Founded in 1911, Eaton (ETN) is a large industrial conglomerate with approximately $20 billion in annual sales. The company produces products in over 50 countries and sells them in more than 175 markets around the world.

Eaton provides a wide range of energy-efficient products and systems that help customers manage power across electrical, hydraulic, and mechanical applications. The company operates in five main business segments.

- Electrical Products (35% of sales, 40% of profits): consists of electrical components, industrial components, residential products, single phase power quality, emergency lighting, fire detection, wiring devices, structural support systems, circuit protection, and lighting products.

- Electrical Systems & Services (28% of sales, 24% of profits): power distribution and assemblies, three phase power quality, hazardous duty electrical equipment, intrinsically safe explosion-proof instrumentation, utility power distribution, power reliability equipment. The principal markets for these segments are industrial, institutional, governmental, utility, commercial, residential and information technology.

- Vehicle (16% of sales, 17% of profits): supplies drivetrain and powertrain systems and components used in cars, trucks, and agricultural vehicles. Key products include transmissions, clutches, engine valves, and superchargers.

- Hydraulics (12% of sales, 9% of profits): sells components and systems such as pumps, motors, valves, and controls that are used in industrial and mobile equipment. Key end markets are oil and gas, agriculture, construction, and mining.

- Aerospace (9% of sales, 10% of profits): sells fuel, hydraulics, and pneumatic systems used in commercial and military aircraft. Products include pumps, motors, controls, sensing products, hose fittings, and more.

By geography, the U.S. is Eaton’s largest market accounting for 55% of sales, followed by Europe (22%), Asia-Pacific (12%), Latin America (7%) and Canada (5%).

Eaton also has a substantial aftermarket business (approximately 20% of total sales) that provides recurring revenue and more stable cash flow. Aftermarket revenue usually carries high margins and consists of parts, repairs, maintenance, and digital services for equipment sold to customers.

Business Analysis

Eaton represents one of the top quality names in industrial components and services. This is a highly fragmented market with Eaton maintaining less than 10% global market share despite its large base of revenue.

However, the company does enjoy strong competitive advantages in several key areas, including Eaton’s substantial economies of scale. With $20 billion in annual revenue and operations in nearly 60 countries, the company has meaningful purchasing power and can source its inputs in bulk from the cheapest sources. This helps Eaton maintain a lower manufacturing cost structure than most of its smaller rivals.

In addition, Eaton has a network of over 13,000 channel partners that sell its products. The company has spent more than 100 years building up this network, and it’s one that rival upstarts can’t easily replicate to achieve global scale.

In Asia specifically, the largest potential growth market, Eaton’s distribution network has grown by 50% in the past five years. Management hopes to increase that another 30% over the next five years, helping to ensure that the company’s products reach as many customers as possible.

The other major advantage Eaton has is that its products represent a “sticky” ecosystem for its end customers. For example, Eaton builds mission critical components for highly complex industrial machines, including parts used in heavy duty trucks, aircraft, and industrial construction markets.

Reliability is of paramount importance in these industries, since downturn and breakdowns can be extremely costly and disruptive to businesses. In fact, Eaton estimates that unexpected downturn in the global industrial industry costs businesses about $50 billion in lost profits in 2017.

Eaton can also routinely pumps around $600 million into research and development activities each year to maintain the broadest, most advanced portfolio of technologies and established brands.

As a result, Eaton is famous for its high quality and reliability. That’s why its fuel pumps are what General Electric (GE) uses in its latest jet engines, and its heavy duty truck transmissions come with 750,000 mile warranties.

This has led to Eaton enjoying strong market share in most of its industries including:

- No. 4 in global hydraulics

- No. 3 in electrical systems and components (with management planning on achieving No. 1 or No. 2 position within a few years)

- No. 1 in all sub aerospace industries in which it operates

Another benefit Eaton enjoys is that as its installed customer base expands it can sell more aftermarket products and services. According to McKinsey, on average industrial aftermarket EBIT margins are 25% compared to just 10% on original hardware sales.

Since aftermarket revenue tends to carry much higher margins, Eaton can price some of its upfront equipment sales at levels that make it difficult for smaller competitors to earn a profit (a lot of the money is made in equipment support and services).

