Wells Fargo has been fighting a number of scandals that are impacting its fundamentals. Let’s take a look at how the bank’s turnaround efforts are going and what they mean for dividend investors.

More Scandals Continue To Surface

At this point, Wells Fargo has become well-known for its ever-growing list of scandals which include:

- An independent third-party review of the bank’s accounts revealed that the total number of unauthorized accounts opened was actually 3.5 million, 67% more than initially thought.

- The bank incorrectly charged 800,000 car loan customers for unnecessary insurance that, according to Wells Fargo, could have caused around 20,000 customers to default on their payments and have their vehicles repossessed.

- Wells Fargo Merchant services apparently overcharged thousands of small businesses for credit card processing due to “deceptive language” in its 63-page service contract.

- 110,000 customers were inappropriately charged “mortgage rate lock extension fees” for missing mortgage payments that were actually a result of Wells Fargo’s initiated payment processing delays.

- In October 2017, regulators fined Wells Fargo $3.4 million for recommending clients invest in volatility-linked hedge investments that were “highly likely to lose value over time.”

The original fake account scandal has now resulted in a $142 million class action lawsuit settlement being approved by a judge in June 2018. While the size of the legal settlement isn’t large compared to the bank’s overall profitability (over $20 billion in net profits), it has hurt Wells Fargo’s brand with retail customers.

Meanwhile, as a result of an exhaustive internal review, management has continued to uncover more examples of misconduct by its employees that harmed customers and its overall reputation, especially among higher end wealthy clientele.

These latest examples include overcharging wealth management clients by as much as $171 million for foreign exchange fees. As a result, and in anticipation of future fines by the government, Wells Fargo has set aside $285 million to cover total costs of this latest scandal.

The bank is also setting aside $114 million to rebate fiduciary and custody clients in its wealth management business. This is because over the past seven years the bank has determined its been charging “incorrect fees” to individuals with trust, estate and custodial accounts managed by Wells Fargo.

Due to these legal costs, profits at Wells Fargo’s wealth management division fell 37% in the second quarter of 2018. However, the bank did note that no long-term effect is expected to the wealth management division.

The company’s CFO, John Shrewsberry, told reporters that, “We’ve accounted for what we know so far but there’s likely to be a little more to do as the review continues.”

However, Shrewsberry also affirmed that he’s reasonably confident that the worst is behind the bank stating, “We’re pretty far along, or perhaps done, going business to business looking for areas to correct…At this point, I would be very surprised if anything else emerged.”

Disappointed shareholders are likely hoping the same thing, because while the scandal has not resulted in massive legal fees such as levied against mega banks post financial crisis (over $200 billion for Bank of America alone), the scandals and Fed-induced asset freeze do appear to be causing short-term growth headaches.

The Scandals are Impacting Wells Fargo’s Top And Bottom Line Growth

Most banks are enjoying strong growth in their top and bottom lines. For example, JPMorgan recently reported 13% growth in revenue and 18% growth in earnings per share. Wells Fargo, however, is facing some growth headwinds due to scandals affecting its core businesses.

For example, in its most recent quarter the bank reported:

- Average deposits down 1%

- Average loans down 2%

- Revenue down 3%

- Adjusted EPS flat

Fortunately, there is good news for the future of the company’s profitability. First, the bank’s net interest margin, a measure of lending profitability (average loan rate minus average deposit cost), rose 3 basis points to 2.93% in the second quarter. That’s impressive since rising short-term interest rates have pushed up the average interest Wells Fargo must pay on its deposits.

