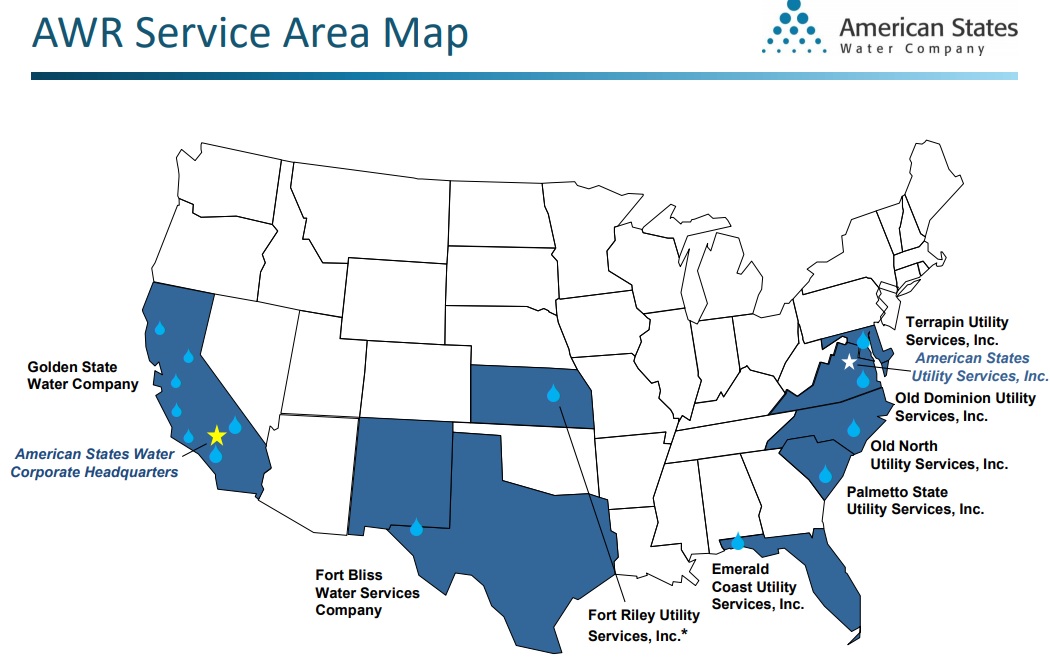

Founded in 1929, American States Water (AWR) is a regional regulated water and electrical utility serving 75 communities in Northern, Coastal, and Southern California. It also serves 24,000 electrical customers in San Bernardino county.