Smaller rivals also lack the network needed to service multinational customers, who demand timely service and maximum uptime. Simply put, Eaton’s aftermarket business helps the company maintain stickier customer relationships and retain its reputation for quality.

Eaton is especially strong in aftermarket in its aerospace segment where more than 30% of revenue is derived from this higher margin, recurring revenue stream. In heavy vehicles, Eaton’s installed base of nearly five million class 8 trucks allows its hydraulics segment to generate about a third of its revenue from aftermarket sales.

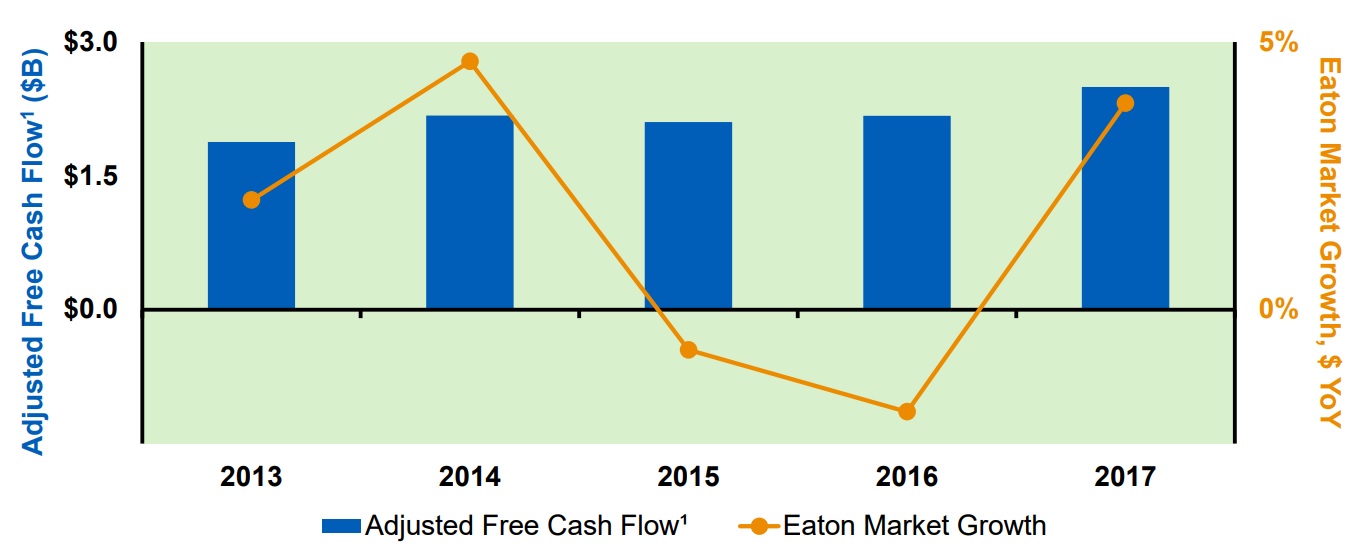

The beauty of aftermarket is that it represents a far less volatile stream of higher margin income. One that has helped Eaton to generate relatively stable adjusted free cash flow even during industry downturns. Adjusted free cash flow is free cash flow adjusted for pension contributions (Eaton’s pension is 95% funded) and legal settlement costs from a 2014 lawsuit.

In fact, Eaton’s cash flow stability has helped the company pay uninterrupted dividends since 1923. This exemplifies both the safe nature of the payout, but also the dividend-friendly corporate culture of the company.

