P&G is a core holding in our Conservative Retirees dividend portfolio because of its extremely safe dividend (88 Safety Score) and relatively attractive dividend yield (3.5% yield is in the 67th percentile of all current dividend yields). The stock was added to the Conservative Retiree portfolio, which was built to provide safe and predictable dividend income, on 7/1/15 at a price of $79.72 (the stock closed at $76.39 on 8/12/15).

Business Overview

P&G provides branded consumer packaged goods and generated $76 billion in sales last year across more than 180 countries. Its biggest brands are Pampers (13% of sales), Tide (6%), and Head & Shoulders (4%). In total, the company has over 20 billion-dollar plus brands.

P&G has been going through a transitional period that will see it exit about 100 non-core brands (60% of current brands), or approximately 15% of P&G’s total sales. These brands have been declining low single digits over the last three years with double-digit drops in pretax profit and margins that are 30% below the company’s average. In July, P&G announced an agreement to merge 43 of its beauty brands with Coty for $12.5 billion.

The remaining company will consist of 65 leading brands across 10 categories (#1 or #2 market positions in each category), a portfolio that will have higher growth and margins than the P&G we know today. The transformation will be complete by the end of P&G’s fiscal 2016 and will hopefully allow P&G to have greater focus on its strengths and top growth opportunities. As a result of its strategic actions, P&G also hopes to return $70 billion to shareholders over the next four years in the form of dividends and buybacks.

Stock Performance

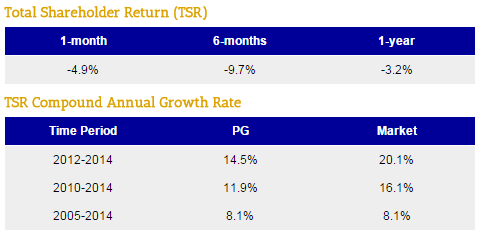

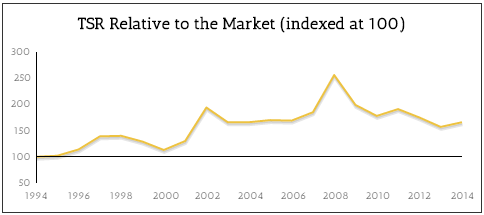

As we all know, P&G’s stock has trailed the market in recent years. As seen below, the stock has generally underperformed the market since 2008, compounding at an 11.9% rate from 2010-2014 compared to the market gaining at a 16.1% clip. Looking near-term, P&G has sold off by 10% over the past six months, a large move for a consumer staples business. Clearly the market has not (yet) rewarded P&G for its transformation efforts underway and is treating the stock as a “show me” story.

Dividend Analysis

We analyze 25+ years of dividend data and 10+ years of fundamental data to understand the safety and growth prospects of a dividend. P&G’s long-term dividend and fundamental data charts can all be seen here.

Dividend Safety Score

Our Safety Score answers the question, “Is the current dividend payment safe?” We look at factors such as current and historical EPS and FCF payout ratios, debt levels, free cash flow generation, industry cyclicality, ROIC trends, and more.

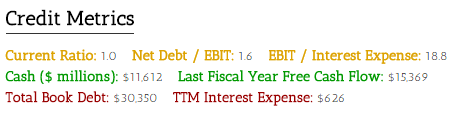

P&G scored a high Safety Score of 88, meaning its dividend is safer than 88% of all other dividend stocks. Management is clearly committed to the dividend, raising it for 59 straight years and paying a dividend for 125 consecutive years.

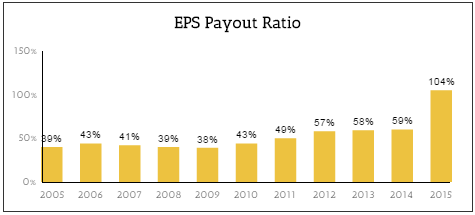

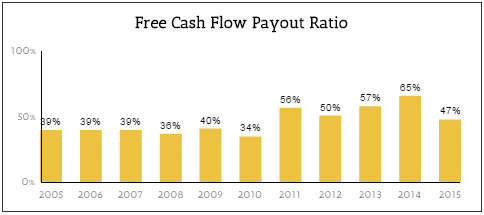

As seen below, P&G has maintained EPS and FCF payout ratios between 40-60% over the past decade, suggesting there is reasonable cushion to continue paying and growing the dividend, even in the event of an unexpected decline in the business. The EPS payout ratio spiked up in fiscal year 2015 because of several divestments and non-recurring charges. Looking forward, the EPS payout ratio will drop back down to 60-70% once results become less noisy. Many of P&G’s top brands are in slow-moving industries and benefit from recurring consumer demand, adding further stability to the business and dividend.

P&G’s balance sheet is also very healthy. As seen below, the company generated $15 billion in free cash flow last year, almost enough to cover the company’s entire remaining net debt of approximately $20 billion. P&G also has a safe net debt / EBIT ratio of 1.6x. The balance sheet further supports the safety of P&G’s dividend.

Dividend Growth Score

Our Growth Score answers the question, “How fast is the dividend likely to grow?” It considers many of the same fundamental factors as the Safety Score but places more weight on growth-centric metrics like sales and earnings growth and payout ratios.

