Founded in 1999, Brookfield Renewable Partners (BEP) is a renewable energy-focused limited partnership, or YieldCo, that’s run by Brookfield Asset Management (BAM). The company is one of the world’s largest publicly-traded renewable power platforms with a portfolio consisting of over 16,300 megawatts of capacity and 843 generating facilities in North America, South America, Europe, and Asia. In total, Brookfield Renewable serves 24 energy markets in 14 countries.

The YieldCo’s clean energy distribution is dominated by hydroelectric power plants (on over 80 global river systems), though it is quickly diversifying into wind, solar, and energy storage as well.

- Hydro: 82% of power generation

- Wind: 16%

- Solar & Storage: 2%

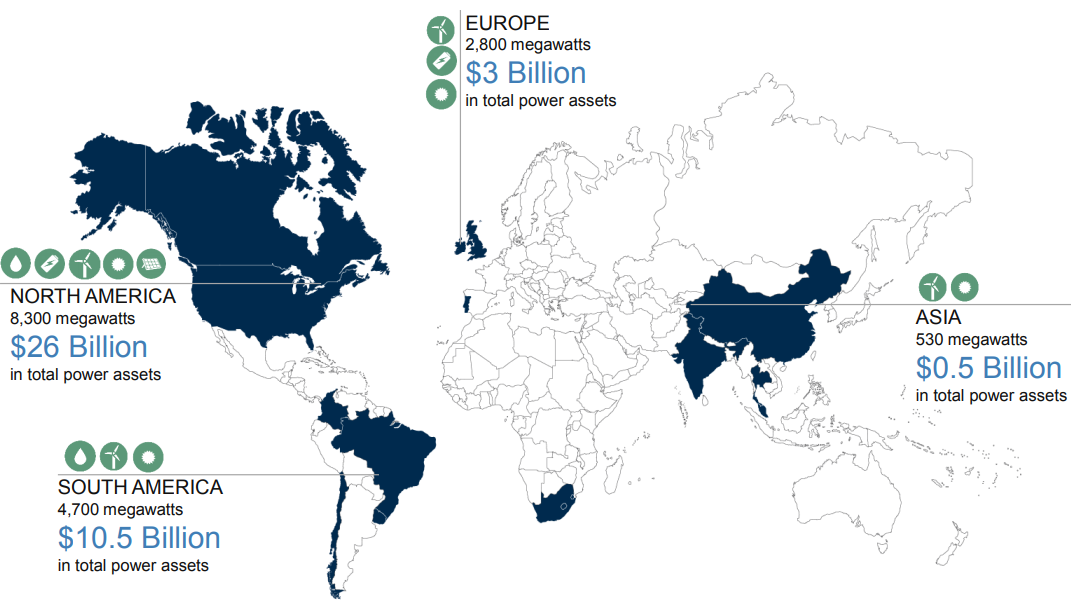

Brookfield Renewable’s operations are concentrated in North and South America today, but the company plans on greatly increasing its generating capacity in Europe and Asia in the future:

- North America: 60% of generation capacity

- Brazil: 20%

- Columbia: 15%

- Europe & Rest of World: 5%

Over 90% of the firm’s cash flows are contracted with credit-worthy counterparties, such as utilities, primarily under long-term power purchase agreements. Brookfield Renewable’s revenue is primarily correlated to the amount of electricity the company generates rather than wholesale electricity prices, providing solid cash flow visibility.