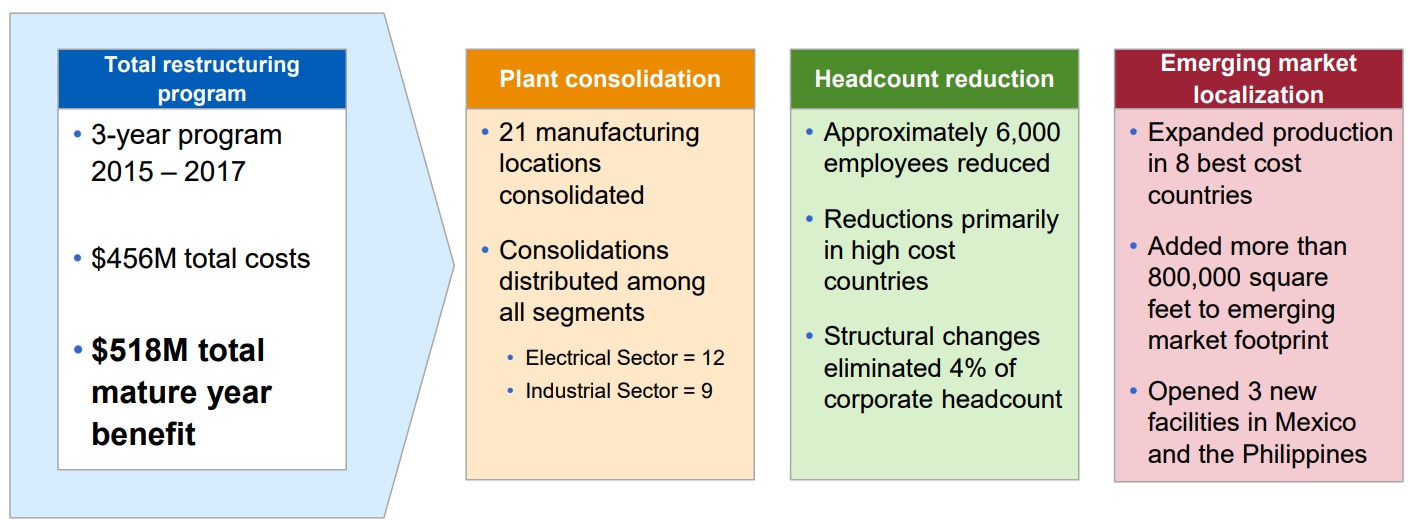

Another competitive advantage is management’s ability to leverage Eaton’s relatively large size to achieve improving economies of scale. In 2015, the company announced a three-year restructuring to coincide with the global industrial recession. This was brought about by a crash in commodity prices that badly hurt the oil, gas, and mining industries.

The turnaround focused on streamlining its logistics chain, closing less profitable factories, downsizing the workforce, and reinvesting into more cost effective production sourcing, including far more sourcing from China.

