Ares Capital Corporation (ARCC) is an externally managed business development company, or BDC. The company is a subsidiary of Ares Management LP (ARES), which provides the firm’s management team. Ares Management has over 1,000 employees working around the world and manages over $100 billion in assets.

Ares Capital specializes in acquisitions, recapitalizations, mezzanine debt, restructurings, rescue financing, and leveraged buyout transactions of private middle market companies across diverse industries. The firm is the largest BDC in America by both market cap and total portfolio size. At the end of March 2018, the company had over $12 billion invested in 360 companies.

The fund typically invests between $10 million and $200 million in companies with EBITDA between $10 million and $250 million and seeks board representation. Ares Capital invests primarily in first and second lien loans and mezzanine (convertible) debt, which in some cases includes an equity component like warrants. To a lesser extent, the business also makes equity investments.

The company seeks current income and capital appreciation through its debt and equity investments in companies with a history of stable cash flows, proven competitive advantages, and experienced management teams. The cash flow generated from these investments is then used to pay Ares Capital’s generous dividend.

Business Analysis

BDCs were created by Congress in 1980 as a special type of closed-end fund regulated under the Investment Company Act of 1940. The goal was to create publicly traded investment vehicles to increase lending to medium-sized, sub-investment grade (junk bond) firms that traditional banks prefer not to lend to. In the U.S. there are about 200,000 middle market firms of this variety that generate about 33% of GDP.

BDCs are regulated investment companies, meaning that they receive preferential tax treatment in exchange for following certain regulatory requirements. Specifically, they don’t pay taxes at the corporate level if they distribute 90% of their taxable income as unqualified dividends.

They must also have at least 70% of their assets in BDC-eligible portfolio investments, meaning that most companies they lend to must have equity under $250 million and not be listed on U.S. stock exchanges.

In addition, their leverage (debt/equity) is capped by law. Before March 2018 the cap was 100%, meaning that a BDC could only borrow $100 for every $100 in equity. Note that this limitation doesn’t apply to debt borrowed from the Small Business Administration, or so-called SBIC loans if the SEC granted special exemptions.

In March 2018, as part of the omnibus spending agreement in Congress, the leverage limit was raised so a BDC can now borrow $200 for every $100 in equity. The industry had been lobbying to obtain high leverage for five years under the argument that it would allow them to increase lending to middle market companies and thus increase economic growth and job creation. In April 2018, Ares Capital announced it plans to take advantage of this regulatory change to boost leverage.

The fundamental business model of a BDC is to raise debt and equity capital from investors (by selling bonds and shares) and then invest mostly in subordinated debt provided to riskier middle market firms at high interest rates. Subordinated debt is lower on the capital stack than secured bonds (and thus higher risk) but still safer than common or preferred equity. This means that in the event of a bankruptcy, Ares gets paid before a borrower’s shareholders but after senior bond holders.

The difference between these interest rates and borrowing costs is known as the net margin spread, which provides the profits from which BDCs pay dividends. Ares Capital’s average yield on income-producing securities is 8.9%. Such high-yield loans, combined with leverage, have allowed Ares Capital to average 9% to 12% returns on equity.