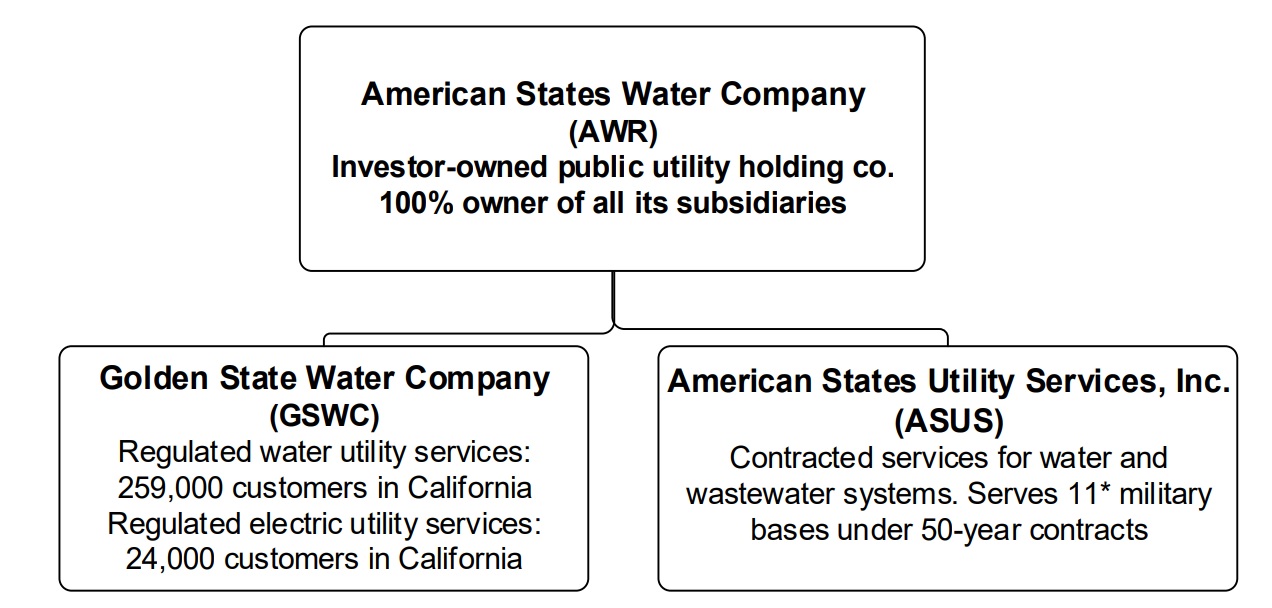

The company has two major segments. The Golden State Water Company owns the firm’s regulated water and electric assets, and American States Utility Services operates privatized water systems on 11 military bases under 50-year contracts. This includes the four largest military bases in the US: Fort Bragg, Fort Bliss, Eglin Air Force Base, and Fort Riley.

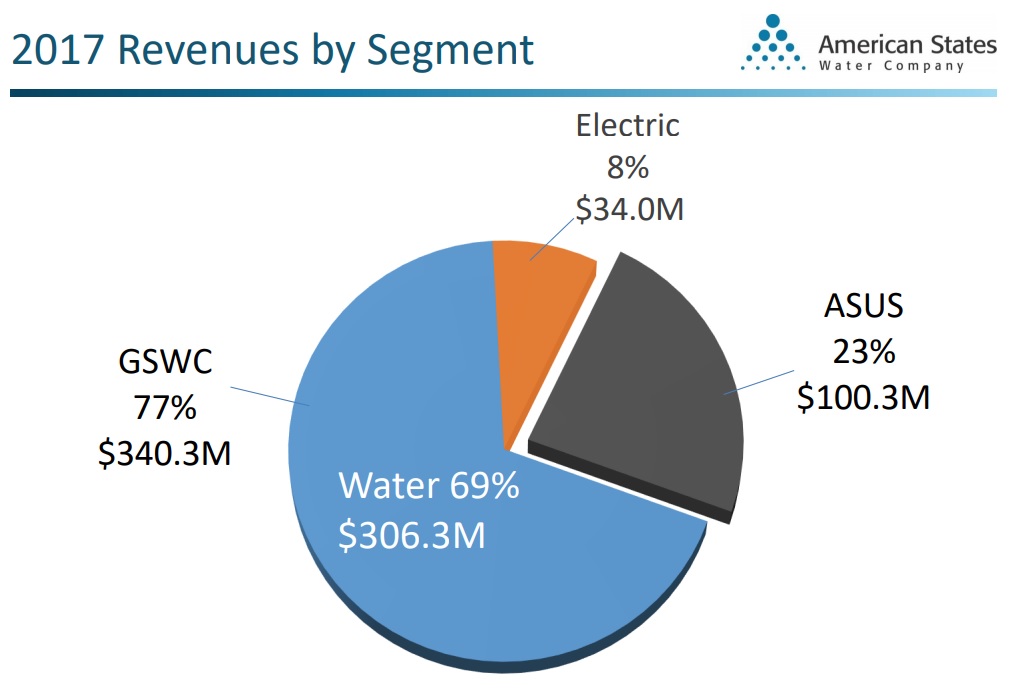

In 2017, approximately 77% of the company’s revenue came from its regulated utilities operations (69% from water), with the remaining 23% coming from American States Utility Services (ASUS). 90% of water revenue is derived from commercial and residential users.

Business Analysis

Regulated utilities have historically been a dependable source of generous and moderately growing dividends. That’s because they are essentially government-sanctioned monopolies in which a company enjoys no competition in its service territories in exchange for regulators setting prices and maximum allowed returns on equity and base rates. Due to the highly capital intensive nature of building and maintaining water systems, it makes little sense for competing firms to duplicate such systems within an area, which only has so many customers.