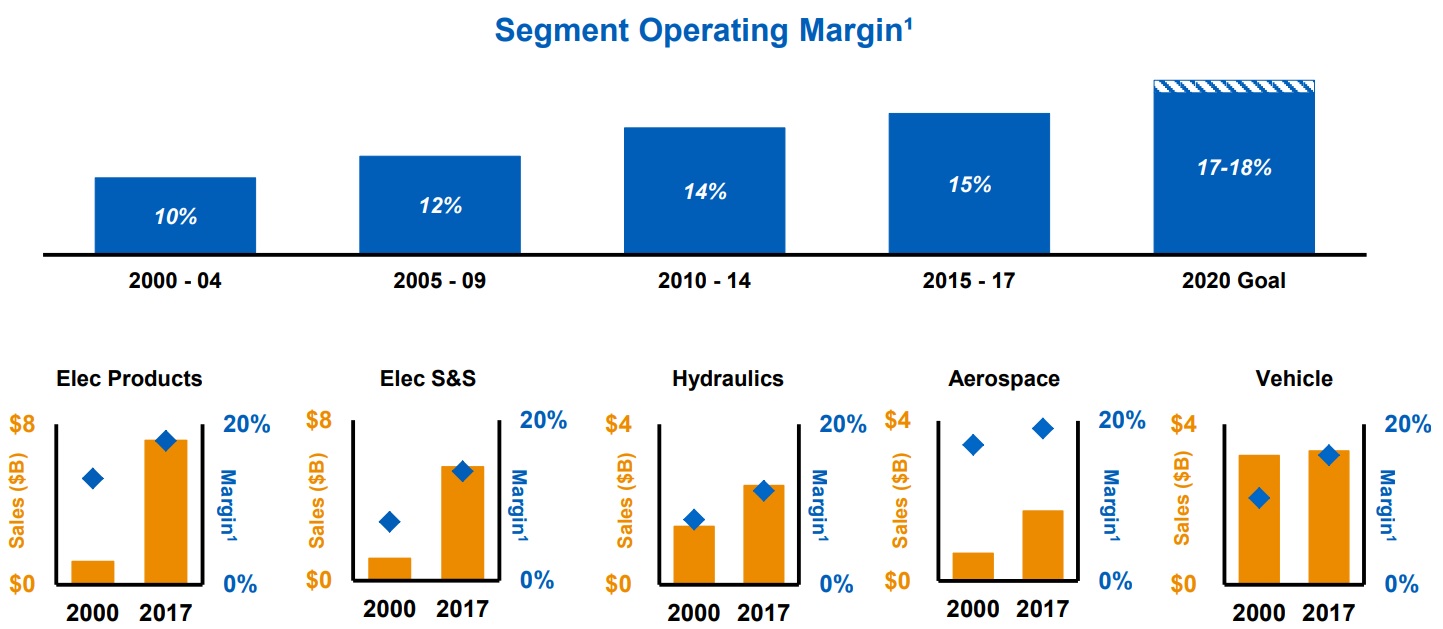

Management expects to achieve $518 million in permanent cost savings from the turnaround plan. As a result of Eaton’s ongoing cost reduction efforts, the company’s operating margin is expected to reach 17-18% by 2020, nearly doubling the 10% margin it recorded in the early 2000’s.

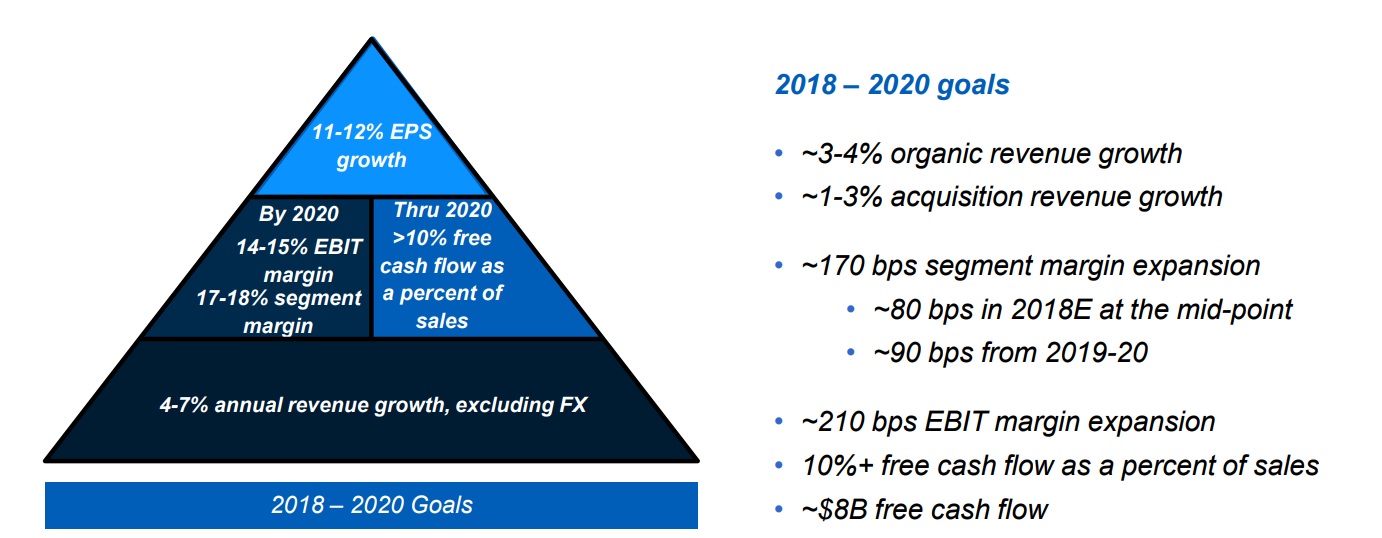

Going forward, management has a two pronged approach to achieve mid-single-digit sales growth, low double-digit earnings growth, a free cash flow margin above 10%, and another 210 basis points of operating margin expansion.

First, the company hopes to achieve 3% to 4% organic sales growth by targeting key fast-growing markets with the largest future growth potential. These include:

- Electrical: $200 billion addressable market

- Hydraulics: $40 billion market

- Electrical Vehicles: $33 billion market (by 2030)

- Factory automation: $3 billion market

- Energy Storage: $5 billion (by 2023)

- Driverless cars: $3 billion market (by 2030)

Combined with about 1% to 2% annual share buybacks and expanding margins, Eaton expects this to drive double-digit earnings growth and solid free cash flow margins.