Business Analysis

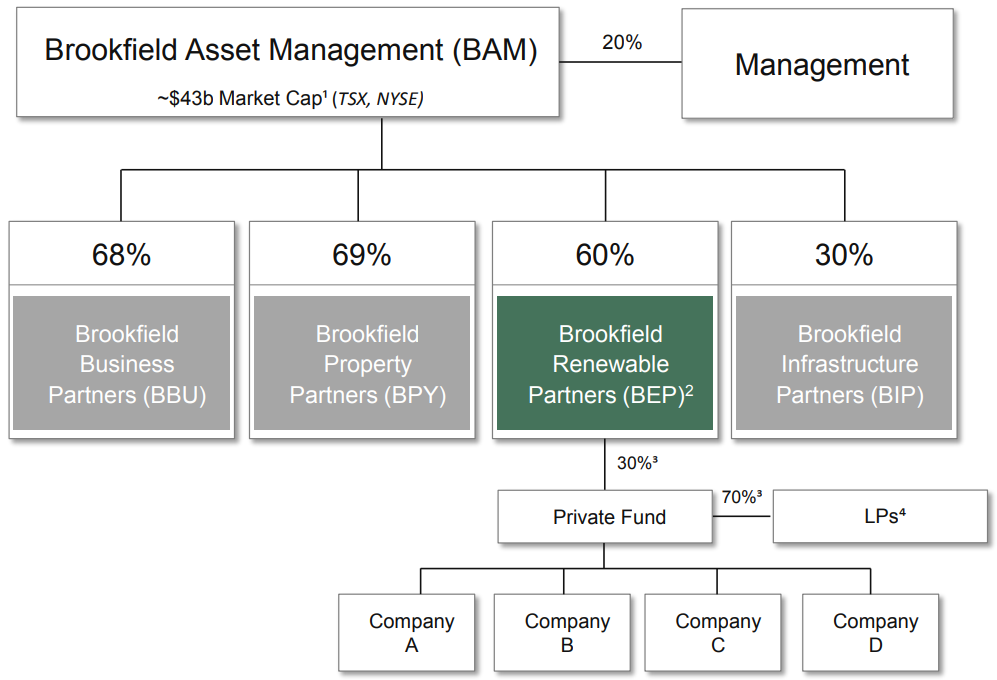

Brookfield Renewable Partners is managed and majority-owned by Brookfield Asset Management, which has 115 years of experience in investing and operating utilities, infrastructure, renewable energy, and real estate. Today the parent company has $285 billion in assets under management and over 100 offices in more than 30 countries around the world.

Brookfield Renewable is one of several limited partnerships that Brookfield Asset Management runs as part of its operations. The parent company owns 60% of the YieldCo’s limited partner units (what it calls shares) as well as its incentive distribution rights (IDRs). These give Brookfield the right to 25% of all marginal distributions in addition to the distributions it already receives from its large ownership stake.

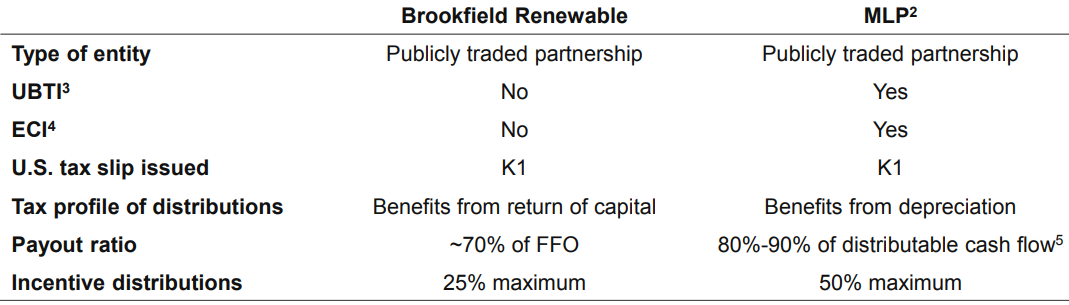

In other words, limited partnerships like Brookfield Renewable are similar in structure to master limited partnerships (MLPs). Specifically, the sponsor (Brookfield Asset Management) uses them as external funding vehicles to grow its overall asset base and cash flows.

Note, however, that most MLPs have IDR tiers of 50% while Brookfield’s is half as large. This means that regular investors get to keep more of the marginal funds from operation (FFO). It also lowers the firm’s overall cost of capital and makes it easier to grow profitably.

Another key difference between Brookfield Renewable and MLPs is that because of how it’s structured (its assets are themselves limited partnerships), it generates no unrelated business taxable income (UBTI). As a result, the stock is safe to own in retirement accounts such as IRAs and 401Ks.