While P&G’s Safety Score was very strong, its Growth Score is much lower at 32. A score of 32 means that the growth prospects for P&G’s dividend are only better than 32% of the 2,700+ dividend stocks we watch. Despite its slower growth, P&G remains a dividend aristocrat.

As seen below, P&G has grown its dividend at a 9% annual clip over the past decade, but the growth rate has steadily declined over each period. Until P&G completes its transformation and gets back to consistent low-single digit organic sales growth and upper-single digit earnings growth, moderate dividend growth rates seem likely going forward.

Yield Score

Our Yield Score simply ranks a stock’s current dividend yield against all of the other dividend yields in the market. A score of 50 means the stock’s yield is right in the middle of the pack. A score of 100 means it has the highest yield.

P&G’s Yield Score is currently 67, placing it nicely above the market’s average dividend yield. While P&G’s Growth Score is on the lower side, its high Safety Score suggests the stock’s valuation has become somewhat undemanding.

Competitive Strengths

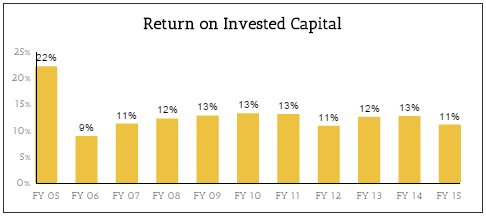

One of the quickest ways to assess the strength of a business model is to evaluate the level and durability of a company’s return on invested capital. As seen below, P&G has generally maintained a return on invested capital in excess of 10% for the past decade, a durable and consistent business:

P&G’s competitive edge starts with its understanding of constantly evolving consumer habits and trends. The company invests $2 billion annually in R&D, conducting thousands of research studies to improve consumer understanding and develop appropriate technologies.

With this understanding and a ridiculous advertising budget (spends over $8 billion per year on advertising), P&G has created a fortress of global brands that dominate the markets they compete in. Almost all of P&G’s 20+ billion-dollar brands hold the #1 or #2 position in their category or segment. Once P&G completes its brand divestiture program, reducing its total categories down to 10, it will be the leader in seven of these 10 categories and #2 in the balance.

Unlike other industries, the non-food consumer products space is very sticky and generally less subject to change. According to IRI Market Advantage, 85% of American household needs are consistently filled with the same 150 items, and 60-80% of new product launches fail. In other words, P&G maintains a highly durable and sticky position with the 5 billion consumers they touch daily, and new entrants really struggle to win over consumers who are happy with incumbents’ offerings.

P&G’s scale ($76 billion in FY15) and global reach (63% of sales are outside the US) also position it well to be a leading supplier to multinational retailers and leverage its supply network.

Finally, P&G’s management team is increasingly looking like a source of competitive advantage. The team has made difficult decisions to exit 100 brands, eliminating approximately 15% of overall sales. However, the remaining brands generate margins that are over 200 basis points higher than the company average and are growing 100 basis points faster as well. In addition to re-focusing the company on its strengths, the team runs the business with a goal of generating a healthy total shareholder return (target is to be in the top one-third of its peer group) by focusing on a balance between sales growth, margin improvement, and operating cash flow generation (not EPS).

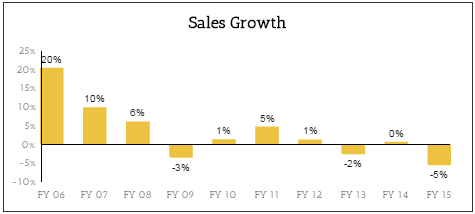

From a growth perspective, it is hard to imagine P&G growing at rates much beyond global GDP due to its large size and focus on stable household and personal care products. With remaining brand divestments underway, headline sales growth will remain negative for the next year. However, by the start of P&G’s fiscal year 2017, growth will reflect P&G’s strongest remaining brands, which should hopefully put up 2-4% organic growth going forward.

Key Risks

Like other multinationals, P&G is dealing with unfavorable currency movements that are impacting growth and profitability. However, P&G has historically recouped 50-75% of unfavorable foreign exchange rate movements with pricing increases, a testament to its strong brands. I view this to be a short-term headwind and something we likely won’t remember a few years from now.

Perhaps the bigger fear with P&G is that the company will struggle to grow organically once the transformation is complete. However, P&G will have significantly more resources to deploy in its remaining brands and categories, helping it maintain or improve share and brand awareness. Additionally, most of the remaining brands and categories have demonstrated nice organic growth in recent years, unlike many of the non-core brands that are in the process of being divested. With the rise of private label products and the risk of middle class customers trading down remains, the case for P&G requires some faith in management’s strategic decisions (i.e. which brands to keep vs divest) that are needed to restore growth.

Conclusion

P&G’s dividend payment is extremely safe, and its current yield is attractive for dividend investors looking for a reliable source of current income. The company’s actions to shed underperforming brands, double-down on its strongest categories, push through additional productivity improvements, and return more cash to shareholders via buybacks and dividends only increase the appeal of P&G’s investment case. Like many other multinationals, foreign exchange fluctuations are creating near-term headwinds, but I would expect P&G’s organic sales growth to accelerate after this year. Until then, patient investors can enjoy collecting their 3.5% dividend yield.