Tracing its roots back to 1886, Diageo (DEO) is the largest producer of spirits in the world and was formed in 1997 after the merger of Guinness and Grand Metropolitan. Diageo is a British company, but the UK does not impose any foreign dividend tax withholdings on investors.

Some of the firm’s 200 leading global brands include Smirnoff (#1 spirit brand by volume), Captain Morgan, Guinness, Johnnie Walker (#1 spirit brand by value), and Bailey’s. Its top six “global giants” brands accounted for 43% of sales in 2017 and grew 5%.

Diageo sells over 6.5 billion liters of beverages in over 180 countries and territories around the world each year. By beverage category, the company’s most important products are scotch (25% of revenue), beer (16%), and vodka (12%).

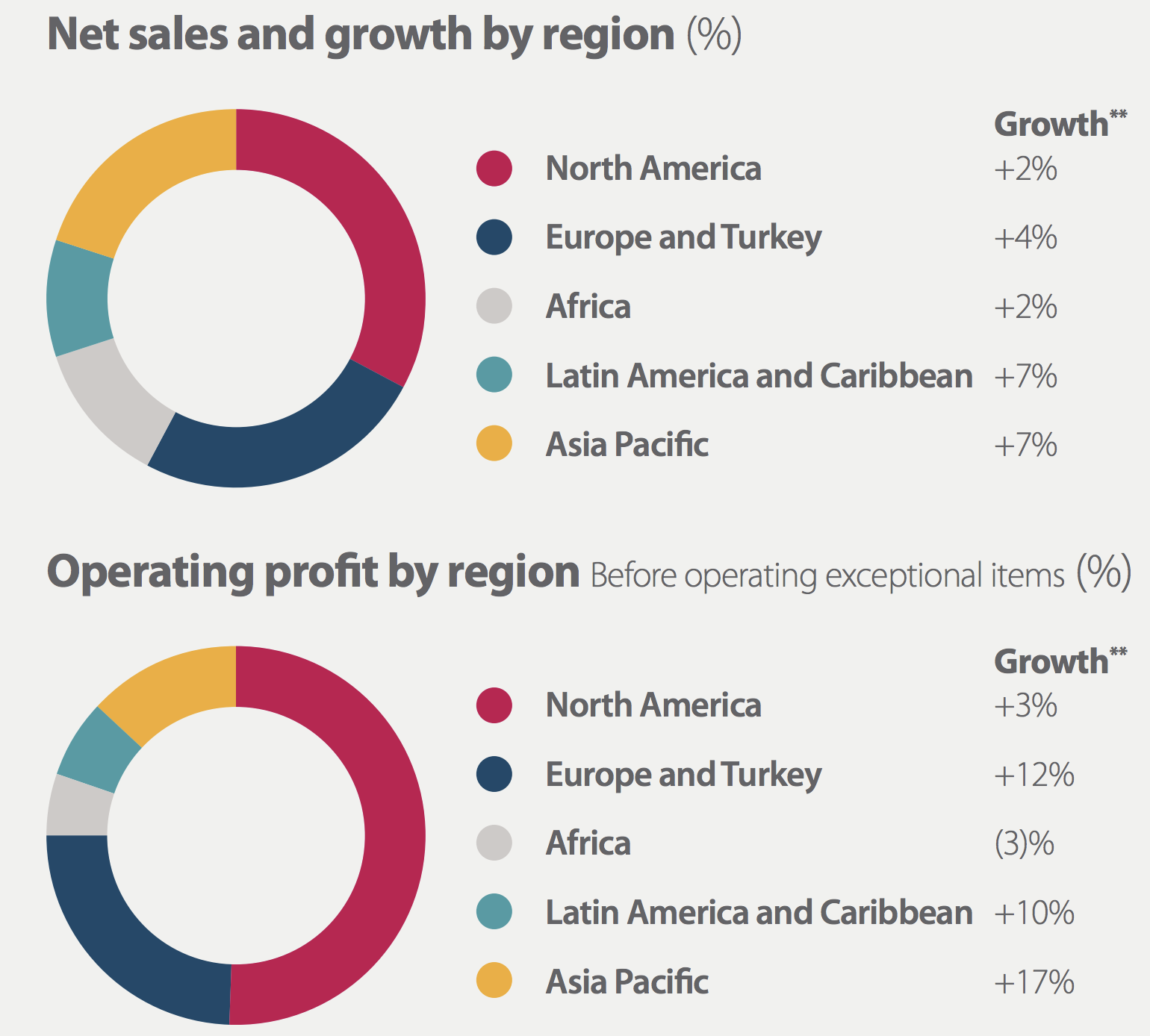

While Diageo is highly diversified geographically, the vast majority of its profits still come from North America (50% of profit) and Europe (25% of profit). However, the fastest growth is in emerging markets (42% of sales) such as Latin America and Asia.

Business Analysis

Diageo’s key strengths are its global distribution network (products are sold in over 180 countries), well-known brands (many have hundreds of years of history behind them), broad portfolio (sells at every price tier of every category), dominant market share, and large marketing budget (spent over $2 billion on marketing in 2017).

Despite its large size, Diageo still offers attractive long-term dividend growth potential for income investors. In fact, the firm currently commands just 27% market share, creating strong growth potential for Diageo to gain market share organically and through industry consolidation.

However, despite the highly fragmented nature of the market (there are 12 major global spirit producers), Diageo also enjoys numerous competitive advantages due to its collection of leading global and regional brands, many of which command the number one or two market share in their product categories. In fact, according to Morningstar, Diageo owns 14 of the top 100 spirit brands in the world and seven of the top 20.

In business for more than 130 years, Diageo has also built up the industry’s largest worldwide distribution network, which which is very hard (and monstrously expensive) for competitors to replicate. The firm’s global reach allows it to easily expand sales of its brands across numerous geographies. It also helps the company’s efforts to quickly introduce new or acquired products to the market to meet changing consumer preferences.