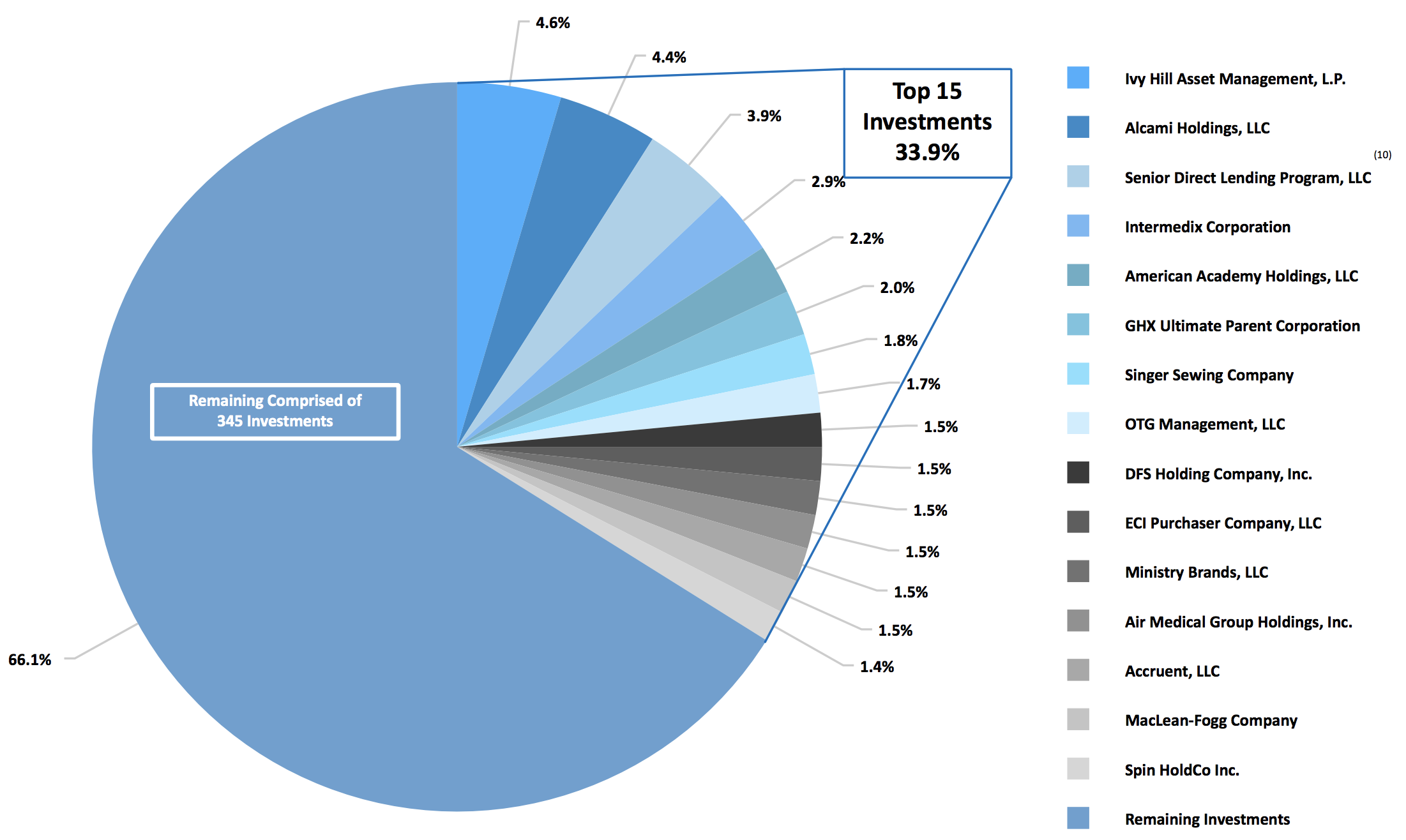

In January 2017, Ares Capital closed on the $4.2 billion acquisition of rival BDC American Capital, which boosted its assets by about 25% and made it by far the largest BDC in America. The acquisition allows Ares Capital to make deals far bigger than any other BDC can, up to $400 million in size. It also created the industry’s largest and most diversified portfolio, with investments in 360 companies with the largest representing just 4.6% of the portfolio’s value.

