Founded in 1940, Air Products and Chemicals (APD) is one of the world’s largest providers of atmospheric gases (oxygen, nitrogen, argon, and rare gases), as well as process and specialty gases (hydrogen, helium, carbon dioxide, carbon monoxide, syngas). The company sells to over 170,000 clients operating in more than 30 industries around the world. To produce and supply its gases to customers, Air Products’ employees operate over 750 manufacturing facilities, a fleet of delivery trucks, and 1,800 miles of industrial gas pipelines.

Air Products is one of those classic, boring industrial giants providing essential elements like liquid oxygen, nitrogen, argon, hydrogen, helium, carbon dioxide, and carbon monoxide to companies that use them in the manufacturing of: metals, glass, chemical processing, electronics, energy production and refining, food processing, medical applications, and general manufacturing.

The company sells its products via three kinds of contracts:

- Liquid bulk: bulk deliveries by tanker in a liquid state. Most contracts are three to five years.

- Packaged gas: smaller truckload deliveries (mostly cylinders filled with helium) primarily for electronics and MRI industries.

- On-site gas supply: large quantities of hydrogen, nitrogen, oxygen, carbon monoxide, and syngas (a mixture of hydrogen and carbon monoxide) are provided to customers, principally the energy production and refining, chemical, and metals industries worldwide. These customers require large volumes of gases that have relatively constant demand. Gases are produced at Air Products’ large facilities located adjacent to customers’ facilities or by pipeline systems from centrally located production facilities and are generally governed by 15- to 20-year contracts.

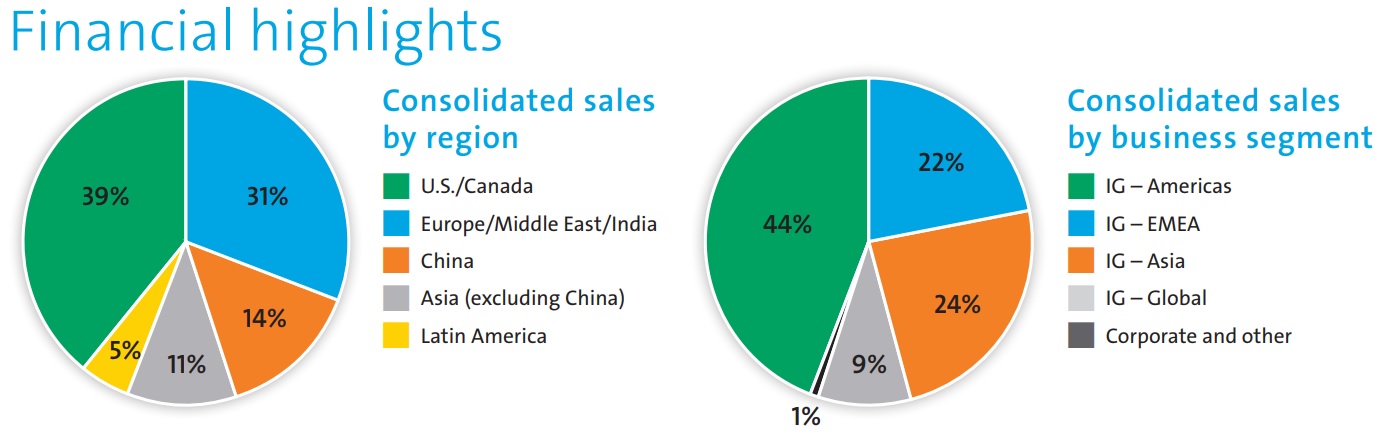

Air Products is highly diversified geographically, with a strong presence in not just North America and Europe, but also fast-growing emerging markets in Asia and Latin America.

The company is also well-diversified by client with no single customer representing more than 10% of revenue.

With 35 consecutive years of annual dividend increases, Air Products is a dividend aristocrat.

Business Analysis

Industrial companies are known for being capital intensive and having volatile sales, earnings, and cash flow. So how is it that Air Products has been able to achieve 35 straight years of safe and fast dividend growth? That lies in its competitive advantages.