And due to its pricing power and substantial economies of scale, including advanced manufacturing capabilities and sourcing from all over the world (a relatively small number of raw inputs are required), Diageo enjoys some of the highest profitability in the industry with a free cash flow margin in excess of 20%.

Despite the industry’s impressive profitability, the spirits market has seen its global sales growth slow to less than 1% per year, which is expected to continue for the next few years. As a result, Diageo will need to gain market share to continue growing.

The company’s strategy is focused on increasing sales of its most premium “reserve” brands to address the mass luxury market. This is especially important in emerging markets such as China, India, and Latin America where fast growing middle classes often view famous foreign brands as aspirational products whose consumption is a signal of success. Thus far, Diageo’s efforts have driven solid organic growth across its portfolio.

The company is also changing with the times and offering new “on trend” products under its most popular brands. For example, to target more health conscious consumers, Diageo launched Bailey’s Almande which is a gluten free, dairy free, vegan almond milk liqueur. It also launched Smirnoff Seltzer in the U.S. and Smirnoff Pure in Australia, two low calorie and low sugar ready-to-drink products.

Diageo has been focused on optimizing its product portfolio as well by selling off weaker brands, including the divestiture of its wine business in 2015. Instead, the firm is focused more on premium spirits such as its $700 million acquisition of super-premium tequila brand Casamigos.

Management’s strategy appears to be working with Diageo recently reporting 2% organic volume growth, about three times the industry average. In addition, management plans to cut 700 million pounds a year in costs (due to adopting zero based budgeting) between 2017 and 2019. Diageo believes this can boost its operating margin by another 175 basis points.

The combination of gaining market share, cutting costs (boosting margins), and ongoing share buybacks is why analysts currently expect Diageo to grow its earnings and cash flow by about 8% per year over the long term. If the company can hit those expectations, than it should be able to grow its dividend at about 7% to 8% per year as well, in line with its long-term average.

