In addition, Conoco’s latest dividend hike (7.5%) indicates that management will likely be very conservative with future dividend growth. That’s to prevent its payout ratio from rising to dangerous levels during a future oil crash.

From an income perspective, it’s hard to make a compelling case for ConocoPhillips compared to the other major oil players. Exxon Mobil and Chevron are dividend aristocrats, and Royal Dutch Shell (RDS.B) is an integrated oil major that hasn’t cut its payout since World War II. These companies all have much higher yields and equally attractive long-term dividend growth prospects.

They also have more diversified sources of cash flow, which could be increasingly important in the decades ahead. ConocoPhillips is betting most of its future growth on oil, which could face demand headwinds sooner than some analysts expect thanks to the rise of electric vehicles and renewable energy. In fact, analyst firm McKinsey believes global oil demand could peak as soon as 2030.

Despite the need to cut expenditures in today’s low oil price environment, independent E&Ps like ConocoPhillips also need to be very careful to invest enough to maintain their proven reserves. While the company has discovered about 10 billion barrels with production costs under $50 per barrel over the past decade, Conoco’s rate of reserve replacement has been very weak in recent years.

The company’s proven reserves (the amount of oil and gas reserves that Conoco can extract in future years) have fallen about 60% in the past two years, largely due to the oil crash forcing Conoco to slash its exploration budget.

Even with oil prices rising again, management expects to spend just $300 million per year on exploring for new reserves. That’s just 6% of the firm’s total annual capex budget of roughly $5.5 billion that management plans to spend through 2020.

- Maintenance capex: $3.5 billion annually or 64% of the total spend

- Production increase capex: $1.2 billion annually (22%)

- Acquisitions (new acreage): $500 million or (9%)

- Exploration (to replace reserves): $300 million annually (6%)

That’s among the lowest exploration budgets in the industry and could mean that Conoco will be unable grow its production much over time. Shale oil production (a key growth focus for the company) also declines very quickly, as much as 90% in the first year. In contract, conventional oil fields decline at about 4% per year, and LNG projects have nearly zero decline rates in the first 20 years.

This explains why Conoco plans to spend so much on maintaining its production, because it needs to continuously drill new U.S. shale wells to offset the fast decline in output from legacy wells.

The bottom line is that ConocoPhillips, while being a well-run independent oil producer, is extremely vulnerable to commodity prices in the short term. And in the long term, the company’s current growth plan leaves it exposed to disruption should the world transition away from oil and towards electric vehicles and natural gas.

Management’s disciplined capital allocation plan could be a double-edged sword for income investors as well. Conoco’s deleveraging and free cash flow growth plans likely mean its dividend will increasingly become one of the safest in the industry. However, that same focus on safety means Conoco’s payout is unlikely to grow fast enough to make up for its low yield.

Closing Thoughts on ConocoPhillips

ConocoPhillips has made a major turnaround since the dark days of the oil crisis when it was forced to cut its dividend by 66%. Major asset sales, deleveraging, and a refocus on lower cost production, especially in U.S. shale, have turned the company into a cash cow now that crude oil prices have recovered.

Over the next few years, management’s growth plans are likely to make ConocoPhillips’ free cash flow increase substantially, assuming we don’t experience another oil crash. However, the company seems to be underinvesting in exploration and increasing its reliance on oil over gas, making it more vulnerable to disruption than more diversified integrated oil companies.

ConocoPhillips’ low dividend yield, average payout growth, and less certain long-term growth runway ultimately make the stock appear less attractive compared to its major integrated oil rivals. Conservative income investors might want to avoid the company in favor of proven dividend aristocrats like Exxon or Chevron.

To learn more about ConocoPhillips’ dividend safety and growth profile, please click here.

Leave A Comment