Thanks to the highly recurring and recession-resistant nature of its cash flow, American States Water boasts arguably the most impressive dividend growth record of any U.S. company. The utility has paid uninterrupted dividends since 1931 and has increased its dividend for 63 straight years, making it a dividend king.

American States Water benefits from a highly experienced management team with over 100 years of total industry experience. That includes dealing with challenges like droughts, handling various changes in regulatory regimes, and getting large-scale infrastructure projects approved and recouped quickly.

The company’s experience has helped it continue growing its earnings despite slightly negative sales growth over the last few years caused by the worst drought in decades in its core market of California. That, in turn, has translated into impressive 10% annual dividend growth over the last six years.

The key to AWR’s success has been the utility’s impressive ability to generate large economies of scale despite its relatively small size. This is accomplished by growing revenues faster than costs, via increases in rate base and its utility service contracts with minimal staff expansion. As this happens, the company amortizes its fixed costs over a great revenue base, boosting margins and returns on capital over time.

Besides its impressive track record, American States Water is a rather unique utility given its operations across 11 major military bases. This segment of the company is led by James Cotton who was with the Department of Defense for 15 years and has numerous valuable contacts in the Pentagon to help win further military base privatization contracts.

The utility service segment is the company’s best long-term growth prospect. It provides a high margin source of recurring revenue and growth opportunities while diversifying American States Water away from its high dependency on just one state.

American States Utility Services has recently won two important contracts:

- April 2017: Eglin Air Force Base: $702 million, 50-year contract

- September 2017: Fort Riley: $601 million, 50-year contract

These two contracts alone are worth $26 million per year in inflation-indexed revenue. That’s a 6% boost to revenue, which is an impressive feat in this slow-growing industry. And in terms of EPS growth, management predicts that each such contract boosts the firm’s EPS growth rate by about 2%.

In the next five years, numerous military bases are expected to privatize their water systems, and American States Water Company believes that it is one of the best positioned companies to win these lucrative 50-year contracts.

However, there are three primary components to the company’s long-term growth plans. First, AWR plans to continue making accretive acquisitions to consolidate the industry. This means small bolt-on acquisitions of other California-based municipal water systems.

The second growth catalyst is rate base increases by investing in improvements in its existing assets (if approved by regulators). In 2018, American States Water plans to invest $115 million in capex which represents 26% of its 2017 revenue. Over the long term, the company believes that upgrading its aging infrastructure (most built between the 1950’s to 1970’s) will allow it to invest in growth at three times the rate of depreciation of its assets. That, in turn, means a steadily growing rate base that should translate into slow but steady EPS growth.

Finally, the American States Utility Services segment’s continued success in obtaining new military base contracts represents a competitive advantage that few other water utilities have. That’s because each contract obtained represents roughly 2% growth in sales and earnings per share.

Meanwhile, its good track record of running military water systems for decades means that American States Water is a trusted Department of Defense partner that’s usually at the top of the list for winning new privatization contracts. While the utility services business is about three times smaller than the regulated segment, the rate of growth in this segment is expected to drive about 33% to 40% of management’s long-term 5+% EPS growth forecast.

And given the company’s safe payout ratio near 60%, if American States Water Company is able to achieve this growth rate, then it should be able to grow the dividend at 5% to 6% per year over time.

As a result, American States Water Company has the potential to be a decent low risk source of steady dividend growth for years to come. However, there are several negative factors that mean AWR might not be as good of a choice as its rivals American Water Works (AWK) and Aqua America (WTR).

Key Risks

There are several risks facing American States Water Company. The biggest issue is the highly concentrated nature of its core water business, which is located in mostly rural and suburban California.

While management has over a century of collective experience in the water utility business, all of it is with California regulators. This makes diversifying into other states more difficult. This is a problem not shared by industry leader Aqua America (operates in seven states) and American Water Works (16 states and Canada). A more diversified operating area makes it easier for its larger rivals to continue adding new customers over time.