All things considered, Diageo seems to have many of the characteristics possessed by some of the best blue-chip dividend stocks – a portfolio of leading brands with hundreds of years of history in some cases, strong and consistent profitability, participation in large and slow-changing markets, and a management team focused on the long term.

Key Risks

There are several risks to consider before investing in Diageo. First, income investors need to be aware that while Diageo pays its dividends in U.S. dollars, it is a British company which reports its results in British Pounds. As a result, its semi-annual dividend payments fluctuate with the second payment of the year usually being larger.

However, the actual amount paid by Diageo to American investors can be affected by the exchange rate between the U.S. Dollar and British Pound, which has significantly weakened and become more volatile since the country voted to exit the European Union. In other words, investors looking for highly consistent payments might want to avoid this stock.

As it relates to fundamental risks to the business, Diageo must deal with changes in consumer tastes as different liquor types go in and out of favor. For example, vodka sales in the U.S. have struggled with negative volume growth for several years and only recently returned to very modest growth. This is a reversal of the trend that started in the 1990’s when brown spirits (like Scotch) fell out of favor while white spirits (like vodka) became more popular.

Meanwhile, in Canada the company’s volumes continue to decline (2%), and Diageo’s Australian volumes recently fell by 10% as consumer tastes shifted and the company has yet to successfully evolve its product mix there. Adapting isn’t as easy as simply flipping the switch on a machine, because many spirits (like scotch and bourbon) take a long time to age properly. Therefore, if management misjudges future consumer preferences, than volumes, sales, and profits in a particular region can take a hit for several years.

Diageo’s diversified portfolio of drinks and geographies (see below) reduces some of this risk, but shifting consumer tastes in the firm’s largest categories have caused multiyear stretches of market share losses in the past.

In addition, distilled spirits are more sensitive to the health of the economy due to their highest costs. In fact, historically their sales have been over twice as correlated to GDP growth than cheaper alternatives such as beer.

Another risk is posed by changes in government policy, including higher excise duties on alcohol which can substantially alter the price consumers have to pay. For instance, in 2017 Diageo paid an average of 25% alcohol taxes on its products.

Cash-strapped governments frequently try to increase “sin” taxes to raise revenue. This creates the risk that the effective cost for Diageo’s consumers, especially in emerging markets, might rise to levels that start to hurt sales. Or at the very least higher alcohol taxes could reduce the company’s ability to raise prices over time.

Over the short term, inflation and wild currency swings can be a challenge for the company, especially in emerging markets. For example, in mid-2018 Argentina’s Peso collapsed after its central bank lowered its interest rate in order to boost the economy.

Overall, currency fluctuations reduced company-wide net sales growth by 200 basis points over the last six months. This highlights the downside of relying so much on fast growing but less economically stable regions to power the company’s long-term growth.

And speaking of emerging markets, while consumers in developed markets are trading up from beer to spirits, this hasn’t been the trend in emerging markets. Instead, consumers in less affluent countries are trading up within product segments (higher price points) rather than switching product categories (such as beers to spirits).

Should this continue, Diageo’s growth potential in these markets might be less than analysts previously believed under the thesis that a larger middle class would both trade up by price point and by category type (to more expensive alcohol categories).

Finally, while Diageo has been focused more on organic growth in recent years (as opposed to large acquisitions), many spirit companies will occasionally acquire new brands and even rivals due to the fragmented nature of the market. The pursuit of large deals can result in integration challenges and the risk of overpaying (prices in recent years on premium spirit brands have soared).

Closing Thoughts on Diageo

Diageo enjoys numerous competitive advantages, including a large portfolio of top-tier brands, the industry’s largest global manufacturing and distribution system, and a major presence in the world’s emerging economies.

Thanks to the company’s excellent profitability and management’s conservatism, Diageo has paid uninterrupted dividends for 19 consecutive years (though U.S. investors must remember that the actual payments they will receive can fluctuate based on currency exchange rates). Overall, Diageo might make a solid dividend growth choice for investors seeking exposure to the alcoholic beverages industry.

To learn more about Diageo’s dividend safety and growth profile, please click here.