Founded in 1997, Annaly Capital Management (NLY) is the largest and oldest mortgage REIT (mREIT) in America with over $100 billion in assets. The firm primarily invests in residential mortgages that are guaranteed by Fannie Mae and Freddie Mac.

Like all mREITs, Annaly’s business model involves borrowing at short-term (lower) interest rates, in order to fund the purchase of longer-term, higher-yielding assets, mostly residential and commercial mortgage-backed securities (MBS). Combined, these securities collectively make up 97% of the firm’s asset base.

The difference between short-term borrowing rates and the yields Annaly earns on its investments is the net interest margin, or “spread,” which is how the company makes money. Combined with a high amount of leverage (6.5:1 as of the first quarter of 2018), this strategy creates around a 10% levered return that generates the company’s profits and funds the stock’s double-digit dividend yield.

Since REITs must pay out 90% of taxable income as unqualified dividends in order to avoid paying taxes, mREITs have some of the highest dividend yields in the market. However, it’s very important to understand that the mREIT business model is very different than that of its equity REIT cousins (who own physical rental properties). As a result, mREITs like Annaly are unsuitable for all but the most risk-tolerant income investors.

Business Analysis

Unlike equity REITs, which generate stable rental income from leasing out physical real estate properties, mREITs like Annaly should be thought of as financial companies. They own no permanent assets, but rather operate purely on the basis of interest rate arbitrage, profiting from differences in interest rates on various assets. The firm’s assets eventually mature and must be replaced, meaning that mREITs like Annaly have extremely volatile revenue and earnings over time.

In addition, mREITs are among the most interest rate sensitive companies in America. This is because Annaly’s main funding source is the repurchase, or repo, market. For this type of financing, Annaly sells some of its assets in order to raise funds, promising to buy them back at a slightly higher price in a few weeks (usually 14 to 72 days).

The repo market is extremely volatile since it is affected by short-term interest rates that are largely driven by 2-year Treasury yields and commercial lending rates, which both rise when the Federal Reserve increases interest rates. Today the company’s average borrowing cost is 1.9%. In contrast, the average interest rate on its agency-backed (government-insured) mortgage bonds is 3.75%.

In recent years, Annaly has been diversifying and is technically considered a hybrid mREIT, meaning that it owns a mix of assets, including residential mortgage assets, commercial assets, and middle market (subprime) commercial loans (think BDC).

However, since 95% of its assets are still in residential mortgages, the company is still effectively an agency mREIT. In other words, it uses high leverage and is very exposed to several aspects of long-term interest rates (which affect mortgage rates). For example, Annaly has a lot of so-called prepayment risk. When mortgage rates are falling, in addition to lowering the yield on its residential MBS portfolio, more homeowners can refinance by taking out a new mortgage to pay off an existing one, cancelling it out.

Residential mREITs buy their MBS at a slight premium which needs to be amortized over time in order to earn a profit. If prepayments rise too high, then mREITs can incur steep losses on past investments.

So when interest rates are falling, Annaly’s business model can be hurt. However, when interest rates are rising, this can also cause trouble for the company due to its high leverage.