Another risk is the highly regulated nature of its California water business, which involves dealing with numerous regulatory agencies including:

- California Department of Conservation

- Integrated Waste Management Board

- The California EPA

- Department of Water Resources

- The California Public Utilities Commission

These appointed regulators must approve the company’s investment plans and determine what kind of returns on capital it earns in its water business. Specifically, regulators can decide to lower the allowable returns on equity and rate base the company enjoys. In April 2017, the company filed a cost of capital request with the California Public Utilities Commission for a return on equity of 11% and a weighted return on base rate (what customers pay) of 9.1%

On February 6, 2018, the California Public Utilities Commission authorized a return on equity and return on base rate of 8.2% and 7.4%, respectively (retroactive to the start of 2018). That return on equity is lower than the previous 9.4% level, and the return on base rate also dropped from its previous amount of 8.3%. Management expects this development to reduce revenues by $9.5 million per year, or 2.2% per year going forward. That offsets almost 40% of the company’s new military base service contract revenue.

That might not sound like much, but remember that the water utility business is inherently slow growing. And thanks to years of drought, American States Water Company has been struggling to achieve any revenue growth at all (-1.2% annual revenue growth over the last five years).

And since American States’s water segment is purely focused on California, it lacks the regulatory risk diversification enjoyed by American Water Works and Aqua America where a single negative regulatory outcome impacts their top and bottom lines far less.

Geographical concentration also poses other risks. For example, while the California drought may be over (for now), Governor Jerry Brown signed two bills into law on May 31, 2018, to make the water conservation rules of the last few years permanent.

Specifically, the new law orders the States Water Resource Board to work with regional and local utility commissions to maintain the current 55 gallon per person per day limit. That will be reduced to 50 gallons per day by 2030. Such restrictions, combined with the company’s naturally slow growth nature in obtaining new customers, could make it much harder for management to achieve its 5% annual long-term dividend growth target.

Another potential growth headwind is that local cities sometimes attempt to take over the company’s water assets. For instance, in 2017 the company settled with the Casitas Municipal Water District for $34.5 million over an eminent domain case. The city would take over the 2,900 connection Ojai water system which American States has been operating since its founding in 1929. Claremont, California, similarly attempted to take over its city’s water system, though the company has successfully blocked the attempt, including the city’s appeals.

Regardless, remember that the nature of the water utility industry is that growth is predicated on numerous small acquisitions to consolidate municipal water systems. This means that any growth in customers is very slow, and losing even a single eminent domain case as is did with Casitas can undo several years worth of growth through acquisitions.

Next, be aware that while American States Water Company has a strong balance sheet, including an A+ credit rating from Standard & Poor’s, it also faces some problems. For one thing, 28% of its debt has variable interest rates, which have pushed the utility’s borrowing costs up to nearly 6%. The relatively high borrowing costs, combined with its small market cap (about $2 billion), means that American States Water Company must dilute investors via selling new shares to fund its growth plans.

Now that’s not inherently bad, since it is standard practice for nearly all regulated utilities to issue equity. However, be aware that American States Water Company has been enjoying strong stock appreciation in the past year, allowing it to sell new shares to raise equity growth capital at highly attractive rates.

Should the utility’s stock price decline and interest rates rise, American States Water Company’s cost of capital would increase. The firm’s low cost of equity capital today is also a bit of a double-edged sword for income investors because it means that the utility has one of the lowest dividend yields in the industry.

Not only do its larger and more diversified water utilities offer slightly higher yields, but analysts expect Aqua America (a firm with 25 years of consecutive dividend increases) to grow as fast as American States Water Company (5% annual EPS growth over next decade). Meanwhile, American Water Works is expected to grow much faster at about 8% per year. When combined with their greater diversification, those stocks may be more appealing for most dividend investors.

Closing Thoughts on American States Water Company

Regulated water utilities can be a great source of low risk and steady income growth thanks to their wide moats and recession-resistant revenue streams. American States Water Company has an exceptional track record of strong capital allocation thanks to its experienced and conservative management team. This has resulted in the longest consecutive annual dividend growth streak of any U.S. corporation.

That being said, while the utility service segment offers strong long-term growth and diversification potential, the company’s core California water business seems likely to experience both slower growth and lower profitability going forward. Investors looking to gain exposure to the water utility industry might want to consider larger, more diversified, and faster growing rivals like American Water Works or Aqua America instead.

To learn more about AWR’s dividend safety and growth profile, please click here.

Leave A Comment