MMM makes it into our Top 20 Dividend Stocks list. The company is exceptionally managed and diversified across numerous profitable markets. The dividend is extremely secure and reliable with 10%+ growth potential going forward. With the stock selling off 10% over the past six months, now looks like a good time to consider MMM for long-term dividend growth investors.

Business Overview

3M is a diversified technology company that operates globally in five segments, each of which recorded mid-single digit organic sales growth in 2014. 3M is an extremely large company with over $30B in revenue and over 60% of sales coming from outside of the US. 3M’s segments cover nearly all end markets (from industrial adhesives to medical products to office supplies) and collectively produce more than 50,000 products. Each segment generates operating margins near 20% or above. 3M is one of more than 50 dividend aristocrats, having increased its dividend for over 25 consecutive years.

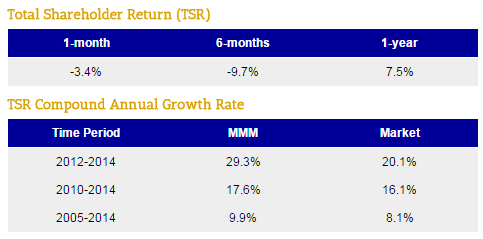

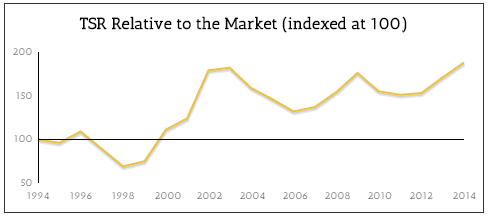

Stock Performance

MMM has created significant value for shareholders over time. As seen below, the stock has generally outperformed the market since the late 1990s and has been particularly strong over the last three years, compounding at a 29% rate compared to the market at 20%. MMM is a stock that has rewarded shareholders very nicely.

Dividend Analysis

We analyze 25+ years of dividend data and 10+ years of fundamental data to understand the safety and growth prospects of a dividend. MMM’s long-term dividend and fundamental data charts can all be seen here.

Dividend Safety Score

Our Safety Score answers the question, “Is the current dividend payment safe?” We look at factors such as current and historical EPS and FCF payout ratios, debt levels, free cash flow generation, industry cyclicality, ROIC trends, and more.

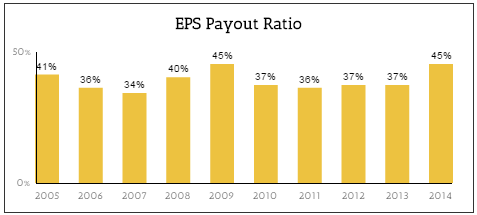

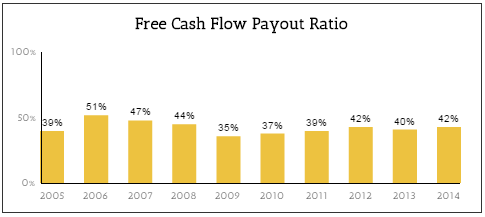

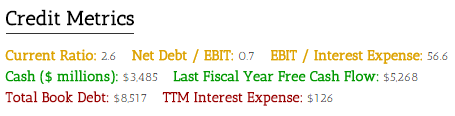

MMM scored an impressive Safety Score of 98, meaning its dividend is safer than 98% of all other dividend stocks. As seen below, MMM has maintained EPS and FCF payout ratios between 30-40% over the past decade, suggesting there is plenty of cushion to continue paying and growing the dividend, even in the event of an unexpected decline in the business.

The balance sheet is also very healthy, with MMM maintaining a net debt / EBIT ratio of 0.7. The company has also generated and meaningfully grown free cash flow and EPS each of the last 10 years. The dividend payment is about as rock solid as they come.

Dividend Growth Score

Our Growth Score answers the question, “How fast is the dividend likely to grow?” It considers many of the same fundamental factors as the Safety Score but places more weight on growth-centric metrics like sales and earnings growth and payout ratios.

MMM’s Growth Score came in at 91, meaning its dividend’s growth prospects are in the top 10% of the 2,700+ dividend stocks we monitor. We previously saw MMM’s healthy and steady payout ratios, which are even more impressive given the company’s strong dividend growth. As seen below, MMM has grown its dividend at a 9% annual clip over the past decade, with stronger growth in recent years.

Yield Score

Our Yield Score simply ranks a stock’s current dividend yield against all of the other dividend yields in the market. A score of 50 means the stock’s yield is right in the middle of the pack. A score of 100 means it has the highest yield.

MMM’s Yield Score is currently 55, placing it just slightly above the market average. Typically, companies with high quality dividends and growth prospects trade at greater premiums than that.

From a traditional multiple perspective, MMM trades at 19x FY15 EPS estimates and 17x FY16 EPS estimates. While not a bargain, the multiples are certainly very easy for MMM to grow into rather quickly.

Competitive Strengths

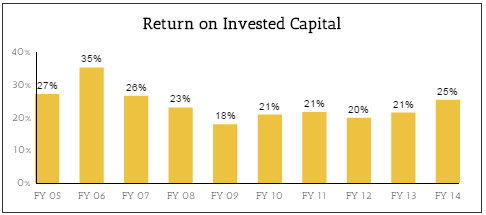

One of the quickest ways to assess the strength of a business model is to evaluate the level and durability of a company’s return on invested capital. As seen below, MMM has generally maintained a return on invested capital in excess of 20% for the past decade, suggesting a very durable business:

The company’s high returns are possible for several reasons. First, many of 3M’s products are economically very attractive because they represent a small cost of the total product or project the customer is working on but are often mission-critical to the outcome.