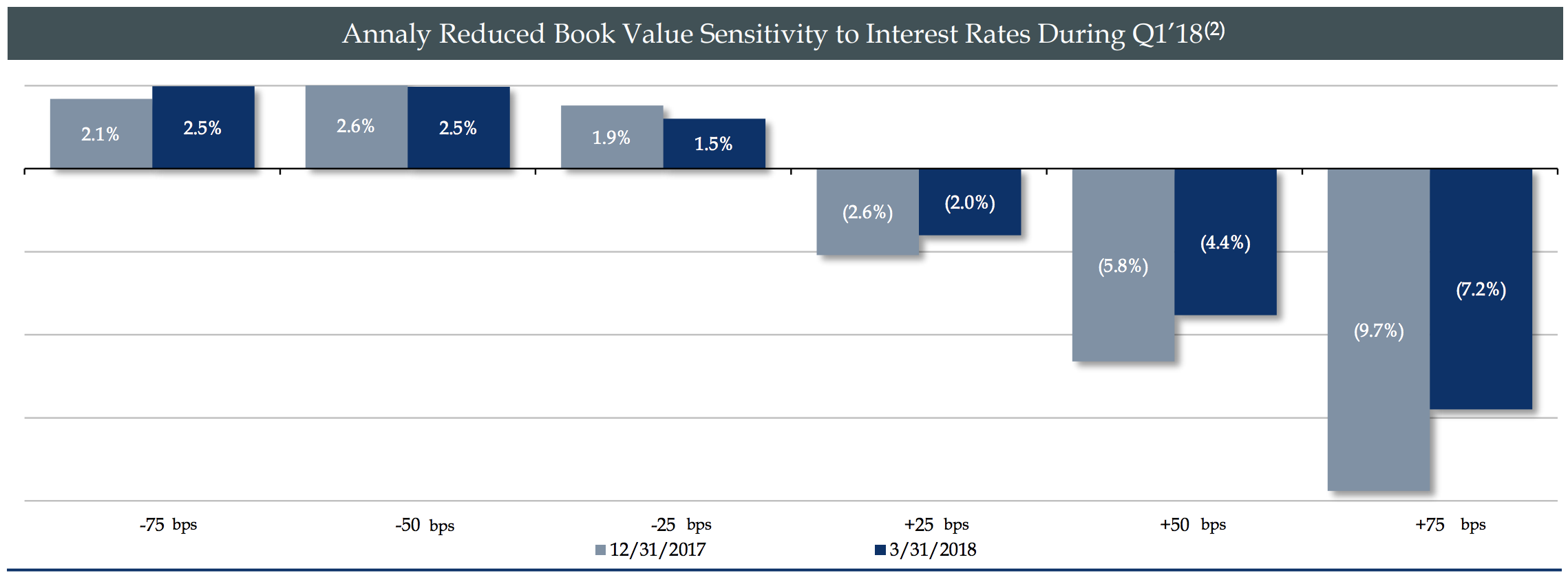

Remember that like bonds, the value of Annaly’s MBS portfolio will move in the opposite direction of interest rates. That’s because higher rates mean that older MBS need to sell at a discount in order for their effective yields to compete with newer, higher-yielding mortgage-backed loans.

As a result, Annaly’s book value, or net asset value (i.e. the fund’s value), will decrease as rates rise. For example, if long-term interest rates (10-year Treasury yield) rise 75 basis points, the value of Annaly’s existing portfolio would decline by 7.2%.

But if higher yields also mean more income for new investments, then why does it matter if the firm’s loan portfolio declines in value?

That’s because mREITs are constantly needing to raise new equity growth capital due to the 90% taxable net income payout requirement from the IRS. In fact, in the past 12 months Annaly has raised about $2.8 billion in new equity (including preferred shares).

An mREIT’s stock price is typically a function of its net asset (book) value (Price / NAV is the most commonly used valuation metric in this industry). So if Annaly’s assets decline in value too much, its cost of equity can rise significantly, making it harder to fund profitable growth.