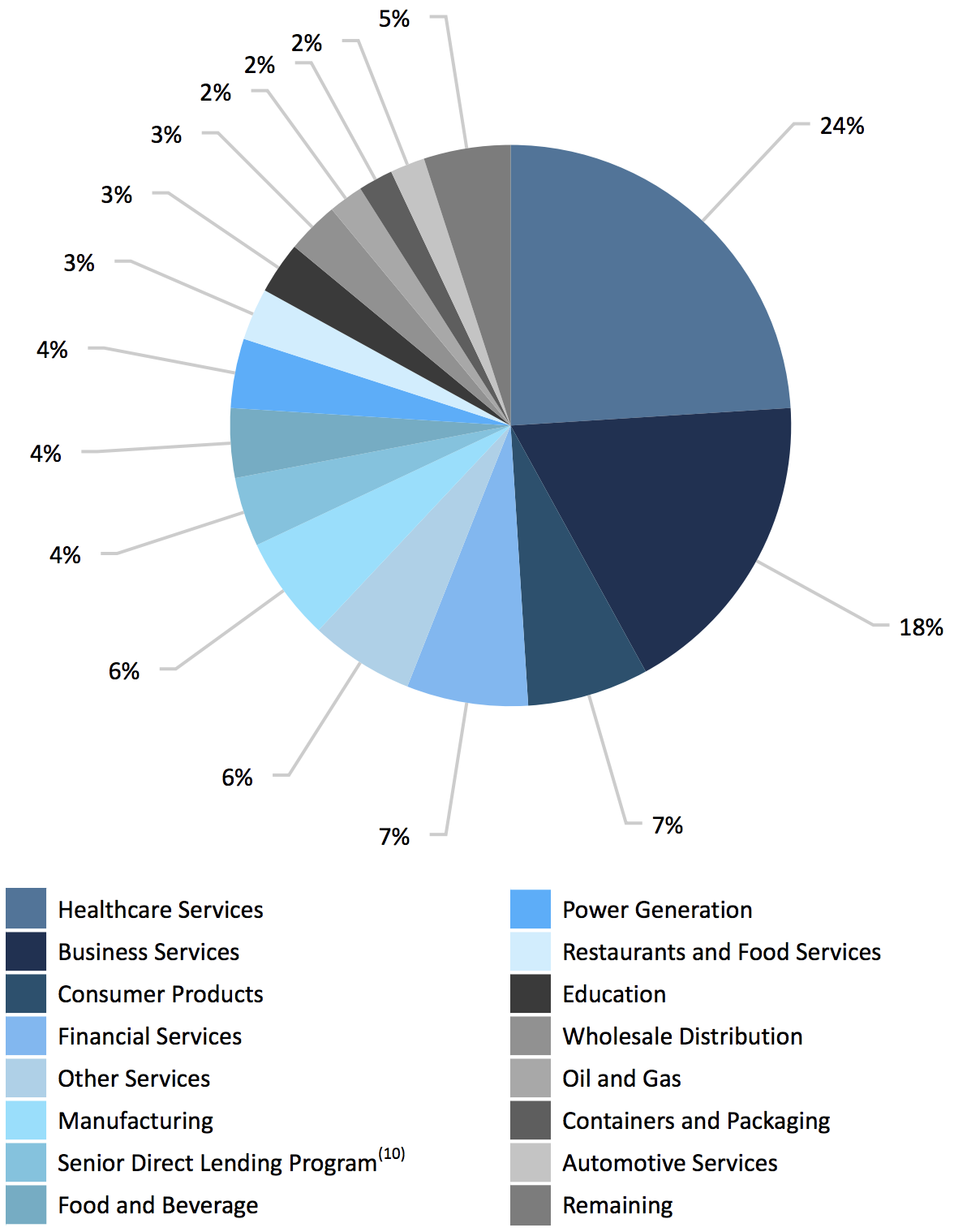

The BDC’s portfolio is also highly diversified by industry with relatively little exposure to cyclical industries such as oil & gas (5% of the portfolio). As you can see, healthcare services (24%), business services (18%), consumer products (7%), and financial services (7%) are Ares Capital’s largest industry exposures.