For example, 3M supplies structural adhesives to automotive manufacturers. 3M’s adhesives bond plastics and metals together and are must maintain their strength throughout the entire car’s life. The company’s brand, technology innovation, and favorable product dynamics (low portion of the car’s total cost) provide nice pricing power, and it’s simply not worth risking the reliability of a vehicle for the OEM to switch suppliers.

The high returns on invested capital go beyond product dynamics. 3M’s management team has implemented a culture that embraces Lean Six Sigma and actively manages the company’s 27 operating divisions based on their profitability and growth characteristics. If a division is underperforming, 3M will take action to bring its returns up to an appropriate level and is not afraid to shed weak assets.

Finally, a third part of 3M’s secret to high returns is its unique ability to leverage its R&D investments. 3M invests 5-6% of its sales into R&D each year and has developed over 45 fundamental technology platforms (and owns over 100,000 patents) that are critical to its operations. Almost all of 3M’s technologies are relevant across many end markets with slight tweaking.

From a growth perspective, it is hard to imagine MMM growing at rates much beyond global GDP due to its large size and well diversified operations. The company has increasingly penetrated international markets (55% of overall sales in 2014 vs 45% in 2009), but organic growth is likely to remain in the 2-6% range. Management will likely look at M&A to supplement the company’s modest organic growth rate (grew ~5% in 2014). Given the company’s strong track record, focus on portfolio management, and disciplined capital allocation, this is likely more of an opportunity than a risk.

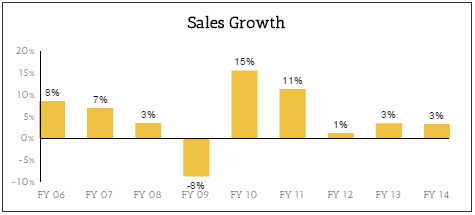

As seen below, MMM’s historical sales growth has averaged out in the mid-single digits. The company’s diversification and stable portfolio of strong brands helped it fare well during the recession, with sales down only 8% in FY09.

Key Risks

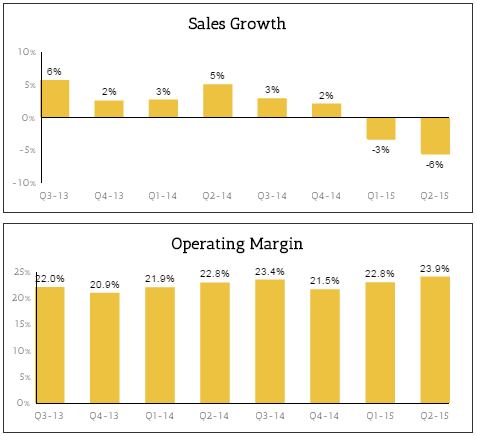

With so many of its sales taking place outside of the US, MMM is vulnerable to the strengthening dollar impacting its reported results. Indeed, unfavorable foreign exchange rates hurt reported sales by over 7% in Q2, but organic sales grew just under 2%.

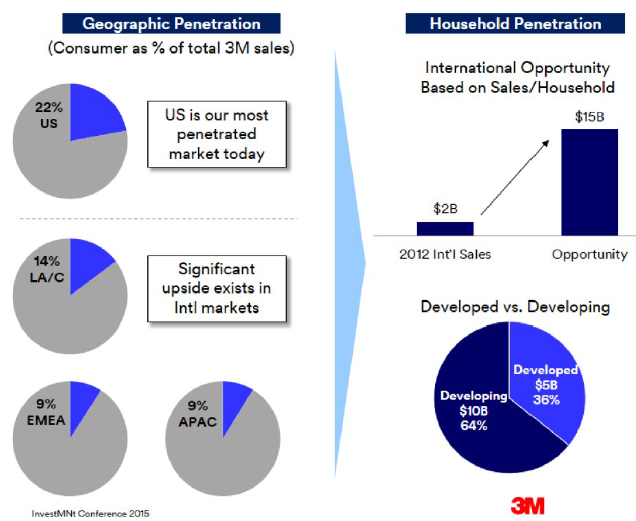

Ultimately, currency-related headwinds will eventually pass but could continue weighing on the stock in the near-term. Longer-term, it is a good thing that MMM is building large positions in international markets, which will support growth for a long time to come. As seen below, in MMM’s consumer segment alone, there is significant room to increase share internationally and capture more of a $15 billion opportunity.

Despite the headline softness in revenue, MMM is still growing earnings and expanding margins. Continued profitability improvements (operating margins rose 110 basis points in Q2) underscore the company’s strength:

Conclusion

For a long-term dividend growth investor, MMM should be viewed as a core holding. With dividend Safety and Growth Scores in excess of 90 and a Yield Score in line to slightly above the market’s average, you are getting a tremendous company at a fair price. In the near-term foreign exchange fluctuations and potential volatility in international markets could keep a lid on the stock, but they have no bearing on MMM’s strong competitive positioning and opportunity for long-term growth in international markets as conditions eventually normalize again.

I wish I can own shares in thee properous companies.