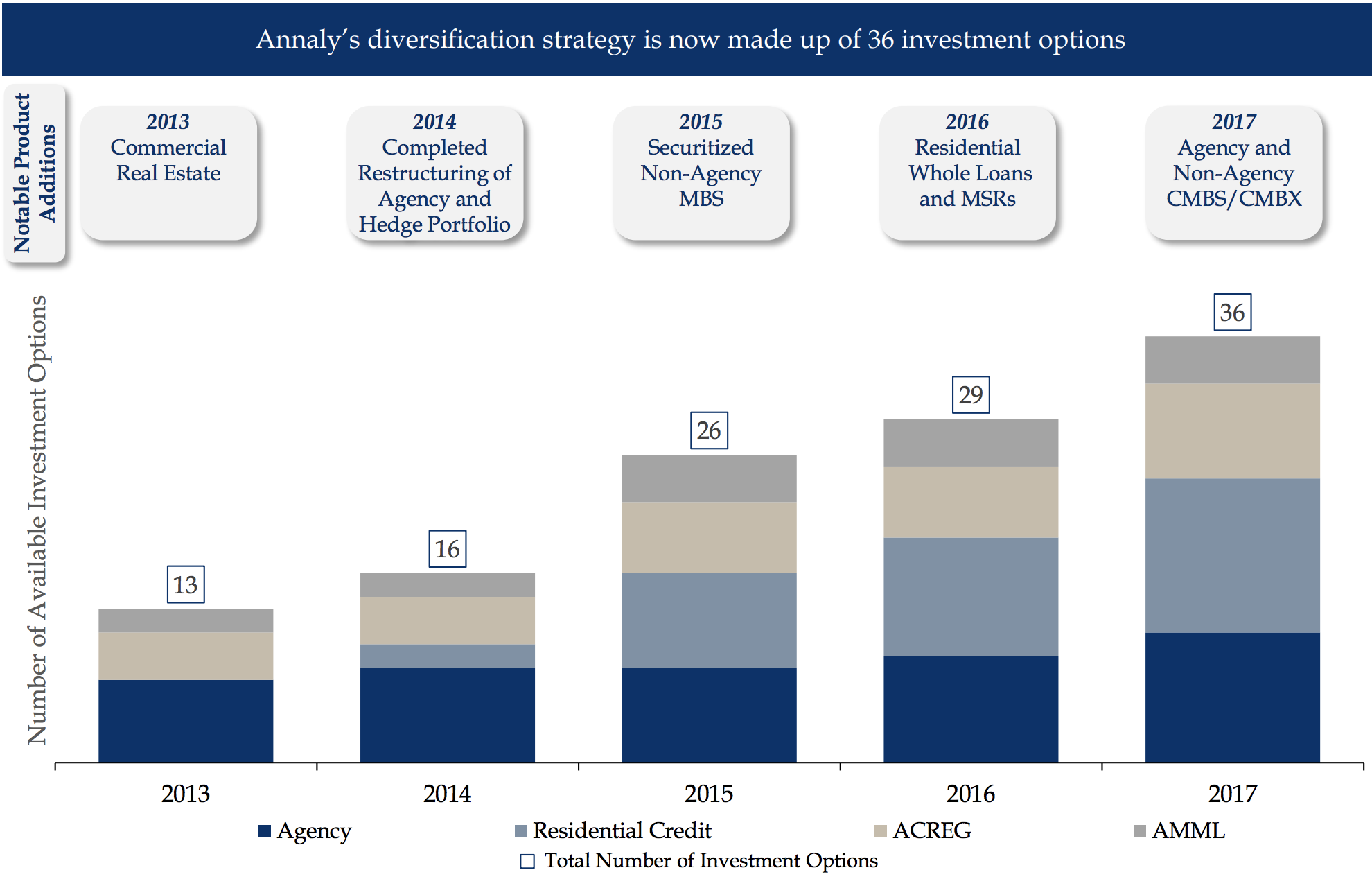

Over the past five years, Annaly has attempted to diversify away from residential mortgage assets and stabilize its earnings (as much as is possible in this industry) by tripling its number of investment options.

However, the downside to diversifying this way is that the business model continues to get more complicated since the profitability of each new investment option has different sensitivities to interest rates. In addition, the net spread on different business models is affected by the supply and demand balance imposed by other mREITs, as well as private equity and hedge funds that are increasingly active in this space.

To manage all these moving parts (and risks), the company needs experienced management, which is provided by Kevin G. Keyes. He is Annaly’s Chairman and CEO and has 27 years of industry experience. In other words, he knows how to adapt to changing conditions, especially shifts in interest rates that can dramatically impact the mREIT’s earnings.

Despite extreme interest rate environments, Annaly’s management team has been able to outperform all major high-yield investment classes since 2014. That includes most other mREITs and even the S&P 500 itself.

The company’s performance is driven by the firm’s two primary competitive advantages. First is the management team, which has proven itself to be among the best at adapting to changing conditions in each of Annaly’s individual business segments.

The other major competitive advantage is the firm’s enormous scale, including a market cap that’s about 25 times larger than its median peer. Remember that mREITs need to frequently issue new stock to grow their assets over time. Thus, the bigger an mREIT is, the more capital it can raise at once to invest opportunistically.

Since Annaly is the largest mREIT in the country by far, the company’s expenses as a percentage of assets and equity are 65% and 53% below the industry average, respectively. In addition, its operating costs as a percentage of earnings are just 16% compared to 25% for most of its peers.

To maximize its scale, the company occasionally makes very large acquisitions, mostly funded by issuing new shares. This includes the $1.5 billion all-stock purchase of mREIT Hatteras Financial in 2016, which gave Annaly more exposure to investments that benefit from higher rates (variable rate-linked assets).

In May 2018, Annaly announced the $900 million all-stock purchase of mREIT MTGE Investment Corp. MTGE’s portfolio is primarily agency-backed residential assets. However, it also has a small portfolio of triple net lease healthcare properties that generate stable, long-term contracted, and high-margin rent.

In other words, in addition to diversifying into every corner of the mREIT industry (as well as middle market lending, becoming a BDC), Annaly is now diversifying into actual real estate properties as well.

Once the merger closes at the end of the year, Annaly will stand a colossus in the industry, with an average market cap 25 times its median rival and nearly double that of American Capital Agency (AGNC), the second largest mREIT in America.