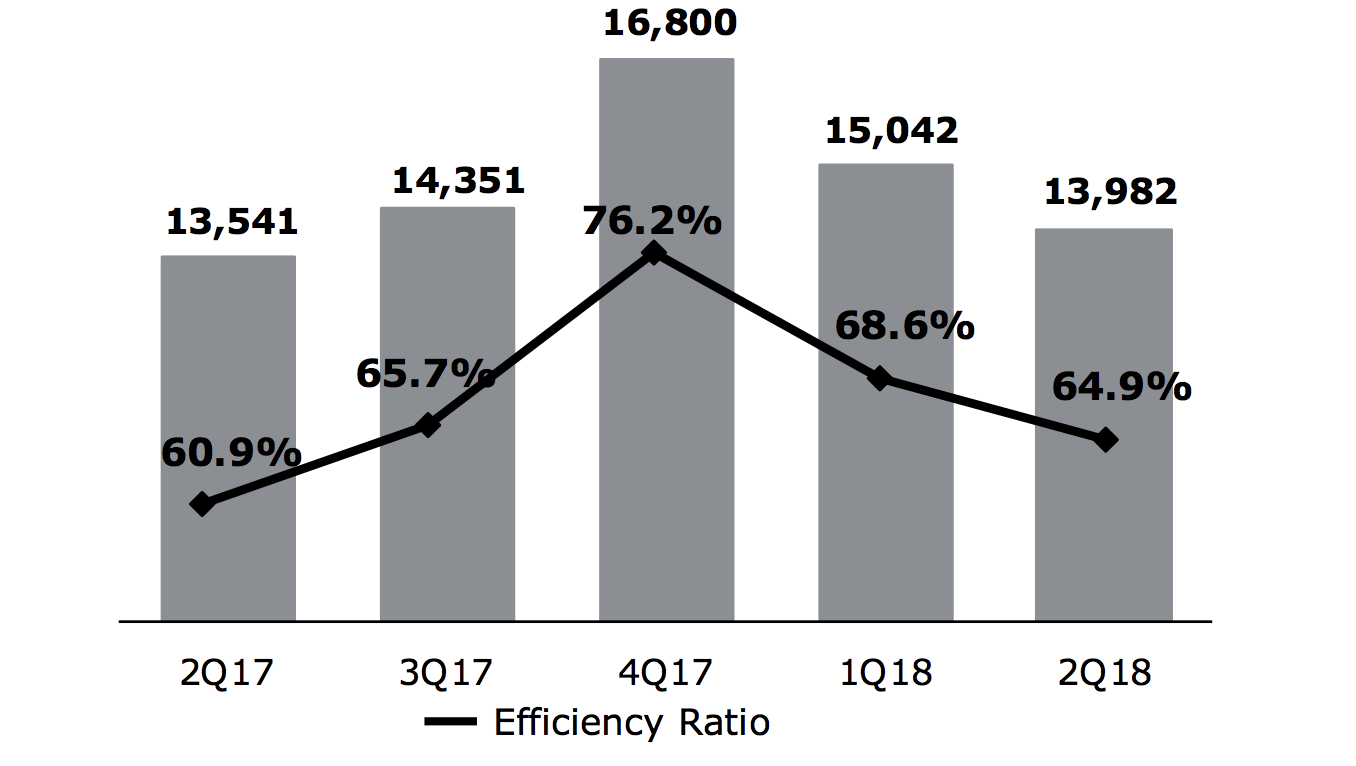

In addition, the company has made great headway on cutting costs. The bank’s efficiency ratio (non interest expenses/revenue) has been falling steadily as the legal costs of the scandals are starting to peter out. Management is also in the process of cutting $4 billion in annual expenses between 2018 and 2019.

Management expects costs to continue falling in 2020 thanks to continued strength in higher-margin mobile banking. All told, analysts expect that within five years Wells Fargo’s efficiency ratio could fall from about 65% today to 57%, greatly increasing the profitability of its core business.

And if management is correct that its internal control reforms are almost complete, then by September of 2018 the Federal Reserve could lift its asset growth restriction on the bank, unleashing stronger revenue and earnings growth in the future.

Good News Is The Dividend Is Safe And Growing

At the end of the day, while Wells Fargo’s flat revenue and earnings growth is a disappointment to investors, the dividend remains safe and growing. That’s because the bank remains extremely profitable and its balance sheet rock solid.

For example, in the 2018 Federal Reserve stress test, which simulates another global recession (far worse than 2008-2009 in fact), Wells Fargo passed with flying colors. More importantly, as part of its new stress test protocol the Federal Reserve lifted its previous soft cap on dividend payout ratios, which previous limited EPS payout ratios at around 35%.

As a result, America’s big banks have been allowed to massively increase their capital returns to investors over the next year, including strong dividend hikes:

- JPMorgan Chase (JPM): boosting dividend 43% and buying back $21 billion in stock over next year

- Citigroup (C): 41% dividend hike and $17.6 billion buyback

- Wells Fargo: 10% dividend hike and $24.5 billion in planned buybacks

While Wells Fargo’s dividend increase is disappointing compared to its faster growing peers, keep in mind that the stock’s new forward dividend yield near 3% is still generous compared to the S&P 500’s paltry 1.8% payout.

More importantly, that dividend represents a payout ratio near 40%, which is firmly in the safe range for large banks and indicates that Wells Fargo’s dividend is likely to continue grow. Potentially faster than earnings for the next few years as payout ratio could safely rise to about 50%.

Wells Fargo Remains A Hold

It’s understandable that Wells Fargo’s seemingly endless stream of scandals has caused many income investors to question the company’s long-term thesis.

After all, the bank’s self-induced crisis has now caused it to suffer from flat revenue and earnings growth during the strongest economy in nearly a decade, when other banks are enjoying record profits and much stronger top and bottom line growth.

That being said, Wells Fargo seems to deserve the benefit of the doubt, and the worst from the scandals is likely behind it. The cost of the scandals remains relatively small compared to the bank’s total profits, and its dividend and overall financial health remain on very solid ground (especially in light of the Fed’s latest stress test results).

I plan to continue holding our shares of Wells Fargo as the impact from the scandals hopefully fades over the years ahead.

I have a mortgage with Wells Fargo that will be paid off in less than a year. Doing business with such an ethically-challenged co. makes me feel dirty, and like an enabler. I have a close friend who works for Wells in their fraud division, and he has been telling me for years and years about how they’ve been trying to alert management to numerous problems like those mentioned in the article. But, sadly, apparently it was never taken to heart. Meanwhile, thank goodness I’ve resisted all attempts by Wells to sell me additional products they offer. I’m going to take particular pleasure in telling them why I won’t choose to do any more business with them, once my loan is paid. How we spend our $ is kinda/sort like voting, and I take “voting” seriously.