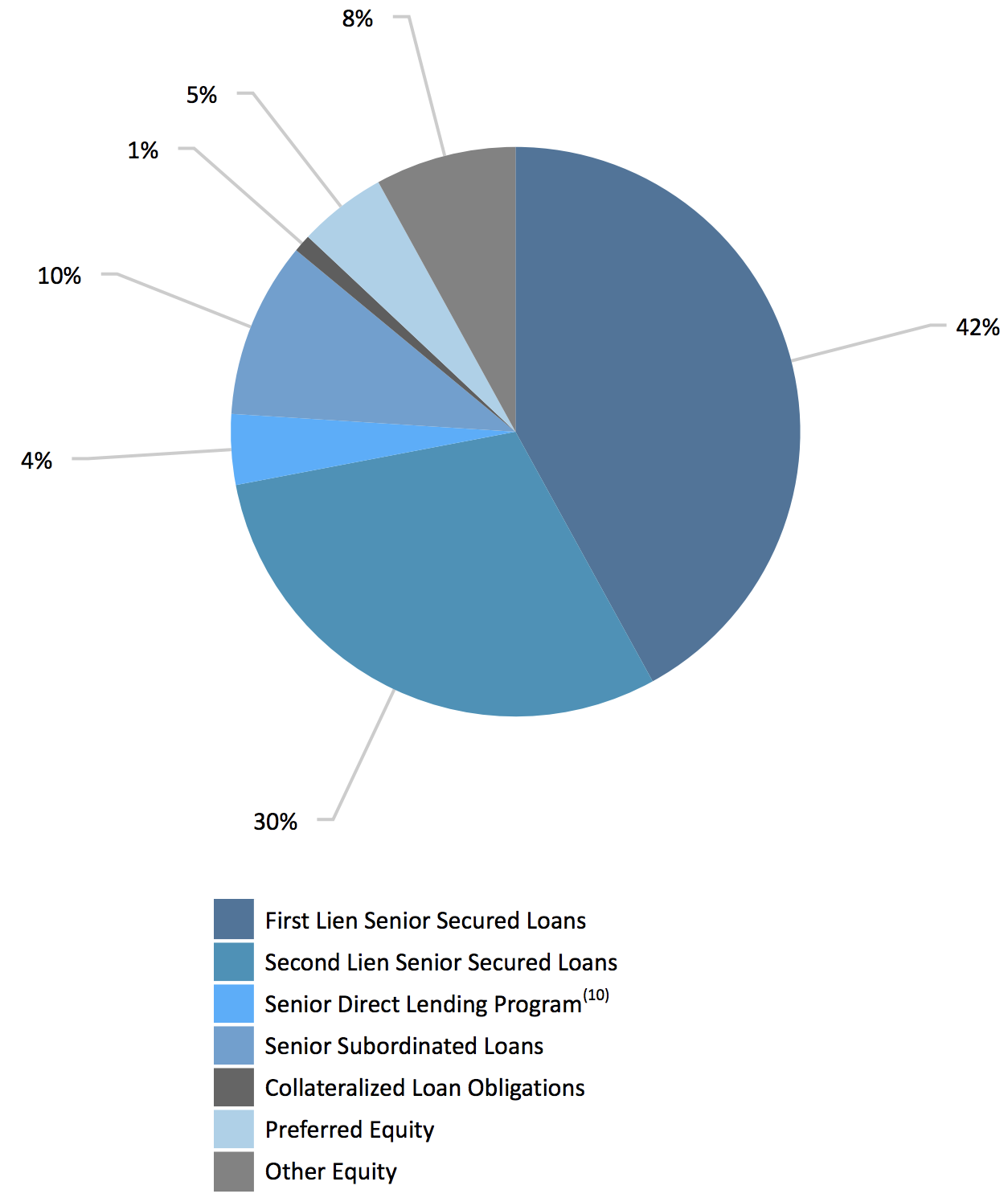

While the firm still has a relatively large (30% of the portfolio’s fair value) amount of higher risk second lien debt, Ares Capital has recently been focusing much more on first lien loans, which reduce its risk of a permanent loss in case a borrower defaults. That’s because in the event of a default, Ares Capital will be first in line to obtain the assets of the company it borrowed to which can be sold to recoup its investment.

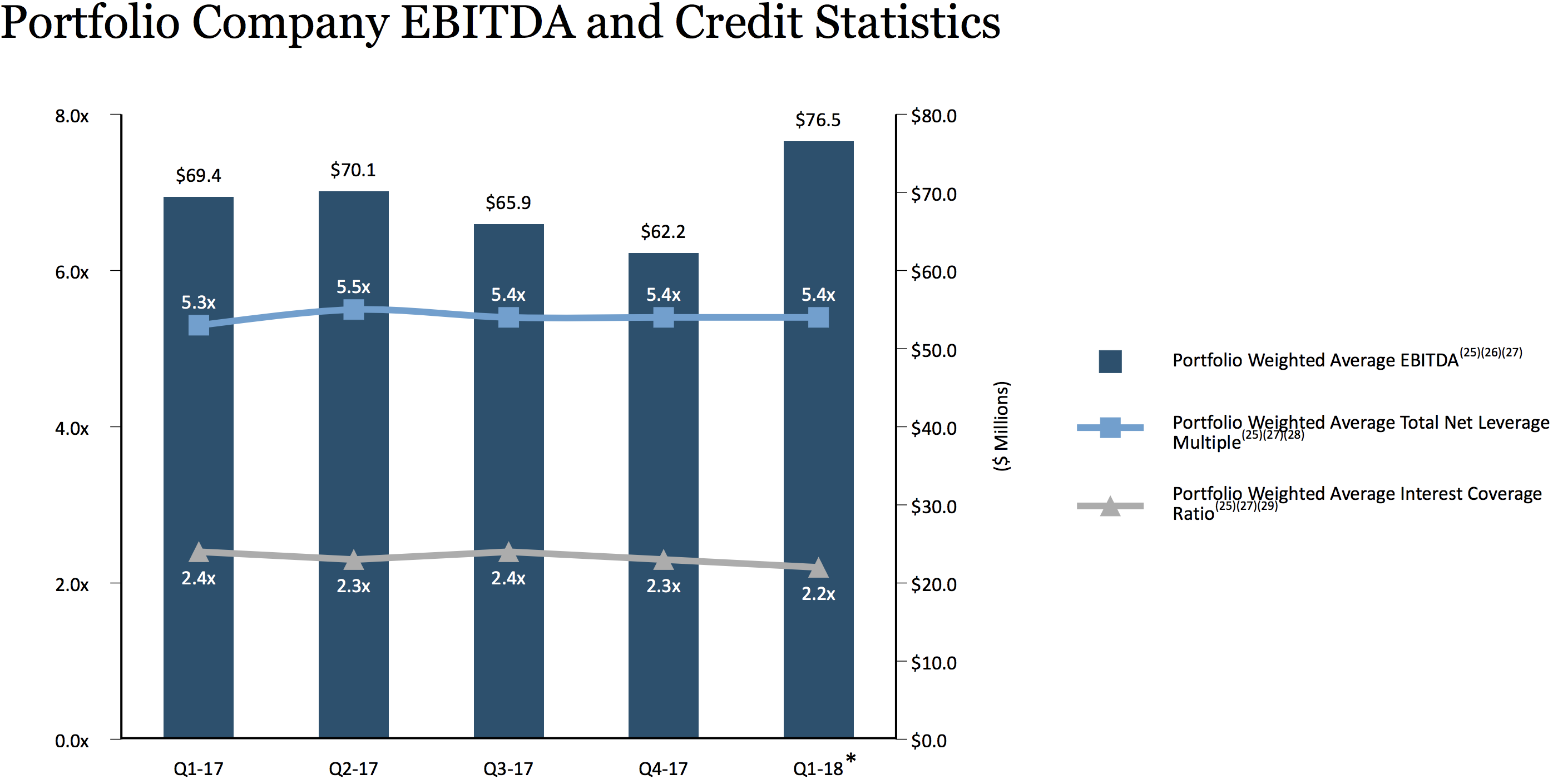

Generating safe income and recouping the full value of its investments can be very challenging during recessions because Ares Capital’s average loan is to a company with annual EBITDA of just $77 million, a relatively high debt/EBITDA (leverage) ratio of 5.4, and an interest coverage ratio (operating cash flow/interest) of just 2.2. In other words, these portfolio companies generally have little margin for error.