A good deal of Eaton’s R&D spending targets digitization of industrial markets. For example, analysts expect over 30 billion global products to be connected to the internet in the so called “internet of things” (IoT) by 2020. Much of the strongest growth in IoT is expected to come from industrial sectors where constant data monitoring can vastly improve the efficiency and reliability of various components.

The $10 trillion per year global construction industry is one example where productivity growth has been far slower than in other industrial sectors. Eaton is focused on creating products that can speed up construction times, but also result in far more energy efficient buildings, with superior electrical component reliability.

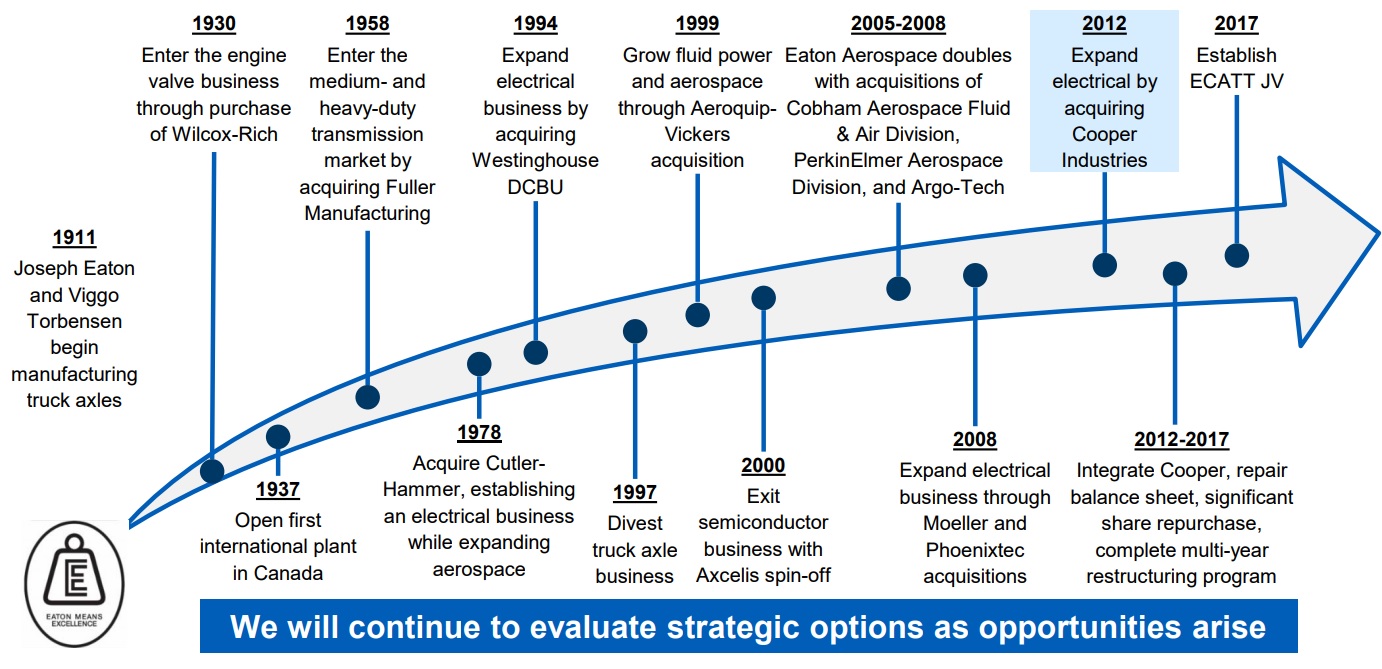

Another major growth driver will be acquisitions, which are expected to add 1% to 3% to Eaton’s annual sales growth over the next few years. Since 2000, the company has made over 65 total purchases, most of which where small bolt-on purchases to augment Eaton’s core strengths.

However, Eaton isn’t afraid to make needlemoving purchases, such as its 2012 acquisition of Cooper for $11.8 billion. Cooper was a major electrical equipment manufacturer specializing in: fuses, lighting controls, voltage regulators, circuit-protection equipment that helps companies save money on energy.

Eaton’s acquisition of Cooper vastly expanded its electrical component business, increased its total addressable market by about $70 billion, and created a denser distribution network to help the business compete better with some of its bigger rivals.