The industrial gas industry is highly commoditized, since the actual gases themselves are all the same. However, creating and transporting those gases requires a lot of technical expertise and complex industrial equipment (cryogenic storage and specialized tanker trucks). For instance, Air Products has 532 U.S. patents and 2,544 foreign patents, mostly related to its on-site gas production systems.

Another benefit to Air Products is that gases are hard to store properly, requiring advanced cryogenic tankers and storage facilities. They can also be shipped via highly insulated short-term pipelines which are usually built around centralized gas generation facilities. A new gas facility can cost $2 billion to $3 billion and take several years to construct, assuming all technical regulations are complied with.

In addition, while the gas itself is usually low cost (air is a very cheap raw material), transporting and storing it is far more complex and expensive (liquid oxygen put in a tanker will evaporate after 200 miles). That’s because it requires advanced infrastructure such as cryogenic gas storage equipment, large pipeline networks, and vast fleets of specialized tanker trucks.

These substantial costs mean that smaller rivals can’t compete well on price because customers ultimately care more about reliable delivery of gases from sizable distribution networks that only large players can provide.

The high transportation costs also make industrial gas a local business, with competition typically limited to a radius no greater than a couple hundred miles. When combined with Air Products’ long-term contracts and relationships with many customers, new entrants have a hard time taking market share.

Ultimately, Air Products benefits from the fact that industrial gas is a capital intensive and highly regional business. Due to the high capital costs and need to build out large production and distribution networks, the industry’s four largest players command 80% to 85% of the market share.

Air Products is the world’s largest supplier of hydrogen and helium with approximately 40% market share in those two critical gases in the U.S. and Canada. The company is especially strong in the refining industry where it is the world’s largest hydrogen supplier, including on the U.S. gulf coast where energy exports are booming. The firm also owns the only hydrogen pipeline system supplying Canada’s enormous tar sands region.

Another positive aspect to this business is that industrial gases are critical, non-discretionary inputs to Air Products’ clients, who need a reliable and scalable supply in order to function. As a result, Air Products is able to leverage its reputation for industry leading safety and reliability into very long-term (up to 20-year) supply contracts that create a relatively steady source of cash flow.

Since gas typically accounts for just a small portion of a customer’s total manufacturing costs and is an essential expense, Air Products is able to enjoy some pricing power as well. Thanks to these advantages, as well as its strong economies of scale, Air Products boasts a 21% operating margin and generates excellent free cash flow it uses to pay safe and growing dividends.