Here’s how the business model works. Brookfield Renewable Partners raises debt and equity capital from investors in order to buy the attractively valued renewable power assets that Brookfield Asset Management locates for it via its globe-spanning network.

Brookfield Renewable locks in stable cash flow (over 90% of cash flow is contracted) via long-term (usually 20-year), inflation-adjusted power purchase agreements (PPAs). These contracts are mostly entered into with local utilities (43%), distribution companies (18%), and industrial users (18%). Most of these counterparties (85%) have investment-grade credit ratings, and the weighted average remaining contract is for 16 years.

The funds from operation these PPAs generate are then used by Brookfield Renewable to pay distributions to investors. Brookfield estimates that the annual investment in renewable energy in its target markets is $325 billion per year, which means that its cash flow (and distribution) have impressive long-term growth potential.

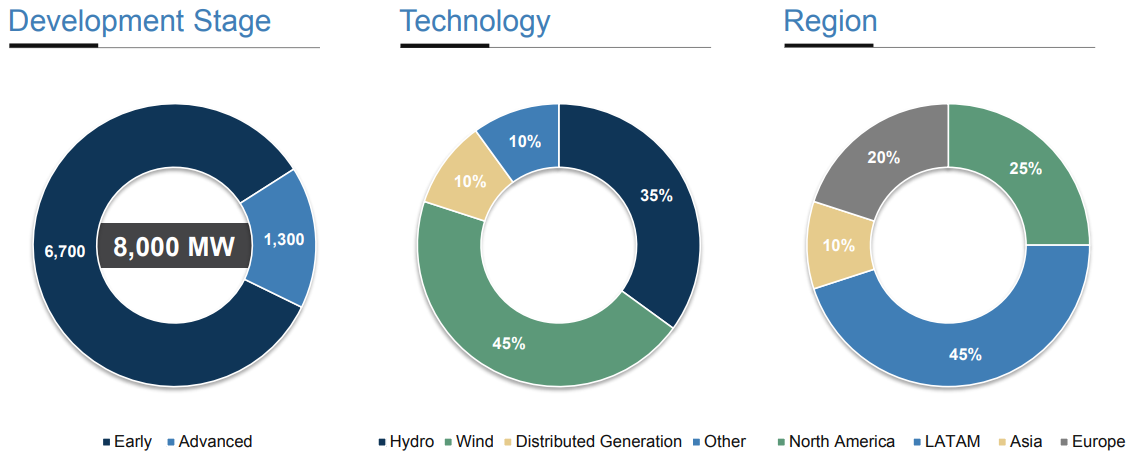

First, management sees ample opportunity for organic growth, meaning funding new construction on renewable assets or expanding capacity at existing ones. Currently Brookfield Renewable has 8,000 megawatts of new capacity projects in either early or late state development. About 65% of this capacity is non-hydro power, and roughly 35% is located outside the Western Hemisphere.

Over the long term, management expects the firm’s development pipeline to remain robust as the world’s advanced economies continue transitioning away from carbon producing power sources in favor of decentralized renewable technologies such as hydro, wind, and solar.

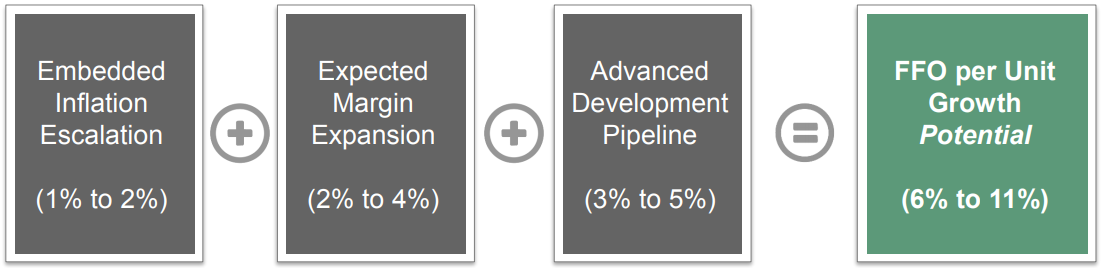

Combined with cost cutting efforts from increasing economies of scale and inflation escalators in its contracts, Brookfield Renewable believes that it can achieve long-term FFO per unit growth of 6% to 11%. That, in turn, should allow the firm to hit management’s long-term goal of 5% to 9% annual distribution growth while maintaining a reasonably safe FFO payout ratio of 70%.