Since BDCs serve as financiers of smaller, sub-investment grade companies, prudent risk management is essential. Management has to perform thorough due diligence ahead of time to ensure it doesn’t underwrite large loans to bad companies on which it will later realize losses.

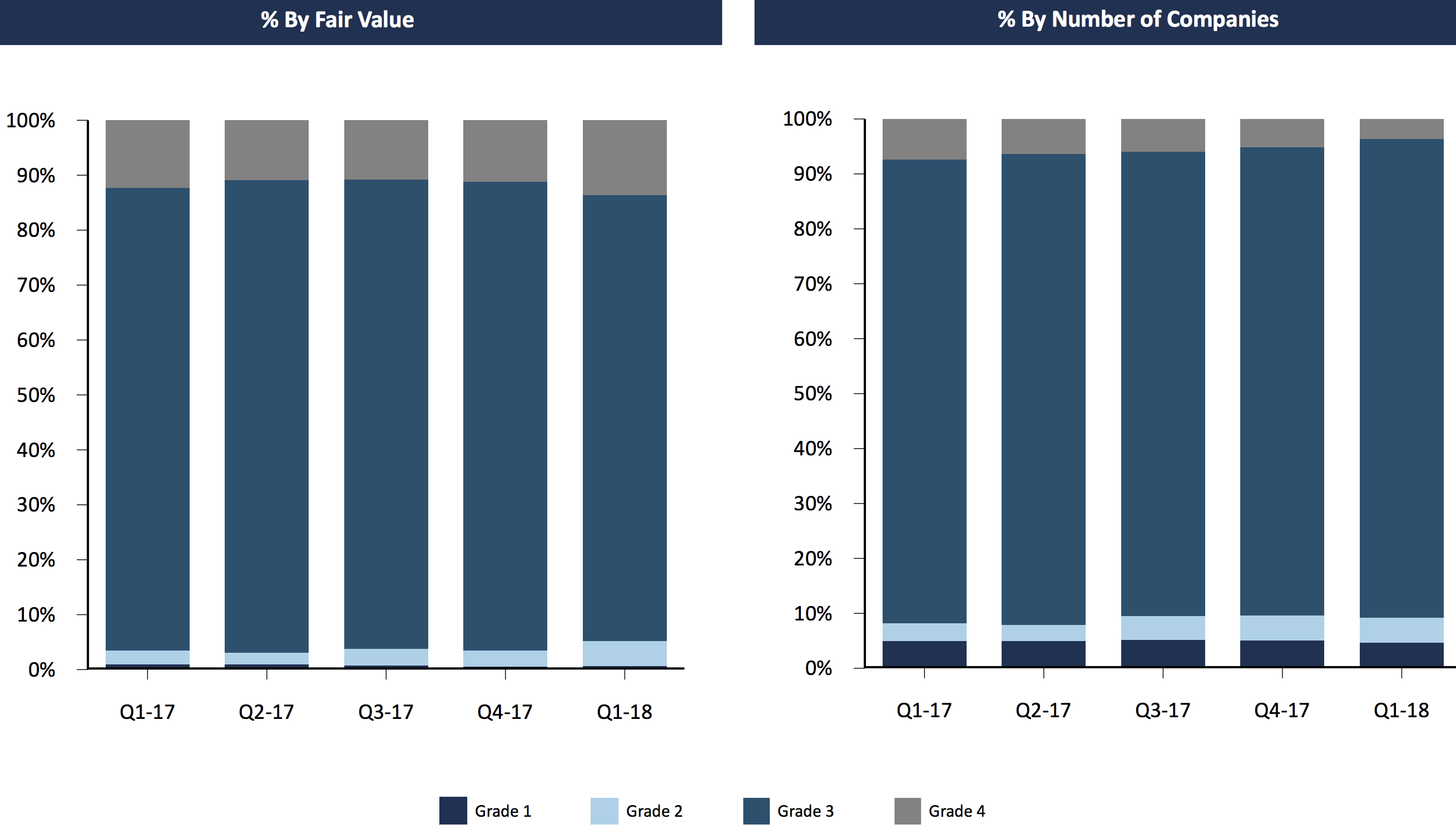

And once a loan is made, Ares Capital has to monitor the performance of the borrower, both in terms of repayments but also its fundamentals. To do this, Areas Capital has developed a proprietary risk management system that classifies investments by numbers ranging from 1 to 4. The higher the score the lower the risk of a permanent loss of capital.

- Grade 4: lowest loss risk on cost basis, company is performing well and Ares expects to make the expected profit on this investment

- Grade 3: average loss risk equal to initial cost basis, company is no better or worse off then before Ares invested in it.

- Grade 2: risk of loss has increased since initial investment due to deterioration in borrower’s business. Debt repayments are under 120 days past due.

- Grade 1: high risk of permanent capital loss. Borrower is struggling and in violation of debt covenants and payments are more than 120 days past due. Ares expects to realize a loss on these investments.