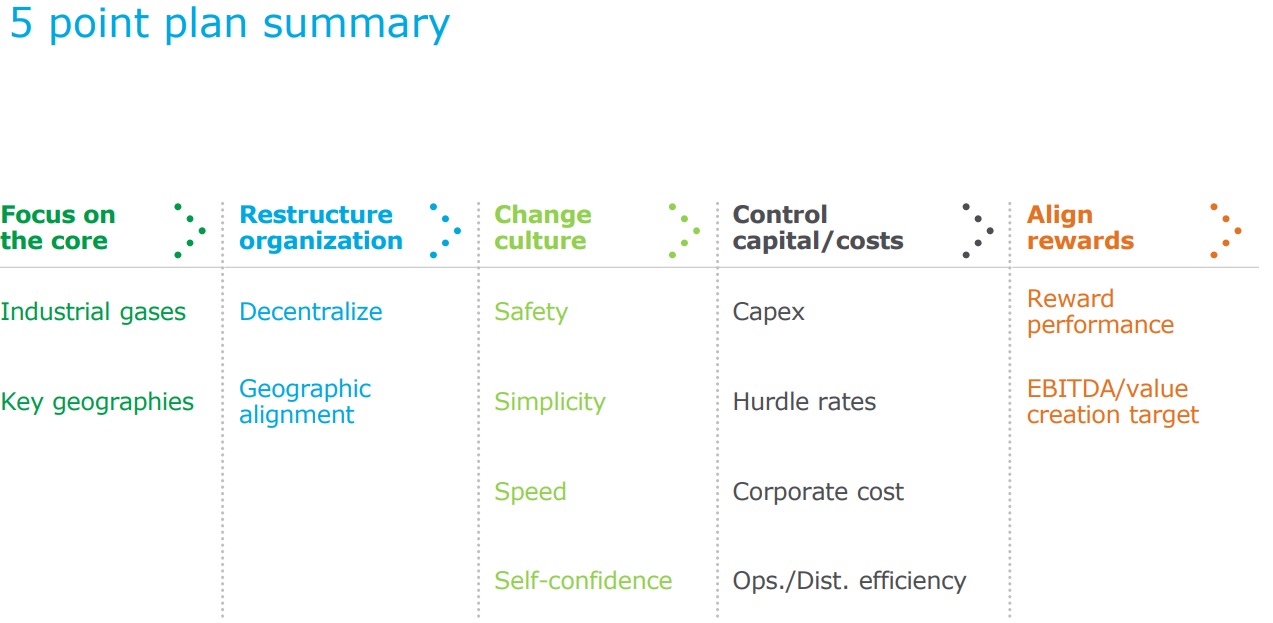

Air Products’ solid profitability is a testament to the company’s ability to adapt over time. One example is the corporate restructuring the company undertook in 2014. This was the largest restructuring in Air Products’ history and had five goals:

- Be the safest industrial company in the world

- Become the most profitable company in the industry

- Divest non-core (slow growth, low margin) businesses

- Achieve the strongest balance sheet in the industry

- Achieve long-term 10% EPS and FCF per share growth

Over the past four years, management has used advanced data analysis to greatly improve the cost effectiveness of its operation (boost EBITDA margin by 9%), while cutting the employee injury rate by 83%. Management also refocused the company by selling non-core assets, including the lower margin performance materials business which was divested for a healthy 15.8 times EBITDA multiple. In addition, Air Products spun off its electronics materials business into Versum Materials (VSM) in 2016.

In total, these two divestitures gave the company about $3.8 billion and allowed Air Products to lower its net debt from $5.8 billion in 2015 to just under $400 million today. Air Products maintains an excellent balance sheet, as demonstrated by the company’s A credit rating from Standard & Poor’s.

A strong balance sheet helps not only maintain better dividend safety, but it also provides management with more financial flexibility to invest and grow the business. For instance, management estimates that the firm has current liquidity (cash plus borrowing power) of about $7 billion right now and expects that to rise to roughly $10 billion by 2020. Air Products is using its large financial flexibility to invest in growth around the world.