The cash flow Brookfield Renewable retains after paying its distribution is used to further grow the business. Management’s ultimate long-term goal is to generate 12% to 15% annual total returns for investors, and so far the firm has actually exceeded that ambitious target (16% annual total returns since going public).

The company’s other growth catalyst is acquisitions, such as in 2017 when Brookfield spent $656 million to take a 51% controlling stake (and become the manager) in Terraform Power (TERP). TerraForm is a YieldCo who had been bankrupted by its previous sponsor SunEdison after taking on dangerous amounts of debt in an effort to grow too quickly.

Later in 2017, Brookfield Renewable acquired 100% of TerraForm Global, another SunEdison-sponsored YieldCo, for about $1.3 billion. Combined, these two transactions added 3,600 megawatts of long duration, contracted solar and wind assets in core markets such as the U.S. and Brazil to the company’s portfolio. These assets are fully operational and virtually all recently built with an average portfolio age of approximately 5 years.

Acquisitions have largely driven Brookfield Renewable’s expansion from just 950 megawatts of North American hydro power in 2009 to 16,300 megawatts of power generation from six different renewable sources in 14 countries today.

Looking ahead, Brookfield Renewable depends on two key advantages as it executes its growth plan. First, the company has one of the best long-term track records of successfully investing in and operating renewable energy assets.

Brookfield Renewable is very experienced operating globally, including in emerging markets where expertise in operating under a variety of regulatory environments is essential. In addition, Brookfield Renewable is very good at opportunistic value investing, meaning it is able to take advantage of periodic downturns in a region’s economy to strike attractive and profitable deals to acquire or build new renewable energy infrastructure. The firm can also acquire distressed assets at highly attractive prices, like it did with TerraForm.

The firm’s second competitive advantage stems from its enormous access to low-cost capital, thanks largely to its sponsor’s status as the world’s largest publicly-traded infrastructure asset manager. The company boasts a BBB+ credit rating from Standard & Poor’s and is the only investment-grade rated firm in the YieldCo industry.

However, 72% of the YieldCo’s debt is actually not at the corporate level but rather what’s called non-recourse debt. This is debt taken on by its subsidiaries to directly build or acquire renewable assets. The cash flow generated by these assets is what funds the interest and loan repayment.

Brookfield Renewable does this in part to protect itself from something catastrophic happening at one of its assets, such as a dam collapsing. In that event, the loans used to acquire those assets would default (due to lack of cash flow). However, since those debts are backed only by the assets themselves (collateral), creditors have no ability to demand repayment from Brookfield Renewable.

Simply put, non-recourse debt is frequently used by Brookfield Renewable to acquire or build long-lived, cash-rich assets in a way that insulates investors in the parent organization from credit risk.

In order to further minimize risk from its leverage, just 13% of the YieldCo’s debt is floating rate. As a result, management believes a 300 basis points increase in interest rates would impact the firm’s FFO by less than 3%.

Overall, Brookfield Renewable appears to be one of the highest quality businesses in the YieldCo space. As the largest and oldest YieldCo in the country, the firm has built up a diversified portfolio of on-trend generation assets and enjoys a cash flow stream secured by long-term contracts with credit-worthy counterparties.

Brookfield Renewable is also run by the oldest and largest global renewable asset manager, who has a great track record of generating safe and growing distributions and healthy total returns. Management’s conservatism is also reflected in the company’s solid investment-grade credit rating.

However, there are several risks to keep in mind before investing.

Key Risks

First, because of how the business is structured (as a limited partnership owning other limited partnerships), Brookfield Renewable issues a K-1 tax form each year. Many investors prefer to avoid these forms entirely due to increased tax complexity.