Ares Capital estimates that about 3% of its portfolio currently consists of investments in grade 1 or 2 investments made to 7% of its borrowers who are struggling. The vast majority of its portfolio continues to benefit from a strong U.S. economy. As a result, the non-accrual rate on its portfolio is just 2.8% of invested capital today, which is below the 5.1% industry average for junk bond loans.

Besides its scale, diversification, and focus on relatively less risky borrowers, Ares Capital gains advantages from its affiliation with Ares Management, whose experience ($45 billion in deals closed since 2004) and investment sourcing infrastructure allow it to source very large amounts of loans for the BDC.

For example, Ares Management provides Ares Capital with over 100 direct loan origination officers in six U.S. offices. Their deep industry connections (and an average of 22 years of industry experience) allow them to work directly with more than 400 loan sponsors. Thus, Ares Capital has less trouble finding large quantities of new loans and investments to make compared to smaller BDCs.

It also allows Ares Capital to be more selective with its deals and underwrite fewer riskier loans. For instance, the firm usually only closes on 4% of deals management considers. This kind of selectivity is why in 2009, during the financial crisis, the BDC’s non-accrual rate (i.e. loans not making payments) was just 2.5% compared to 10.3% for the industry average.

Ares Capital’s size and relationship with Ares Management also allow the firm to borrow at fairly low fixed rates (average interest rate 4.2%) and then lend to companies at higher floating (variable) rates averaging 8.9%. Ares Capital also matches its borrowing to the duration of its loans (usually five to six years long), locking in its borrowing costs and minimizing its own interest rate risk.

Currently 89% of Ares Capital’s debt is fixed rate while 79% of its loans are floating rate. Note, however, that due to management’s confidence that interest rates will continue to rise for several years, the BDC’s most recent lending was for much safer (71% first lien loans, 29% second lien) loans, 100% of which were at floating rates. The average yield on these safer loans was slightly lower (8.7%) but Ares Capital expects that to rise over time, increasing the profitability on these investments.

Management estimates that if floating rate loans (indexed to LIBOR, the global commercial lending standard rate) rise by just 100 basis points, then it will see its core EPS rise by 11%. And if rates keep rising due to a stronger global economy, then Ares Capital’s core EPS potentially benefits as much as 33% from a long-term increase in LIBOR of 300 basis points.

Ultimately, Ares Capital stands to potentially benefit from several positive growth catalysts including a continued decline in banks lending to middle market companies. That’s largely due to stricter financial regulations that force banks to hold safer investment grade loans on their books and is why bank market share in middle market lending had fallen to 9% in 2017 compared to 71% in 1994.

The firm’s other growth catalysts are increased use of leverage and rising interest rates, which could potentially cause Ares Capital’s total investment income to soar in the coming years.

While that may be great for the BDC as a whole, be aware that there are several major reasons why investors may not benefit nearly as much. In fact, Ares Capital, like most BDCs, has several major flaws that might make it a poor choice for risk averse income investors.

Key Risks

The biggest thing investors need to understand about BDCs is that almost all of them are externally managed, meaning they are effectively run as hedge funds that pay management first. Ares Capital has three forms of management fees: a base fee, an income incentive fee, and a capital gains incentive fee.

The base management fee is 1.5% of assets other than those purchased with cash. In other words, Ares Capital has an incentive to grow its assets by maximizing how much equity (shares) it issues and borrowing more (to maximize leverage).