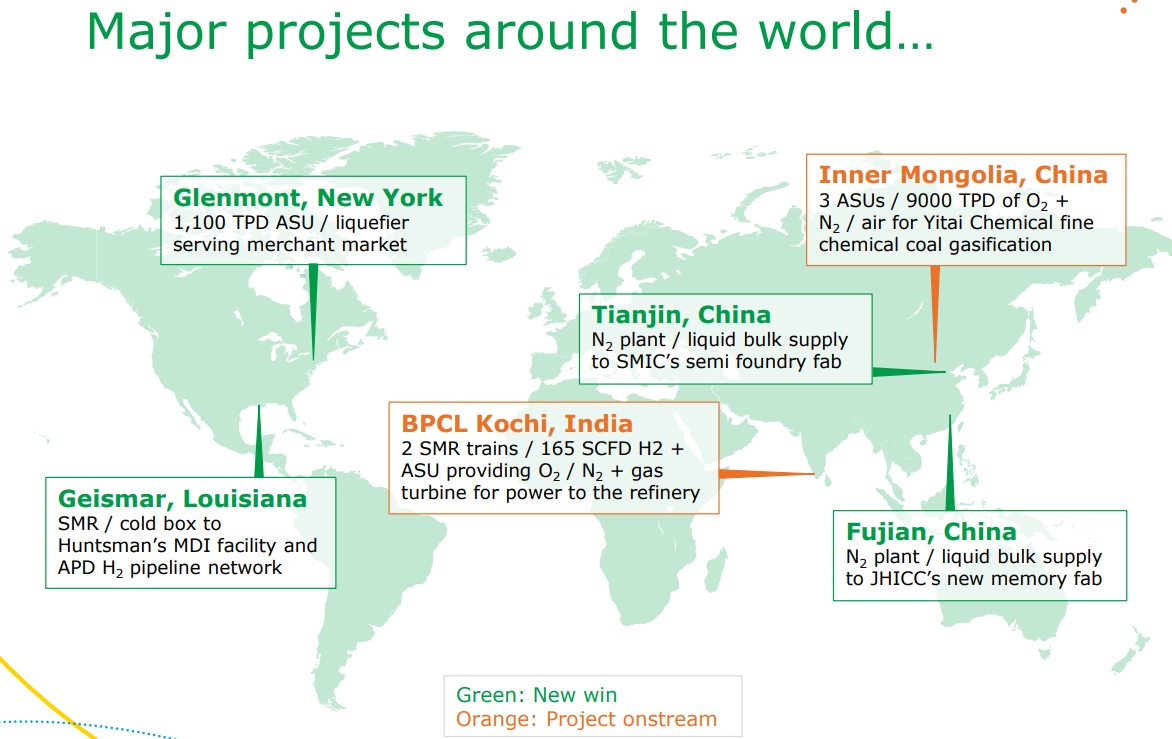

One of its notable projects is a $1.3 billion investment in a Chinese coal-to-gas joint venture with chemical company Lu’An. Air Products just completed this deal and owns 60% of the project. Lu’An will supply the on-site gas delivery project with coal, steam, and power. In exchange, it will gain critical industrial gases generated on-site under a 20-year contract. Now that the Lu’An project is complete, Air Products has about $1.5 billion in ongoing new construction that’s underway and will be finished in the next few years.

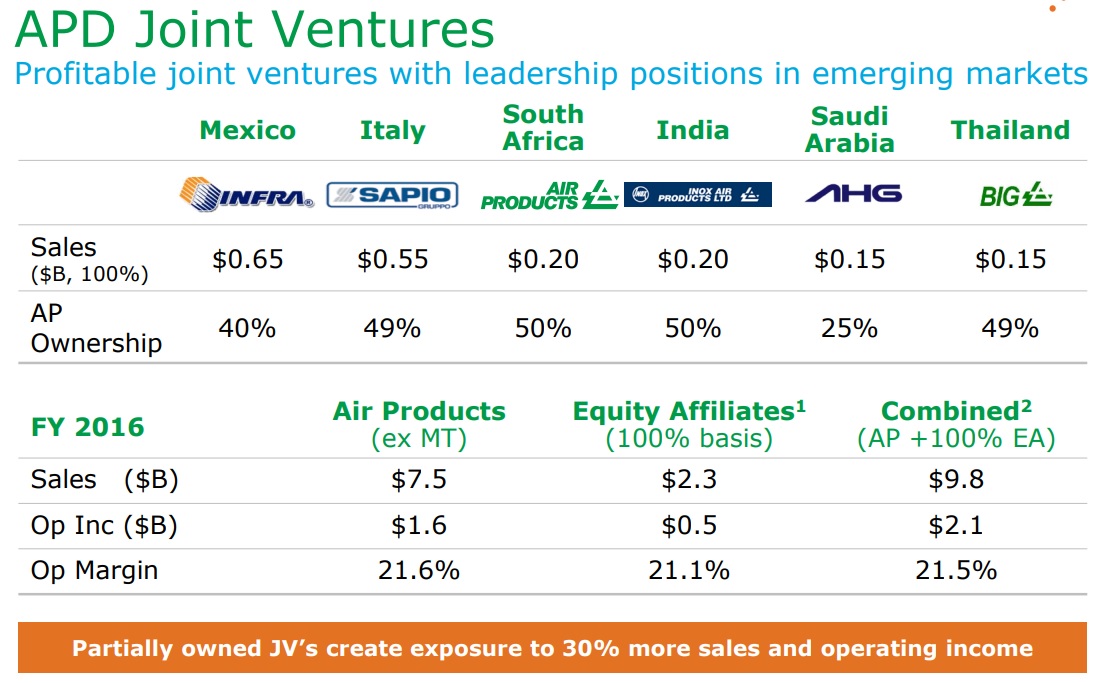

Air Products often uses joint ventures to grow internationally because its partners bring local regulatory and market expertise.