In addition, because Brookfield Asset Management is a Canadian company, 15% of Brookfield Renewable’s distributions are withheld for tax reasons. Tax treaties between the U.S. and Canada allow U.S. investors to potentially recoup this withholding, but it can be a complicated and lengthy amount of paperwork at tax time.

As for risks to the YieldCo itself, there are several. For one thing, operating in emerging markets (Brazil and Colombia account for 35% of power generation) creates several potential challenges. These less developed countries occasionally face political upheaval, which can cause their governments to take dramatic actions against businesses.

For example, the government could choose to nationalize (i.e. take ownership of private assets) some of Brookfield Renewable’s assets, or it could impose higher costs and restrictions on the firm’s water rights for its hydro assets. While few companies have more experience operating in such countries than Brookfield, it’s still a risk to be aware of.

Brookfield Renewable’s large presence in international markets (only 40% of cash flow is generated in the U.S.) also creates currency risk. Since the firm generates cash flow in local currencies, if the U.S. dollar appreciates against currencies like the Brazilian Real, Colombian Peso, Indian Rupee, and Chinese Yuan, Brookfield’s FFO can decline. Management does hedge against this to prevent such cash flow variability from threatening the safety of the distribution, but headwinds can still reduce the growth rate.

More importantly, while the long-term contracts covering nearly all of the YieldCo’s power generation do a nice job protecting the company from volatile electricity prices, they don’t protect Brookfield Renewable against periodic fluctuations in power output.

In other words, the company’s revenue is dependent upon available water flows and upon wind, sunshine, and weather conditions generally. A prolonged drought, weaker than expected wind conditions, and a lack of sun could result in a material drop in the volume of electricity generated by the firm’s assets, weighing on revenue and cash flow.

In fact, in recent years poor hydrology created by droughts in South America and parts of the U.S. have caused the YieldCo’s FFO payout ratio to climb higher than management would like (80% instead of the targeted 70%). As a result, Brookfield Renewable is likely to record distribution growth on the lower end of its guidance over the next few years as it attempts to bring down its payout ratio to retain more cash flow for investment purposes and increase the safety of its distribution.

Finally, while management has done a good job accessing low cost capital in the past and minimized the YieldCo’s exposure to rising interest rates, Brookfield Renewable’s underlying business model means that its long-term growth potential is still somewhat at the mercy of fickle debt and equity markets.

Rising interest rates increase the company’s borrowing costs over time, and Brookfield Renewable still needs to sell new units to finance large growth opportunities. For example, the firm’s unit count is up about 5% over the past year as the YieldCo took advantage of its strong unit price to raise capital.

However, in the event that the stock market becomes excessively bearish, a low unit price could raise Brookfield’s cost of equity to levels that make profitable growth harder to achieve, slowing the expansion of its assets, FFO, and distribution.

The firm’s access to capital also depends on its relationship with Brookfield Asset Management, who owns approximately 60% of the company and whose entities are customers for over 40% of Brookfield Renewable’s contracted generation. Should Brookfield Renewable become a less strategic business for its parent, the company’s growth potential and cost of capital would be significantly hurt.

Closing Thoughts on Brookfield Renewable Partners

Renewable energy is one of the largest long-term trends in the global economy with solar and wind power capacity expected to grow strongly for the foreseeable future. Certain YieldCos are a potentially solid way for high-yield investors to profit from the green energy boom, but it’s important to remain aware of their risks (high leverage, dependence on capital markets, complex business structure, long-term growth in renewables could disappoint, sensitivity to weather and production output, etc.).

With that said, Brookfield Renewable has one of the best risk profiles of any YieldCo. The company’s experienced management team, access to low cost capital (investment-grade credit rating), increasingly diversified portfolio of assets, long-term contracts, conservative payout ratio, and global growth runway form a potentially appealing investment case. However, high-yield investors considering the stock should only do so as part of a well-diversified portfolio given some of the unique risk factors in this space.

To learn more about BEP’s dividend safety and growth profile, please click here.

Leave A Comment