The Cooper acquisition also allowed Eaton to move its headquarters to Ireland which has a 12.5% corporate rate. Even after the recent tax reform and accounting for its global operations, Eaton expects its long-term corporate tax rate to be about 15%, which is far lower than most of its peers.

Eaton did have to take on a lot of debt to buy Cooper, but since then it has largely restored its balance sheet, and management says the company is ready to start acquiring rivals once more. However, Eaton has a very disciplined approach to purchases including a comprehensive checklist:

- Total addressable market: at least $2 billion

- Long-term growth potential: faster than global GDP growth

- Operating margins: mid teens

- Returns on tangible assets: mid 20’s or above

- Operating margins in trough of industry cycle: mid teens

- Accretive to earnings within two years

- Returns on invested capital: at least 3% above cost of capital

Overall, Eaton represents a well-managed industrial conglomerate and possesses a number of durable competitive advantages. The company’s long operating history has allowed it to develop highly profitable and sticky relationships with customers who are most focused on reliability of mission critical components.

When combined with Eaton’s large installed base, which leads to a fast-growing and high-margin aftermarket business, the business is a potentially solid dividend growth investment for the future.

That being said, Eaton still faces its fair share of risks and potential future problems.

Key Risks

Since Eaton is incorporated in Ireland, U.S. investors are subject to a 20% withholding tax on dividends. Fortunately, an Ireland / U.S. tax treaty allows American shareholders to deduct this withholding dollar for dollar against their U.S. tax liabilities, offsetting most of the withholding.

However, single investors can only deduct the first $300 ($600 for couples) in their portfolios on their 1040 tax forms. Amounts over this require the more complicated 1116 tax form.

Regarding company-specific risks, there are several. First, like almost all industrial companies, Eaton’s sales and earnings are cyclical and tied to the health of the global economy and the industries in which it operates.

For example, much of the hydraulics business services the mining, oil, and gas industries. As 2015 and 2016 showed, volatility in commodity prices can have a strong negative effect on short-term results.

Furthermore, because nearly 50% of Eaton’s sales are generated overseas, there is significant foreign exchange risk. If the U.S. dollar appreciates against local currencies, than foreign sales will translate into less earnings and cash flow when it comes to accounting purposes.

There’s also the issue of potential trade barriers rising in the future. Eaton has said that the recently announced U.S. steel and aluminium tariffs would raise its costs by $50 million per year. The good news is that most countries have been temporarily exempted from those tariffs, but if those exemptions are lifted then Eaton’s input costs could rise.

A potentially bigger threat is the fact that Eaton’s restructuring led to significantly greater foreign sourcing of components, especially from China. Should the U.S. and China get into a long-lasting trade war, than Eaton could be at a competitive disadvantage relative to its peers.

Which brings us to the broader issue of commodity risk. Eaton’s cost cutting has been impressive, but if overall global input costs for materials such as steel rise, then Eaton’s margins could decline in the short term. That could result in earnings and dividend growth disappointing investors.

While these macro issues can weigh on Eaton’s results any given quarter or year, they seem unlikely to impact the company’s long-term earnings power.

However, management’s plans for increased M&A activity in the coming years could have a more structural impact on the business. While Eaton’s track record with acquisitions is generally good, and its standards for new purchases are high, every acquisition comes with execution risk. Eaton will have to avoid overpaying for an acquisition, and then successfully integrate the new company’s products, supply chains, and culture into its own.

Whether or not such mergers become accretive within the company’s two-year time goal will largely depend on achieving targeted synergistic cost savings. Synergies can prove challenging to recognize and are far from guaranteed.

Overall, Eaton’s business diversification, long operating history, healthy cash flow generation, and slow-changing markets reduce its risk profile.

Closing Thoughts on Eaton

Eaton is a quality business that seems likely to remain relevant for many years to come. The company’s moat is driven by its long-standing market positions, extensive product portfolio, massive distribution channels, sizable aftermarket business, and leading technologies.

When combined with management’s disciplined approach to acquisitions, plans to win market share in critical industries of the future, and successful restructuring, Eaton seems very likely to continue delivering safe and growing dividends for many years to come.

For dividend investors seeking a secure income investment with decent long-term growth prospects, Eaton may be an interesting industrials candidate as part of a well-diversified dividend portfolio.

To learn more about Eaton’s dividend safety and growth profile, please click here.