As a result, Annaly should have an even greater ability to obtain the lowest possible cost financing and continue consolidating smaller mREITs, as well as diversify its business model over time. The end goal is not so much to grow EPS (which pays the dividend) over time, but stabilize cash flow and make it less variable.

If Annaly can do that, then it could potentially become a source of stable and secure income for investors. However, keep in mind that Annaly is going to face major challenges in the future in achieving that goal. As a result, like all mREITs, the company remains a high-risk stock not suitable for conservative income investors.

Key Risks

First, it can’t be stressed enough how different the mREIT industry is from equity REITs. Equity REITs own permanent income-producing assets that create stable (contracted) cash flow over time to support generous and growing dividends over time. In contrast, mREITs own financial assets that eventually roll off, and their cash flow is incredibly volatile and wildly sensitive to interest rates, creating very variable dividends.

While Annaly has proven to a be a decent buy-and-hold investment over both the last five years (and since its IPO in 1997), along the way shareholders have had to deal with incredibly price declines including:

- 2005: -44%

- 2008: -47%

- 2012 to 2016: -54%

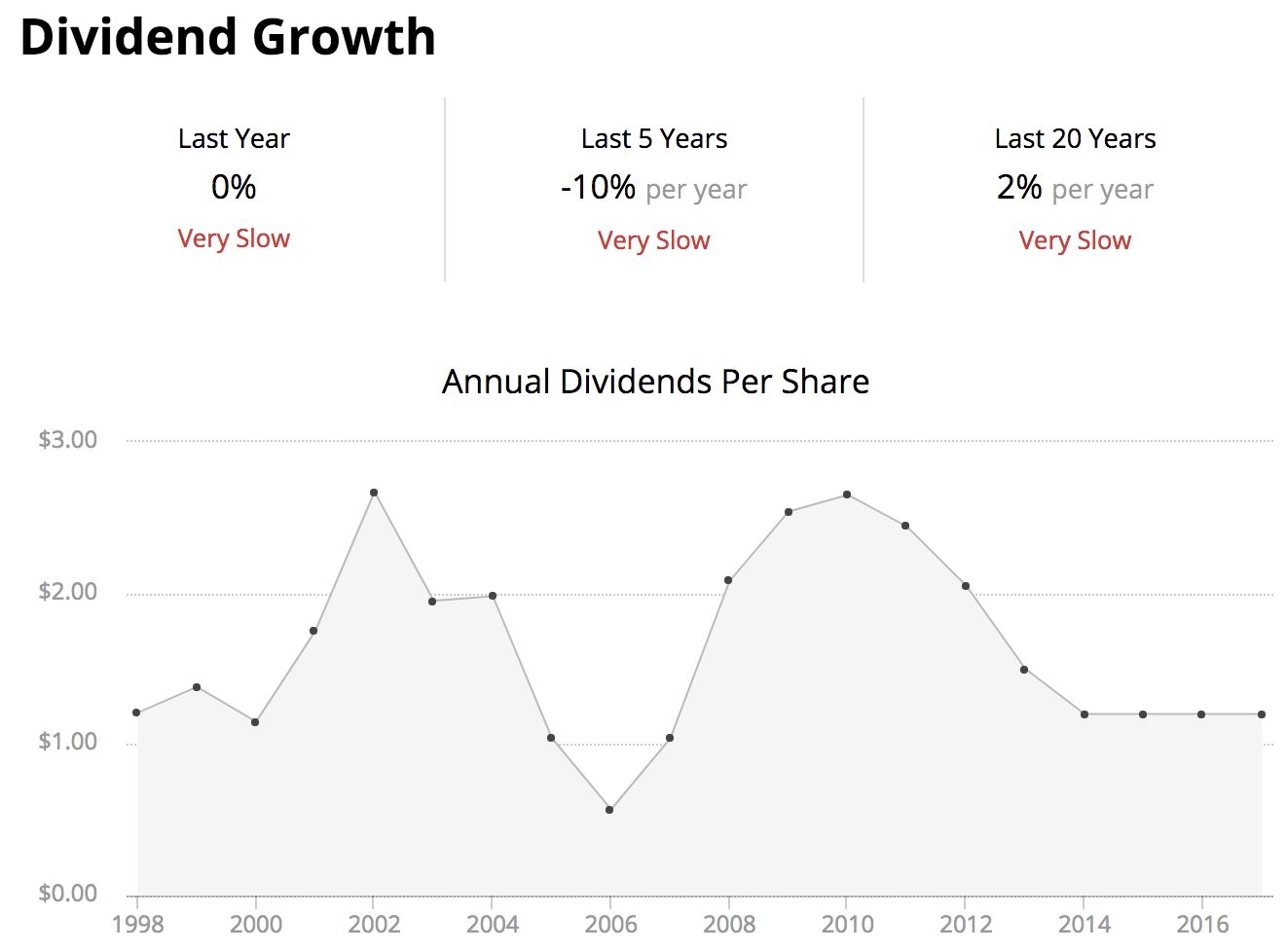

Annaly’s dividend has fluctuated somewhat wildly as well, with its dividend actually declining by 10% per year over the last five years. The substantial financial leverage used by Annaly to boost its portfolio’s returns adds more risk to the company’s cash flows and dividend, especially given the company’s high payout ratio.