In total, Air Products expects to spend about $8 billion on growth projects over the next three years by pursuing three strategies. First, the company wants to buy small to medium-sized companies to consolidate its industry and improve its economies of scale. Second, it wants to purchase existing industrial gas assets from its customers, including joint venture partners. Finally, the firm wants to continue growing organically by building new gas generation and distribution assets all over the world.

Management is being highly disciplined with its investment approach, and any investment of more than $3 million must be approved by the CFO and CEO. The company only proceeds if management believes it can achieve double-digit returns on invested capital.

Over the long term, management’s goal is to deliver at least 10% annual growth in EPS. The company’s forecast seems somewhat reasonable since Air Products has a good track record of hitting its earnings growth target following its restructuring:

- 2015 EPS growth: 10%

- 2016 EPS growth: 16%

- 2017 EPS growth: 10%

- 2018 EPS growth: 15% to 17% (guidance)

If everything goes as planned, Air Products should be able to deliver double-digit dividend growth over the long term, which would be in line with its 20-year average annual payout growth rate of 10%. That being said, while Air Products is certainly one of the faster growing dividend aristocrats, there are still some major risk factors investors need to keep in mind.

Key Risks

Management has indicated that it is looking to be far more aggressive on the M&A front in the coming years. That creates high execution risk because historically Air Products hasn’t been known for large-scale mergers. For example, goodwill, the premium paid for acquisitions, makes up just 4% of the firm’s assets. In contrast, many industrial companies have goodwill-to-assets ratios of 50% or higher, indicating they are far more experienced with growing through large acquisitions.

That’s not to say that Air Products hasn’t tried to make large deals in the past. Over a decade ago the company tried to acquire a major global rival (BOC) via a joint venture with Air Liquide. But that deal fell apart and another major rival, Linde, ended up acquiring BOC.

Air Products also attempted to buy Airgas in 2011 but was unable to close the deal, resulting in Air Liquide snapping up that major player in a $22 billion mega merger in 2016. Then, in 2017, Praxair (PX) and Linde announced the industry’s largest-ever deal, a $73 billion merger that created the industry’s biggest player.

The merger has yet to close (it was announced in June 2017,) and antitrust regulators are likely to require significant asset divestitures that Air Products might be able to pick up.

The only major acquisition that Air Products has closed in the past decade was its 2012 purchase of Chilean gas giant Indura for $884 million. However, just two years later, due to poor execution and integration, Air Products had to take a major write-down on the acquisition which it judged a failure.

Air Products will have to be very careful that it doesn’t allow its large financial flexibility to go to its head and result in overpaying for future acquisitions. While such deals can result in good cost synergies over time, often combining different corporate cultures and production/logistics chains can be tricky.

The good news is that Air Products plans to be far more disciplined with its acquisitions in the future and avoid giant deals which are far harder to pull off well. However, even if Air Products avoids the costly mistakes of the past, investors still need to be aware that the firm’s sales and earnings remain highly volatile, tied largely to the health of the economy (historically the industrial gas industry grows at 1.2 to 1.4 times the rate of the global economy) and the energy sector.

Margins can also be volatile any given quarter due to fluctuations in the company’s two major inputs, natural gas and electricity. Another short-term risk to keep in mind is that Air Products has become more globally diverse, with 61% of current revenue coming from outside the U.S. As a result, the company’s reported growth rates can be affected by fluctuations in foreign currency exchange rates. However, these risks are unlikely to impact the firm’s long-term profitability.

Closing Thoughts on Air Products and Chemicals

Air Products and Chemicals is one of the world’s largest suppliers of critical industrial gases, and the wide-moat nature of this industry has allowed the company to generate one of most impressive dividend growth records of any business.

Air Products offers several appealing qualities including: management’s disciplined investment strategy, one of the industry’s strongest balance sheets, and long growth runways in both North American energy and Asian industrial markets.

All things considered, Air Products seems likely to continue generating close to double-digit dividend growth, making this industrial aristocrat a reasonable choice for most income growth portfolios.

To learn more about Air Products’ dividend safety and growth profile, please click here.

Leave A Comment