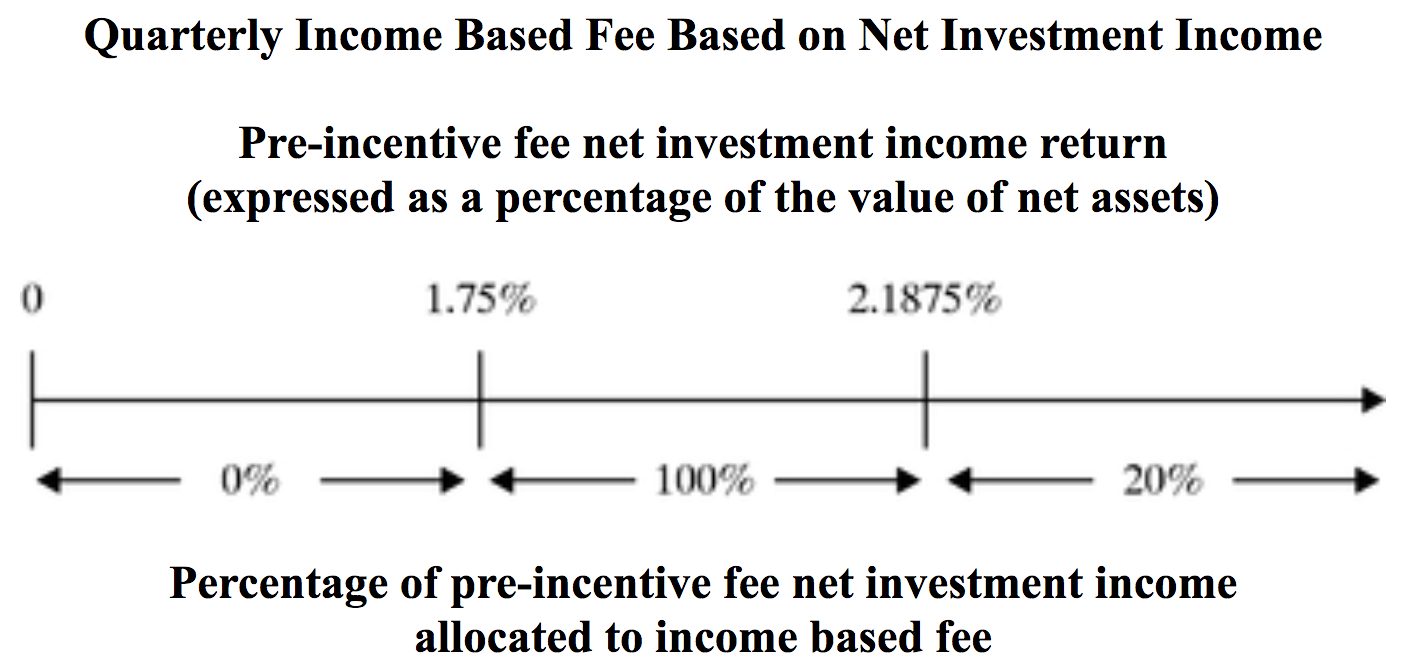

In addition, Ares Capital’s management is paid two forms of incentive fees. The first is an income fee based on growth in net investment income, or NII (not on a per share basis) above a hurdle rate of 1.75% per quarter. Net investment income is the profit a BDC makes on its loans.

Note that between 1.75% and 2.1875% there is a so-called “catch up” period in which management receives all of the growth in NII (profits). Above 2.1875% year-over-year NII growth, management collects 20% of the profit growth. Again, this growth is on an absolute, not per share, basis.

Ares Capital also has a capital gain incentive fee that is 20% of any capital gains (profits) on loans or equity positions that are sold.

The problem with such management fee structures is they are not based on per share metrics, which is what investors should care about. It creates an incentive to boost management pay by growing assets and net interest income and capital gains for their own sake, even if core earnings per share and net asset value per share (off which BDCs are valued) decrease or stay flat over time.

For example. here’s how much Ares Capital’s management was compensated in recent years:

- 2016: $255 million or 25.2% of revenue

- 2017: $346 million or 29.8% of revenue

- Q1 2018: $104 million or 32.8% of revenue

As you can see, management’s cut of revenue has been growing quickly, which harms investors in several ways. First, it means that total costs are higher (management fees make up about 50% of total BDC expenses). In fact, in 2016, 2017, and the first quarter of 2018, Ares Capital’s annual costs/assets (the key industry expense ratio) was 5.4%, 5.3%, and 5.6%, respectively. That’s much higher than the average BDC’s 3.3% expense ratio, and most banks are below 3%.

For further comparison, Main Street Capital’s (MAIN)’s expense-to-asset ratio is just 1.5%. Main Street is one of the few internally managed BDCs, meaning that management works directly for shareholders and doesn’t benefit from hedge fund-like fees.

To put it another way, Ares Capital, despite having the largest scale in the industry, does not really benefit from economies of scale, or at least its shareholders don’t. In fact, the BDC’s core EPS has been struggling to cover the annual $1.52 dividend in recent years thanks to the large amount of shareholder dilution created by Ares Capital frequently selling new shares to increase its asset base including the American Capital acquisition.

- 2016: $1.61 core EPS vs $1.52 dividend (payout ratio 94%)

- 2017: $1.39 core EPS vs $1.52 dividend (payout ratio 109%)

- Q1 2018: $0.39 core EPS vs $0.38 dividend (payout ratio 97%)

The good news is that the 2017 decline in core EPS was primarily a result of the large dilution created by the firm’s acquisition of American Capital. Now that the deal is closed, the company’s core EPS is once again covering the dividend.

The bad news is that Ares Capital’s underlying business model isn’t structured in a way that provides safe and growing dividends over time. For instance, its payout ratio has frequently been near or above 100% over the last few years, and the BDC was forced to cut the dividend during the financial crisis by 17%. Most externally managed BDCs also reduced their payouts, but internally managed Main Street actually grew its dividend during the crisis.

Ares Capital’s quarterly dividend has never returned to its pre-crisis high of $0.42 per share but has been frozen at $0.38 since 2012, even despite substantial increases in its asset base. Simply put, most BDCs, given their penchant for external management which incentivizes growth in assets over growth in core EPS or NAV per share, aren’t reliable stocks for conservative investors seeking sources of safe and steadily rising income.

NAV per share growth is especially important because BDCs must frequently issue new shares to raise growth capital. Remember that BDCs are required by law to pay out 90% of taxable net income as dividends, so they retain very little earnings to fund asset growth.