Another big difference between mREITs like Annaly and equity REITs is the management structure. Almost all traditional REITs are internally managed, meaning management works directly for shareholders and draws traditional compensation packages (salary and stock options). This aligns the interests of management with regular investors because executives end up having a large stake in seeing growth occur on a per share basis (cash flow per share, dividends per share, share price).

In contrast, almost all mREITs, including Annaly, are externally managed. This means that management doesn’t work for shareholders directly but is outsourced to a third-party asset manager; in this case, Annaly Capital Asset Management LLC. External managers normally get paid two fees, a base management fee (based on total assets), and an incentive fee (usually about 2% of growth in earnings).

In other words, externally managed REITs are like hedge funds where management usually gets paid “2% and 20%” fees, which can create high conflicts of interest. This is because the management pay is not based on a per share metric, like NAV per share (also called book value) or EPS, but on absolute size. In other words, if the mREIT simply doubles its assets, management gets double the base management fee, even if EPS and dividends per share end up falling over time.

The good news is that Annaly, while externally managed, is among the most shareholder-friendly companies in its industry. That’s because management only receives a relatively modest 1.05% asset management fee and no incentive fees. This not only lowers its incentives to grow unprofitably (such as with highly dilutive equity-funded acquisitions), but it also lowers the mREIT’s overall cost structure.

For example, Annaly’s operating expenses as a percentage of assets is just 0.24%. That’s nearly three times lower than its peers and much lower than the few internally managed mREITS like tiny Ladder Capital (LADR), which lacks Annaly’s economies of scale. However, just be aware that Annaly’s externally managed structure still creates larger conflicts of interest than regular REITs.

In addition, Annaly’s ability to grow profitably is severely constrained by its business model.

Specifically, most mREITs, due to their cyclical business models, trade at close to book value. This means that raising equity capital to invest profitably (meaning EPS grows over time) is very challenging for all mREITs, even Annaly. This is especially true in today’s interest rate environment where the Federal Reserve is hiking short-term rates (raising Annaly’s borrowing costs), and long-term rates are rising more slowly or remaining flat.

Remember that the yield curve (difference between short and long-term interest rates) is ultimately what drives mREIT profitability. The yield curve has been falling since early 2014 and is now at 0.34%, the lowest point in 11 years.

The Federal Reserve has stated that its tentative plan is to raise short-term rates another six times through the end of 2020. As a result, the yield curve could become even more compressed or even invert if short-term rates move higher than long-term ones.

In that situation, Annaly’s ability to invest profitably would drop dramatically, and many financial companies could even start losing money on new loans. In addition, the last nine recessions (since 1928) have all been preceded by a yield curve inversion (usually by 12 to 18 months).

This means that not only is Anally’s core business seeing continued margin pressure right now, but that trend could continue for the rest of the economic cycle (until the next recession starts). And when the next recession starts, then Annaly’s share price is likely to take a hit due to the bear market that accompanies economic downturns.

In fact, even factoring in all the benefits that Annaly enjoys in terms of economies of scale and diversifying its cash flow stream, analysts expect the firm’s EPS growth rate to be only about 1% over the next decade. This is typical for even the largest and best run mREITS owing to their inability to acquire permanent assets producing stable income, funded with low cost equity.

Closing Thoughts on Annaly Capital Management

Annaly Capital Management is the largest and arguably best run mREIT. The company’s management team has shown an ability to adapt to changing industry conditions, achieve the best economies of scale, and embrace one of the most shareholder-friendly management fee agreements to lower its cost structure and boost profitability.

However, at the end of the day Annaly is merely one of the better houses in a dangerous neighborhood. The underlying business model makes it virtually impossible to sustain dividends over a full economic cycle, much less grow them consistently.

Therefore, Annaly, like virtually all mREITs, is a high-risk dividend stock that is unsuitable for most dividend investors, especially those in need of highly consistent income.

Leave A Comment