Borrowing is one way to fund growth, but legal (and safety) requirements mean that a BDC can only take on so much debt. That’s when NAV per share comes in. NAV per share represents a BDC’s net assets divided by its shares and is used in this industry as a proxy for fair value.

If a BDC’s share price is trading below its NAV per share, it means that any shares sold to increase assets actually dilutes investors enough to offset any benefits from the additional income those assets produce. In other words, core EPS can fall despite total investment income rising due to a larger asset base.

Another way to think about it is that a BDC’s NAV per share represents how much investors are willing to pay for $1 in net assets. Currently, Ares Capital’s price/NAV is 0.99, meaning that investors are willing to pay $0.99 for each $1 in net assets. In contrast, Main Street Capital trades at a price/NAV of 1.65, indicating investors are willing to pay $1.65 for each $1 in existing assets.

Some investors think that buying a BDC at a price/NAV below 1 is a good deal. After all, you are buying $1 in income-producing assets for less than a dollar. However, that’s the wrong way to think about valuation in this industry.

A BDC which historically trades at close to 1 or below 1 times NAV (also called book value) is the market’s way of signaling that management doesn’t deserve a premium because it can’t earn good returns on capital. In contrast, a BDC that has consistently grown its NAV per share, core EPS, and dividends over time, in all manner of economic environments, is one that deserves a premium.

Since a BDC’s share price usually tracks NAV per share over time, a declining NAV per share typically means a falling share price, which results in even higher costs of equity in the future.

In other words, due to how BDCs fund their growth (with large amounts of equity), a premium valuation is actually beneficial in the long-term because it allows proven winners (like Main Street) to keep growing quickly. In essence, these BDCs benefit from low costs of capital and can more easily sell new shares to fund profitable growth.

Ares Capital is not a low quality BDC as far as externally managed firms go. For instance, its average price/NAV since IPO has been 1.04. Investors believe that management has usually warranted a slight premium, which has allowed the BDC to grow its NAV per share by 4% in the past five years. While that’s better than many smaller, poorly managed BDCs, it still pales in comparison to Main Street Capital, which has grown its NAV per share by 27% during this time.

Since Main Street’s cost structure is much lower than Ares Capital’s, it can be more conservative with its business, meaning lower leverage and safer (first lien) loans. While the yield on such loans is not as high, the lower cost structure means Main Street is ultimately more profitable and can safely grow its dividend over time. In contrast, Ares Capital’s high cost structure means it needs to take on more risk (reaching for yield) and higher leverage in order to just maintain its current dividend.

Finally, realize that BDCs are largely at the mercy of the health of the U.S. economy since they lend to smaller sub-investment grade companies to generate their investment income. The U.S. is experiencing its second longest economic expansion in history. Despite this relatively good business climate, externally managed BDCs like Ares Capital have still struggled to grow their underlying NAV per share and core EPS. Again, that’s due to management focusing not on maximizing per share value but overall asset size to maximize its fees.

As a result, dividends have basically remained frozen for years, but are still below their pre-recession highs. Given that Ares Capital has so little safety cushion in its payout ratio, it’s likely that the next economic downturn (whenever it comes) will lead to higher loan losses and defaults on interest payments. That’s especially true now that management plans to boost its leverage by up to 50% which will greatly amplify any future losses.

In other words, Ares Capital is likely to cut its dividend yet again over a full economic cycle. In fact, in 2009 Ares Capital’s non-accrual rate was 2.5%, and it was forced by lack of access to credit markets to reduce its dividend. The firm’s non-accrual rate is 2.8% today despite a much stronger economy. Combined with higher leverage, Ares Capital’s core EPS is likely to take a big enough hit in the next recession to potentially require a much larger (20%+) dividend cut.

While Ares Capital may be a relatively well-run BDC and capable of closing the largest deals in the industry, it also represents a “fair weather” investment that isn’t likely to hold up well during a recession.

Closing Thoughts on Ares Capital Corporation

The BDC industry is known for its high yields, but those dividends come at a very high cost. That includes very complex and highly levered financial structures, enormous management fees (and poorly aligned incentives between management and shareholders), and high sensitivity to the health of the U.S. economy.

As far as externally managed BDCs, go Ares Capital is a relatively good choice, representing the largest and most diversified firm in its industry. It also has access to the industry’s largest source of deal flow (via Ares Management), enjoys relatively low cost borrowing, and should benefit from rising interest rates.

That being said, Ares Capital represents one of the nicest houses in a bad neighborhood, one that is notorious for cutting dividends during economic downturns. Investors determined to invest in the BDC space should consider sticking to the best run internally managed companies.

A business such as Main Street Capital is a more conservative option and benefits from having the lowest cost structure in the industry. Main Street also boasts a disciplined management team with a proven track record of highly conservative underwriting and slow but steady dividend growth, even during the financial crisis.

To learn more about Ares Capital’s dividend safety and growth profile, please click here.

Leave A Comment